filmov

tv

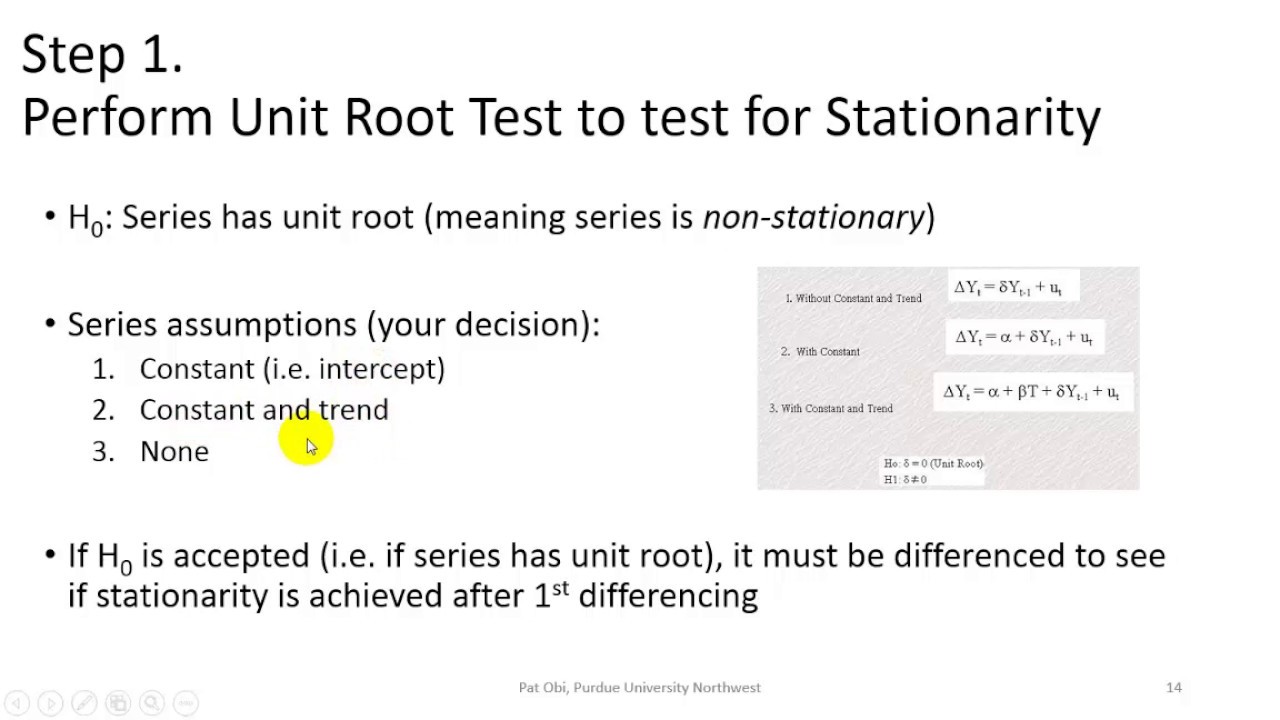

Unit Root Test - Step 1 of 4

Показать описание

Non-stationarity test for time series - EViews

0:13:53

0:13:53

Unit Roots : Time Series Talk

0:05:49

0:05:49

Dickey Fuller test for unit root

0:06:12

0:06:12

Unit Root Test - Step 1 of 4

0:03:23

0:03:23

Eviews: Unit Root Testing

0:23:57

0:23:57

Stata Tutorial: Basic Unit Root Test

0:11:00

0:11:00

Unit Root Test in EVIEWs

0:05:55

0:05:55

Unit root tests in Eviews - Stationarity

0:22:41

0:22:41

Unit Root, Stochastic Trend, Random Walk, Dicky-Fuller test in Time Series

0:12:49

0:12:49

Time Series Analysis: Why are Unit Roots Important?

0:13:32

0:13:32

STATA Tutorial: Time Series Data Analysis Step 1: Unit root test, lag length selection

0:09:39

0:09:39

Time Series Talk : Augmented Dickey Fuller Test + Code

0:12:41

0:12:41

(Stata13):Perform Augmented Dickey-Fuller Test, Stationarity #adf #pp #stationarity #integration

0:05:50

0:05:50

10.7. Time Series Econometrics: Unit root testing

0:11:23

0:11:23

(EViews10):Augmented Dickey-Fuller Test, Stationarity #adf #pp #stationarity #integration

0:06:11

0:06:11

All Unit Root Test in Eviews

0:12:04

0:12:04

(Stata13): Perform Panel ARDL Estimations (Steps 1 to 4) #ardl #paneldata #pedronitest #panelardl

0:05:44

0:05:44

5.1: Unit root testing using RStudio

0:17:03

0:17:03

EViews: Unit Root Test, Cointegration Test and ARDL-ECM (Estimation and Interpretation)

0:04:24

0:04:24

Unit Roots with Breakpoints

0:17:28

0:17:28

Unit Roots and Tests for Non-Stationarity

0:15:01

0:15:01

STATA Tutorial: How to conduct Unit Root Test for panel data using STATA

0:02:02

0:02:02

Unit Root Testing using Excel Dickey Fuller Test using Excel

0:06:41

0:06:41

PEQ 3043: ADF Unit Root Test Procedure

0:15:33

0:15:33

RANDOM WALK | UNIT ROOT | DICKEY-FULLER TEST

Комментарии