filmov

tv

Balance sheet and income statement relationship

Показать описание

How do the income statement and balance sheet connect and interact? Which financial statement is more important: the balance sheet or the income statement? The answer is: both! They each have their own focus and purpose. This video provides you a deep understanding in less than five minutes.

⏱️TIMESTAMPS⏱️

00:00 Intro

00:21 What is a balance sheet

00:51 What is an income statement

01:13 Balance sheet and income statement relationship

01:35 Raising capital

02:00 Plant and Equipment (P&E)

02:17 Buying inventory from supplier

02:33 Recording expenses

02:59 Sales transaction

03:19 Profitability

03:40 Retained earnings

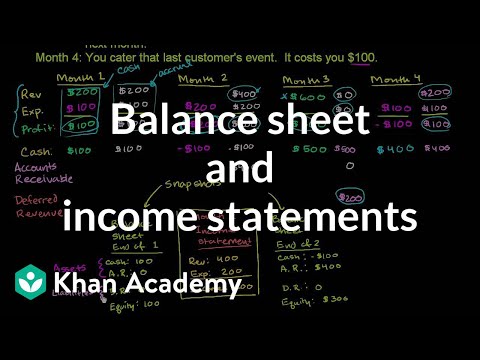

The balance sheet is an overview of a company’s assets and liabilities at a point in time, usually the end of a quarter or the end of the year. A balance sheet shows you what a company owns (on the left hand side), and what a company owes (on the right hand side). As the term “balance sheet” suggests, the total assets should match the total liabilities, what we own equals what we owe. A balance sheet shows you where you got the capital for the company (on the right), and what you have invested it in (on the left).

The income statement, or profit and loss statement, is an overview of how much a company has earned during a period. Some companies use the terms revenue, expenses and profit. Others use sales, costs, and earnings or income. If your revenue is bigger than your expenses, you make a profit. If expenses are bigger than revenue, you make a loss.

The way to remember these easily is to think of the balance sheet as a picture at a point in time, and the income statement as a movie about a certain period.

Let’s put the balance sheet and income statement side by side, starting with a blank sheet. We will make some simple journal entries to show the relationship between balance sheet and income statement.

If we start a company, we need to raise capital. The certificates of ownership that we give to shareholders are called equity, and they send us cash. Our company now owns a cash balance (on the left), and owes equity to the shareholders.

Then we might apply for a loan from the bank. When we sign the loan agreement, we are in debt to the bank. In return, we receive cash.

With the money we raised, we buy Plant and Equipment, in short P&E, or fixed assets. A building and some machines. We now own the Plant and Equipment, and in return for getting the keys to the building and the keys to a forklift truck, our cash is reduced.

We order inventory from a supplier. The delivery truck brings you the inventory (another asset, something you now own), and you receive an invoice from your supplier that you have not paid yet (accounts payable, you owe money to your supplier).

So far, we have only touched the balance sheet, growing both what we own and what we owe. Let’s record some costs or expenses. We receive an interest charge related to the bank loan, and pay it in cash. We account for the usage (value deterioration) of the Plant and Equipment through a depreciation entry. We record salaries (compensation and benefits) for the staff in our shop, and pay them in cash.

Then we finally make our first sale. Note that this took quite a while after starting the company. For the sales transaction, we record the invoicing of the revenue, and the claim to future cash (accounts receivable) from our customer. We also record the shipment of the goods to the customer, and the related Cost of Sales.

Then we can calculate subtotals: Gross Profit, Operating Profit (or EBIT Earnings Before Interest and Tax), Profit Before Tax. We record the tax charge of 20% of the EBT, paying it in cash. And then, to finish off the income statement, we calculate Net Income.

Now we seem to have a problem. Our balance sheet does not balance. Our assets are bigger than our liabilities. What are we missing? This is where we need to remember that the balance sheet is a picture at a point in time, and the income statement is a movie about a certain period. We need to somehow connect the picture and the movie. To do that, we add the net income earned during the year to the balance sheet of the end of the year. Interest is the reward for the bank for granting us a loan. Net income is the reward for the shareholders for making risk-bearing capital available. We add the Net Income earned during the year to Equity, in a sub-account called Retained Earnings. And the balance sheet balances!

That’s how the balance sheet and income statement fit together.

Philip de Vroe (The Finance Storyteller) aims to make strategy, finance and leadership enjoyable and easier to understand. Learn the business and #accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better stock market investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

⏱️TIMESTAMPS⏱️

00:00 Intro

00:21 What is a balance sheet

00:51 What is an income statement

01:13 Balance sheet and income statement relationship

01:35 Raising capital

02:00 Plant and Equipment (P&E)

02:17 Buying inventory from supplier

02:33 Recording expenses

02:59 Sales transaction

03:19 Profitability

03:40 Retained earnings

The balance sheet is an overview of a company’s assets and liabilities at a point in time, usually the end of a quarter or the end of the year. A balance sheet shows you what a company owns (on the left hand side), and what a company owes (on the right hand side). As the term “balance sheet” suggests, the total assets should match the total liabilities, what we own equals what we owe. A balance sheet shows you where you got the capital for the company (on the right), and what you have invested it in (on the left).

