filmov

tv

What Is And How To Calculate The Units Of Production Method For Depreciation Explained

Показать описание

In this video we discuss what is the units of production method for depreciation and how to calculate the units of production method for depreciation

Transcript/notes (partial)

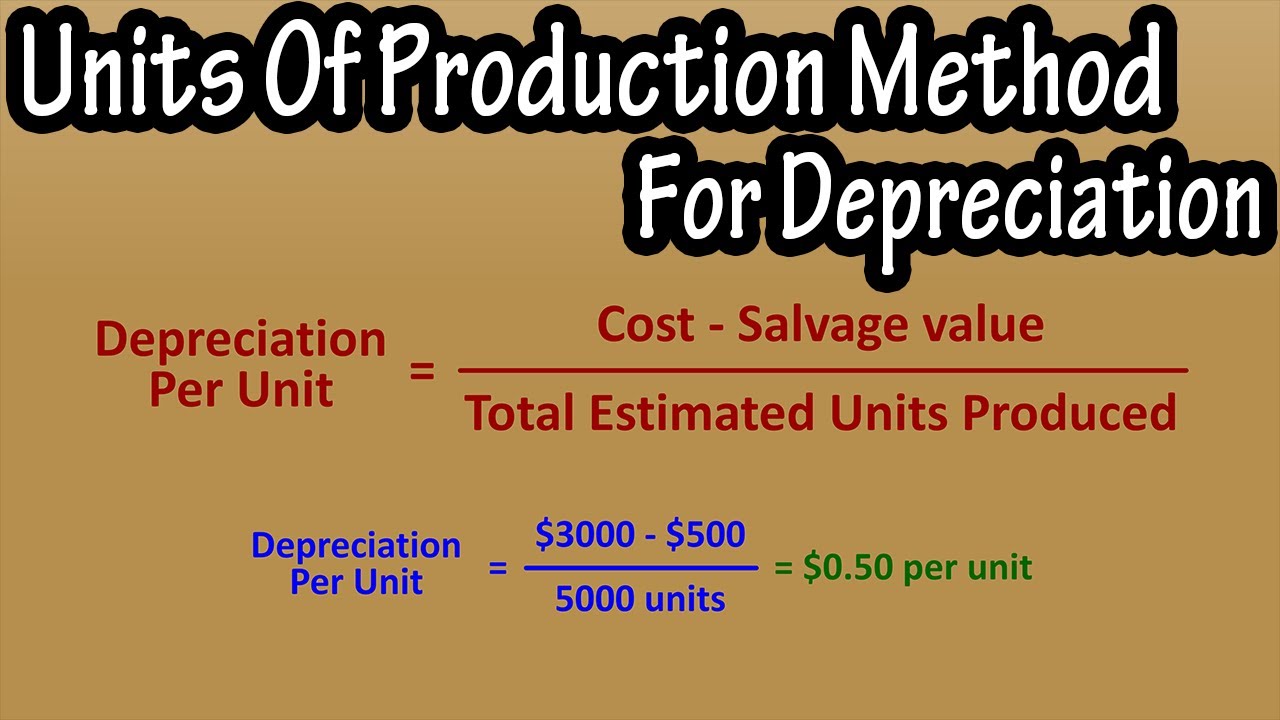

The units of production method for depreciation is based on how much a company uses the asset.

As an example, let’s say that a company purchases a piece of equipment for $3000, the useful life is 5 years, the salvage value is $500, and the company estimates that the asset has a useful life of 5000 units. Create a depreciation schedule for the asset.

In order to create the depreciation schedule we first must calculate the depreciation per unit, and the formula for that is, depreciation per unit equals, the cost of the asset minus the residual or salvage value, divided by the total estimated units produced.

From our example, plugging into the formula, we have $3000, the cost of the asset, minus $500, the salvage value, divided by 5000, the total estimated units produced over the useful life of the asset. And this calculates to 50 cents as the depreciation per unit.

Now we are going to create a depreciation schedule. And we are going to put 5 columns in it, end of year, units produced, depreciation expense for year, accumulated depreciation at end of year, and the book value at end of year. And one note about book value, the value in this column cannot go below the salvage value of the asset, which in this case is $500.

Here are the units produced over the 5 years of useful life of the asset.

