filmov

tv

Hyperparameter Optimization - The Math of Intelligence #7

Показать описание

Hyperparameters are the magic numbers of machine learning. We're going to learn how to find them in a more intelligent way than just trial-and-error. We'll go over grid search, random search, and Bayesian Optimization. I'll also cover the difference between Bayesian and Frequentist probability.

Noah's Winning Code:

Hammad's Runner-up Code:

More learning resources:

Join us in the Wizards Slack channel:

And please support me on Patreon:

Thanks to Veritasium (bayesian animation) & Angela Schoellig (drone clip)

Follow me:

Signup for my newsletter for exciting updates in the field of AI:

Noah's Winning Code:

Hammad's Runner-up Code:

More learning resources:

Join us in the Wizards Slack channel:

And please support me on Patreon:

Thanks to Veritasium (bayesian animation) & Angela Schoellig (drone clip)

Follow me:

Signup for my newsletter for exciting updates in the field of AI:

0:09:51

0:09:51

Hyperparameter Optimization - The Math of Intelligence #7

0:03:15

0:03:15

Hyperparameters Tuning: Grid Search vs Random Search

0:09:50

0:09:50

Bayesian Optimization (Bayes Opt): Easy explanation of popular hyperparameter tuning method

0:18:00

0:18:00

Bayesian Optimization - Math and Algorithm Explained

0:08:02

0:08:02

Hyperparameters Optimization Strategies: GridSearch, Bayesian, & Random Search (Beginner Friendl...

0:00:06

0:00:06

Hyperparameter Tuning in Machine Learning #education #artificialintelligence #programminglanguage

0:01:19

0:01:19

Parameters vs hyperparameters in machine learning

0:05:11

0:05:11

Hyperparameter Optimization

0:13:48

0:13:48

Minimizing Noise Cluster for Topic Modeling

0:05:11

0:05:11

5 - Hyperparameter Optimization

0:00:57

0:00:57

Hyperparameter Tuning for Improving Model Accuracy #ai #datascience #learnwithav #hyperparameter

0:43:54

0:43:54

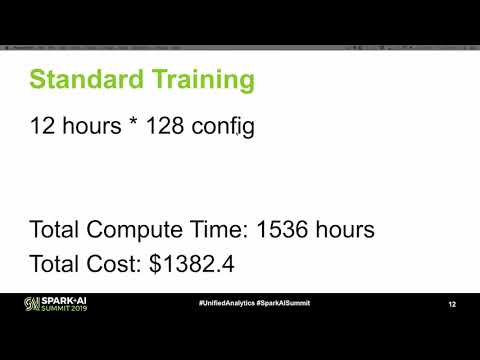

Advanced Hyperparameter Optimization for Deep Learning with MLflow - Maneesh Bhide Databricks

0:01:50

0:01:50

hyperparameter optimization techniques to improve your machine learning

0:01:51

0:01:51

hyperparameters optimization methods

0:00:31

0:00:31

The importance of hyperparameter optimization

0:12:41

0:12:41

8.1 Hyperparameter Optimization Motivation [Applied Machine Learning || Varada Kolhatkar || UBC]

0:09:28

0:09:28

Hyperparameter Optimization in Python

0:00:09

0:00:09

Finding the optimal hyperparameters using a high-level PSO

0:01:12

0:01:12

Hyperparameter Optimization with Keras

0:00:18

0:00:18

Machine Learning Engineer Interview Question: What is hyperparameter tuning and how you use it?

0:16:48

0:16:48

Hyper-Parameter Optimization

0:00:31

0:00:31

What is Hyperparameter tuning in machine learning #machinelearning #datascience

0:00:45

0:00:45

Bayesian Optimization - Explained #datascience #machinelearning #dataanlysis #statistics

0:00:25

0:00:25

Unlocking Faster Convergence with Bayesian Optimization! 🚀

Комментарии