The income statement, or profit and loss statement, is an overview of how much a company has earned during a period. Some companies use the terms revenue, expenses and profit. Others use sales, costs, and earnings or income. If your revenue is bigger than your expenses, you make a profit. If expenses are bigger than revenue, you make a loss.

The way to remember these easily is to think of the balance sheet as a picture at a point in time, and the income statement as a movie about a certain period.

Let’s put the balance sheet and income statement side by side, starting with a blank sheet. We will make some simple journal entries to show the relationship between balance sheet and income statement.

If we start a company, we need to raise capital. The certificates of ownership that we give to shareholders are called equity, and they send us cash. Our company now owns a cash balance (on the left), and owes equity to the shareholders.

Then we might apply for a loan from the bank. When we sign the loan agreement, we are in debt to the bank. In return, we receive cash.

With the money we raised, we buy Plant and Equipment, in short P&E, or fixed assets. A building and some machines. We now own the Plant and Equipment, and in return for getting the keys to the building and the keys to a forklift truck, our cash is reduced.

We order inventory from a supplier. The delivery truck brings you the inventory (another asset, something you now own), and you receive an invoice from your supplier that you have not paid yet (accounts payable, you owe money to your supplier).

So far, we have only touched the balance sheet, growing both what we own and what we owe. Let’s record some costs or expenses. We receive an interest charge related to the bank loan, and pay it in cash. We account for the usage (value deterioration) of the Plant and Equipment through a depreciation entry. We record salaries (compensation and benefits) for the staff in our shop, and pay them in cash.

Then we finally make our first sale. Note that this took quite a while after starting the company. For the sales transaction, we record the invoicing of the revenue, and the claim to future cash (accounts receivable) from our customer. We also record the shipment of the goods to the customer, and the related Cost of Sales.

Then we can calculate subtotals: Gross Profit, Operating Profit (or EBIT Earnings Before Interest and Tax), Profit Before Tax. We record the tax charge of 20% of the EBT, paying it in cash. And then, to finish off the income statement, we calculate Net Income.

Now we seem to have a problem. Our balance sheet does not balance. Our assets are bigger than our liabilities. What are we missing? This is where we need to remember that the balance sheet is a picture at a point in time, and the income statement is a movie about a certain period. We need to somehow connect the picture and the movie. To do that, we add the net income earned during the year to the balance sheet of the end of the year. Interest is the reward for the bank for granting us a loan. Net income is the reward for the shareholders for making risk-bearing capital available. We add the Net Income earned during the year to Equity, in a sub-account called Retained Earnings. And the balance sheet balances!

That’s how the balance sheet and income statement fit together.

Philip de Vroe (The Finance Storyteller) aims to make strategy, finance and leadership enjoyable and easier to understand. Learn the business and #accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better stock market investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

0:04:33

0:04:33

Balance sheet and income statement relationship

0:06:59

0:06:59

The BALANCE SHEET for BEGINNERS (Full Example)

0:03:41

0:03:41

Balance sheet and income statement relationship | Finance & Capital Markets | Khan Academy

0:12:19

0:12:19

Connecting the Income Statement, Balance Sheet, and Cash Flow Statement

0:09:06

0:09:06

FINANCIAL STATEMENTS: all the basics in 8 MINS!

0:05:09

0:05:09

The INCOME STATEMENT for BEGINNERS

0:17:23

0:17:23

STATEMENT OF FINANCIAL POSITION(BALANCE SHEET FOR A SOLE TRADER)FINAL ACCOUNTS P2 #accounting#viral

0:11:51

0:11:51

Income statement and Balance sheet Q1

0:08:18

0:08:18

How the Profit & Loss CONNECTS to the Balance Sheet

0:09:10

0:09:10

BALANCE SHEET explained

0:09:17

0:09:17

Relationship between 💵 Income Statement & ⚖️ Balance Sheet

0:05:17

0:05:17

Balance Sheet vs Income Statement

0:21:32

0:21:32

How To Read & Analyze The Balance Sheet Like a CFO | The Complete Guide To Balance Sheet Analysi...

0:08:28

0:08:28

How to Prepare an Income Statement (Step by Step)

0:30:28

0:30:28

Financial Statements Explained | Balance Sheet | Income Statement | Cash Flow Statement

0:21:23

0:21:23

TRADING AND PROFIT AND LOSS ACCOUNT ( INCOME STATEMENT PART 1 ) FINAL ACCOUNT OF A SOLE TRADER

0:12:48

0:12:48

How The BALANCE SHEET Works (Statement of Financial Position / SOFP)

0:12:33

0:12:33

FA5 - Preparing the Income Statement

0:11:24

0:11:24

How to Analyze an Income Statement Like a Hedge Fund Analyst

0:11:18

0:11:18

Balance Sheet (Filipino)

0:43:53

0:43:53

FINAL ACCOUNTS OF A SOLE TRADER (PART 1)

0:29:29

0:29:29

REB| S6| Entrepreneurship| Unit 5| Lesson 5: Preparation of an income statement |

0:57:13

0:57:13

INCOME STATEMENT KNEC REVISION

0:06:17

0:06:17

Worksheet 3 - Income Statement and Balance Sheet Columns

Комментарии