At the end of year 1, the equipment produced 1200 units. So, we put in 1 in the end of year column, and 1200 in the 1st row of the units produced column. Next, we need to calculate the depreciation expense for year 1, and the formula for that is, depreciation amount equals, the depreciation per unit times the number of units produced. Plugging in, we have 50 cents, as we calculated that a moment ago, times 1200, the number of units produced. And this calculates to $600, so, that is the depreciation expense for year 1.

For the 4th column, accumulated depreciation at end of year, this is the total amount of depreciation accumulated at the end of each year. So, at the end of year 1, the total amount of depreciation will be the $600 we just calculated.

Now for the last column, the book value at end of year. This is the original cost of the asset minus the accumulated depreciation at the end of the year. So, the book value at the end of year 1 will be the original cost of $3000 minus the accumulated depreciation at end of year 1, $600. Which equals $2400.

For year 2 we put a 2 in the 1st column, and 1000 in the units produced column. The depreciation expense for year 2 is 50 cents, times the 1000 units produced, which equals $500. The accumulated depreciation at the end of year 2 will be the depreciation for year 1 and year 2, so, $600 plus $500, which is $1100. The book value at the end of year 2 will be $3000, the cost of the asset minus $1100, the accumulated depreciation, which equals $1900, and year 2 is complete.

Here are the numbers for years 3 and 4.

Now for end of year 5, and keep in mind that the book value at the end of year cannot go below the salvage value of $500. The units produced were 900, so we put that in. The depreciation expense will then be 50 cents times 900 units, which equals $450, the accumulated depreciation will be the depreciation for years 1 thru 4 plus the depreciation expense for year 5, $450, which equals $2650. And the book value will be $3000, the original cost of the asset minus $2650, the accumulated depreciation, which equals $350.

However, we cannot have a book value of $350. As stated earlier, the book value cannot go below $500. So, we need to make some changes to end of year 5, so that we have a final book value of $500. To do this, we start with the book value at the end of year that we ended up with, in this case $350. And we subtract that from the book value that we need to be at, which is $500. $500 minus $350 is $150.

Next we are going to use the depreciation amount formula we have been using, depreciation amount equals, the depreciation per unit times the number of units produced. There were 900 units produced in year 5, but, we can’t claim all of them, because as we just saw, that would bring the book value below the $500 salvage value, so we need to use the formula and this time solve for units produced.

Doing this by plugging into the formula, we have $150, the depreciation amount we need to be at, equals, 50 cents, our per unit depreciation, times units produced.

Chapters/Timestamps

0:00 What is the units of production method for depreciation?

0:11 Example of units of production method for depreciation

0:26 How to calculate depreciation per unit

0:59 Depreciation schedule/table set up

1:26 Numbers at end of year 1

2:34 Numbers at end of year 2

3:14 Numbers at end of year 5

3:55 Adjustment for book value at end of year 5

Transcript/notes (partial)

The units of production method for depreciation is based on how much a company uses the asset.

As an example, let’s say that a company purchases a piece of equipment for $3000, the useful life is 5 years, the salvage value is $500, and the company estimates that the asset has a useful life of 5000 units. Create a depreciation schedule for the asset.

In order to create the depreciation schedule we first must calculate the depreciation per unit, and the formula for that is, depreciation per unit equals, the cost of the asset minus the residual or salvage value, divided by the total estimated units produced.

From our example, plugging into the formula, we have $3000, the cost of the asset, minus $500, the salvage value, divided by 5000, the total estimated units produced over the useful life of the asset. And this calculates to 50 cents as the depreciation per unit.

Now we are going to create a depreciation schedule. And we are going to put 5 columns in it, end of year, units produced, depreciation expense for year, accumulated depreciation at end of year, and the book value at end of year. And one note about book value, the value in this column cannot go below the salvage value of the asset, which in this case is $500.

Here are the units produced over the 5 years of useful life of the asset.

At the end of year 1, the equipment produced 1200 units. So, we put in 1 in the end of year column, and 1200 in the 1st row of the units produced column. Next, we need to calculate the depreciation expense for year 1, and the formula for that is, depreciation amount equals, the depreciation per unit times the number of units produced. Plugging in, we have 50 cents, as we calculated that a moment ago, times 1200, the number of units produced. And this calculates to $600, so, that is the depreciation expense for year 1.

For the 4th column, accumulated depreciation at end of year, this is the total amount of depreciation accumulated at the end of each year. So, at the end of year 1, the total amount of depreciation will be the $600 we just calculated.

