filmov

tv

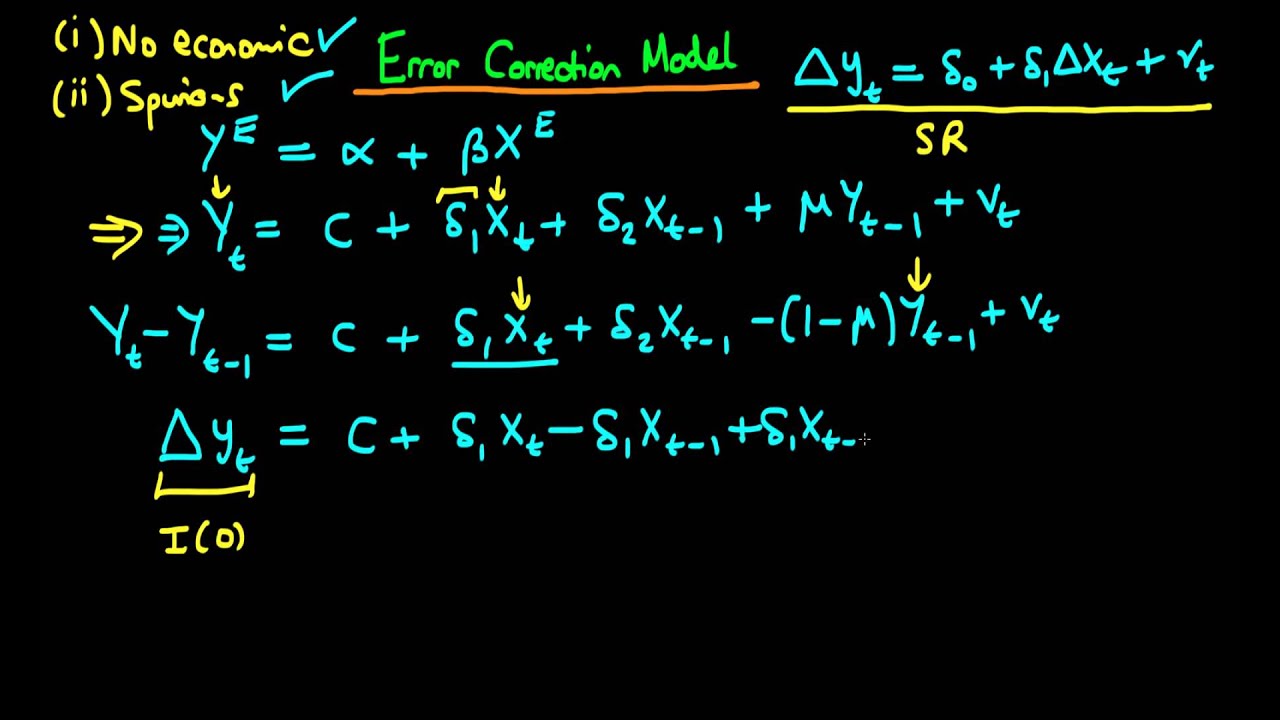

Error correction model - part 1

Показать описание

In this video I introduce the concept of an Error Correction Model, and explain its importance in econometrics.

0:10:02

0:10:02

Error correction model - part 1

0:14:03

0:14:03

Time Series: Error Correction Model explained in Eviews

0:07:01

0:07:01

Error correction model - part 2

0:26:21

0:26:21

Cointegration and Error Correction Model in Stata

0:11:22

0:11:22

The error correction model

0:02:54

0:02:54

Video 20 - Impulse response functions Eviews vector error correction model (part 2)

0:12:33

0:12:33

Introduction to the Vector Error Correction Model

0:12:54

0:12:54

Econometrics - Cointegration and Error Correction Model

0:07:38

0:07:38

'Ought to'&'Dare'|Common Errors in the Use of Model Verb|Basic English Gra...

0:09:56

0:09:56

Video 14 - Vector error correction model Eviews (part 3)

0:10:38

0:10:38

(Stata13): Estimate ARDL and Error Correction Models #ardl #ecm #boundstest #cointegration #lags

0:03:15

0:03:15

GRETL_ Error Correction Model 01

0:10:48

0:10:48

HOW TO DO VECTOR ERROR CORRECTION MODEL (VECM) EVIEWS

0:12:44

0:12:44

Econometrics - Vector Error Correction Model: Johansen Test

0:09:25

0:09:25

Video 13 - Vector error correction model Eviews (part 2)

0:14:08

0:14:08

Time Series Analysis Cointegration and error correction model

0:07:11

0:07:11

co-integrated and error correction model in eview

0:12:15

0:12:15

R studio - Johanson Juselius Vector Error Correction Model for Multi Equilibria Timeseries Data

1:39:20

1:39:20

ecs4863 Error Correction Model (ECM)

0:09:50

0:09:50

Error Correction Model (ECM) part 2

0:09:41

0:09:41

Video 19 - Impulse response functions Eviews Vector Error Correction Model (part 1)

0:07:31

0:07:31

Specifying Vector Error Correction Models #vecm #var #lags #Johansen #serialcorrelation #innovations

0:24:25

0:24:25

Error Correction Model (ECM)-Class Lecture

0:27:46

0:27:46

13. Vector Error Correction Model (VECM) using EViews || Dr. Dhaval Maheta

Комментарии