filmov

tv

Should You Allocate All Your Retirement Funds to the S&P 500?

Показать описание

Many younger investors advocate for an all-equity allocation at younger ages. Is this a wise idea or is there value to being diversified even at a young age?

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

0:06:05

0:06:05

Should You Allocate All Your Retirement Funds to the S&P 500?

0:05:06

0:05:06

How To Allocate More RAM to Minecraft Java Edition in 2023

0:09:40

0:09:40

What Percentage of Revenue Should You Allocate to Marketing?

0:07:08

0:07:08

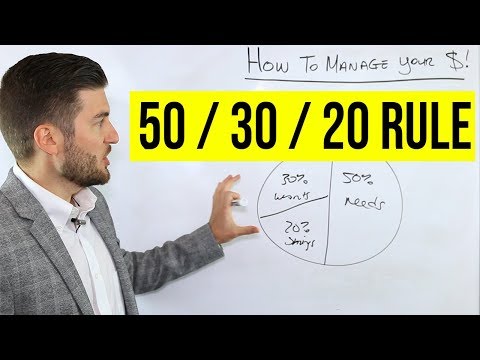

How To Manage Your Money (50/30/20 Rule)

0:01:06

0:01:06

How Should You Allocate Your Time? #shorts

0:03:01

0:03:01

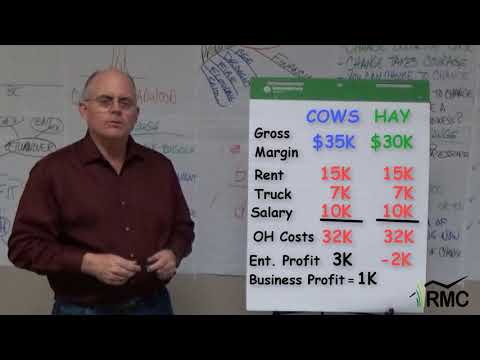

How should you allocate overhead costs?

0:08:20

0:08:20

Do you need to allocate all of your own Grad School funding?

0:00:35

0:00:35

Should You Allocate 100% in Equity?

0:01:09

0:01:09

Management Jargon Series: What Does “Focus” Mean In Business?

0:05:33

0:05:33

How Much Of The Budget Should You Allocate For Content Strategy?

0:00:41

0:00:41

Its okay to allocate your time accordingly to relationships

0:10:42

0:10:42

How Should You Allocate Your Time & Money | Homeschooling

0:00:24

0:00:24

How Do You Allocate Your Assets?

0:00:09

0:00:09

How to allocate your money when investing. 80% index funds, 20% stocks investing strategy

0:14:33

0:14:33

🤑 6600% 🚀 THIS COULD RUN! 🔥 HOW TO INVEST ⛔️ BEST STOCKS TO BUY NOW! ⚠️

0:07:13

0:07:13

To-Do List Overload! How to Manage Too Many Tasks

0:47:12

0:47:12

How should you allocate your assets?

0:00:34

0:00:34

How to Fix Out of video memory trying to allocate a texture

0:02:55

0:02:55

How to Allocate More RAM to a Program? | Increase Your System’s Performance

0:07:02

0:07:02

How to Allocate More RAM to Specific Programs On Windows

0:00:56

0:00:56

What percentage of your income do you allocate towards investments? Comment below👇🏻

![[ENG SUB/Hololive] Miko,](https://i.ytimg.com/vi/8wBYjCAKKs8/hqdefault.jpg) 0:00:22

0:00:22

[ENG SUB/Hololive] Miko, Matsuri, Noel & Botan - When you allocate all your stats in one slot

0:00:18

0:00:18

Allocate more CPU to DAW (WINDOWS)

0:03:19

0:03:19

How to allocate unallocated space MacOS (Resize HDD Partition) - Tutorial 2021

Комментарии