Now for the last column, the book value at end of year. This is the original cost of the asset minus the accumulated depreciation at the end of the year. So, the book value at the end of year 1 will be the original cost of $3000 minus the accumulated depreciation at end of year 1, $600. Which equals $2400.

For year 2 we put a 2 in the 1st column, and 1000 in the units produced column. The depreciation expense for year 2 is 50 cents, times the 1000 units produced, which equals $500. The accumulated depreciation at the end of year 2 will be the depreciation for year 1 and year 2, so, $600 plus $500, which is $1100. The book value at the end of year 2 will be $3000, the cost of the asset minus $1100, the accumulated depreciation, which equals $1900, and year 2 is complete.

Here are the numbers for years 3 and 4.

Now for end of year 5, and keep in mind that the book value at the end of year cannot go below the salvage value of $500. The units produced were 900, so we put that in. The depreciation expense will then be 50 cents times 900 units, which equals $450, the accumulated depreciation will be the depreciation for years 1 thru 4 plus the depreciation expense for year 5, $450, which equals $2650. And the book value will be $3000, the original cost of the asset minus $2650, the accumulated depreciation, which equals $350.

However, we cannot have a book value of $350. As stated earlier, the book value cannot go below $500. So, we need to make some changes to end of year 5, so that we have a final book value of $500. To do this, we start with the book value at the end of year that we ended up with, in this case $350. And we subtract that from the book value that we need to be at, which is $500. $500 minus $350 is $150.

Next we are going to use the depreciation amount formula we have been using, depreciation amount equals, the depreciation per unit times the number of units produced. There were 900 units produced in year 5, but, we can’t claim all of them, because as we just saw, that would bring the book value below the $500 salvage value, so we need to use the formula and this time solve for units produced.

Doing this by plugging into the formula, we have $150, the depreciation amount we need to be at, equals, 50 cents, our per unit depreciation, times units produced.

Chapters/Timestamps

0:00 What is the units of production method for depreciation?

0:11 Example of units of production method for depreciation

0:26 How to calculate depreciation per unit

0:59 Depreciation schedule/table set up

1:26 Numbers at end of year 1

2:34 Numbers at end of year 2

3:14 Numbers at end of year 5

3:55 Adjustment for book value at end of year 5

0:02:41

0:02:41

What is a “body double,” and how does it help?

0:10:44

0:10:44

Lawrence: What's happening in Los Angeles is a hurricane without rain. It is a hurricane with f...

0:00:39

0:00:39

What is dropshipping and how to start ☝️

0:07:12

0:07:12

What is an API and how does it work? (In plain English)

0:12:07

0:12:07

What Is Univibe and How To Use It!

0:15:36

0:15:36

What is an LLC and How Does It Work? 6 INCREDIBLE Benefits

0:07:17

0:07:17

What Is A Chord In Music? How To Build Chords and Chord Progressions

0:06:08

0:06:08

What Thermite is and How to Make it

0:01:09

0:01:09

What is title bar window shake in windows 11 and how to enable it

0:14:17

0:14:17

What even IS a 2-5-1 and how do you use it?

0:03:16

0:03:16

What is a Pomodoro and How Can it Help with ADHD?

0:04:20

0:04:20

What is a VPN and How Does it Work? [SHORT Video Explainer] ⏱️

0:05:45

0:05:45

Magnets for Kids | What is a magnet, and how does it work?

0:07:01

0:07:01

What Is A Guitar Riff - And How To Create One!

0:07:54

0:07:54

What Is a Stock and How Does It Work? (FOR ABSOLUTE BEGINNERS)

0:07:09

0:07:09

What Is A DI Box (Direct Box)? | When & How To Use One

0:05:08

0:05:08

What Are Cookies? And How They Work | Explained for Beginners!

0:20:51

0:20:51

What is a Contactor and How Does it Work?

0:04:57

0:04:57

Wildfire scientist on cause of Southern California wildfires

0:58:09

0:58:09

How to START a YouTube Channel in 2025: Beginners Guide to Growing From ZERO Subscribers!

0:10:05

0:10:05

What is a HomeLab and How Do I Get Started?

0:24:25

0:24:25

What is a stack and how does it work? — 6502 part 5

0:05:55

0:05:55

How To Turn 0 ROBUX Into 70,000 On Roblox.. (How To Get Free Robux 2025)

0:01:46

0:01:46

LA wildfires: Why the California fires are so intense

Комментарии