filmov

tv

Time Series: Error Correction Model explained in Eviews

Показать описание

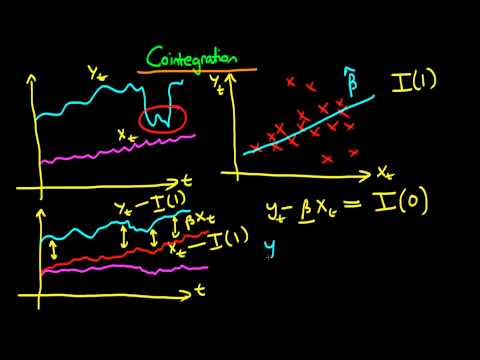

EViews tutorial: Error Correction Model explained in Eviews Step by Step! Hello Everyone! By watching the video "Time Series: Error Correction Model explained", you will learn how to estimate error correction model in eviews step by step and interpret the results. An error correction model is estimated after having determined cointegration among the variables in the model.

📈 Download the dataset for free and replicate the content of the video:

✅ Visit my website to see all my FREE tutorials:

☕️ If you value my content and would like to show a recognition, you can make a donation:

Ensure to watch the 1st Video: "Cointegration - Engle and Granger method in EViews".

---------------------------------------------------------------------------------------------------------

✅ Is there any topic you would like me to cover? Do you have any research questions? Contact me at:

---------------------------------------------------------------------------------------------------------

🗂Video Material:

📈Critical Values Table for Cointegration:

---------------------------------------------------------------------------------------------------------

📚Recommended Literature:

📚Yule (1926): Why do we Sometimes get Nonsense-Correlations between Time-Series?- A Study in Sampling and the Nature of Time-Series

📚 Granger and Newbold (1974): Spurious Regressions in Econometrics

📚 Engle and Granger (1987): Co-Integration and Error Correction: Representation, Estimation, and Testing

---------------------------------------------------------------------------------------------------------

Time Stamps

Introduction 0:00

ECM Overview 0:37

Error Correction Term Details 1:48

Estimating the ECM 3:12

Long and Short Run Model 5:09

Model Diagnostics 7:30

In Sample Forecast 11:32

---------------------------------------------------------------------------------------------------------

✅ Interested in learning more?

🎬 EViews Course videos:

🎬 Stata Course videos:

---------------------------------------------------------------------------------------------------------

If you liked the video and would like more content, please support my channel subscribing!

👍Like and subscribe for more videos!

☕️ If you would like to show your appreciation and make a donation:

Thanks a lot!

📈 Download the dataset for free and replicate the content of the video:

✅ Visit my website to see all my FREE tutorials:

☕️ If you value my content and would like to show a recognition, you can make a donation:

Ensure to watch the 1st Video: "Cointegration - Engle and Granger method in EViews".

---------------------------------------------------------------------------------------------------------

✅ Is there any topic you would like me to cover? Do you have any research questions? Contact me at:

---------------------------------------------------------------------------------------------------------

🗂Video Material:

📈Critical Values Table for Cointegration:

---------------------------------------------------------------------------------------------------------

📚Recommended Literature:

📚Yule (1926): Why do we Sometimes get Nonsense-Correlations between Time-Series?- A Study in Sampling and the Nature of Time-Series

📚 Granger and Newbold (1974): Spurious Regressions in Econometrics

📚 Engle and Granger (1987): Co-Integration and Error Correction: Representation, Estimation, and Testing

---------------------------------------------------------------------------------------------------------

Time Stamps

Introduction 0:00

ECM Overview 0:37

Error Correction Term Details 1:48

Estimating the ECM 3:12

Long and Short Run Model 5:09

Model Diagnostics 7:30

In Sample Forecast 11:32

---------------------------------------------------------------------------------------------------------

✅ Interested in learning more?

🎬 EViews Course videos:

🎬 Stata Course videos:

---------------------------------------------------------------------------------------------------------

If you liked the video and would like more content, please support my channel subscribing!

👍Like and subscribe for more videos!

☕️ If you would like to show your appreciation and make a donation:

Thanks a lot!

0:14:03

0:14:03

Time Series: Error Correction Model explained in Eviews

0:10:02

0:10:02

Error correction model - part 1

0:06:11

0:06:11

Cointegration - an introduction

0:12:54

0:12:54

Econometrics - Cointegration and Error Correction Model

0:01:02

0:01:02

ARDL Eviews Long Run Short Run ECM Cointegration

0:11:22

0:11:22

The error correction model

0:12:15

0:12:15

R studio - Johanson Juselius Vector Error Correction Model for Multi Equilibria Timeseries Data

1:05:20

1:05:20

Lecture 23: Non-stationary, Cointegration and Error Correction Models

0:12:33

0:12:33

Introduction to the Vector Error Correction Model

0:05:00

0:05:00

R Studio - Learning Time Series Regression and Post Regression Diagnostics of ECM Model

0:16:19

0:16:19

Basics of Error Correction Equations in Time Series Data

0:26:21

0:26:21

Cointegration and Error Correction Model in Stata

0:04:25

0:04:25

10.8. Time Series Econometrics: Cointegration analysis

0:14:08

0:14:08

Time Series Analysis Cointegration and error correction model

0:02:59

0:02:59

Master Time Series Model Selection in Just 1 HOUR with VAR and VECM!

0:28:03

0:28:03

R Studio: Error Correction Model - Time Series Estimation Model Tutorial

0:10:38

0:10:38

(Stata13): Estimate ARDL and Error Correction Models #ardl #ecm #boundstest #cointegration #lags

0:07:38

0:07:38

Vector Auto Regression : Time Series Talk

0:10:07

0:10:07

Panel VECM

0:09:50

0:09:50

Estimation of the ADL and ECM Models for Stationary Time Series in OxMetrics

0:15:02

0:15:02

348 Cointegration and Error Correction Mechanism in Time Series using STATA

0:07:01

0:07:01

Error correction model - part 2

0:17:13

0:17:13

Analisis Error Correction Model (ECM) di Stata

1:32:25

1:32:25

Lecture 5: VAR and VEC Models

Комментарии