filmov

tv

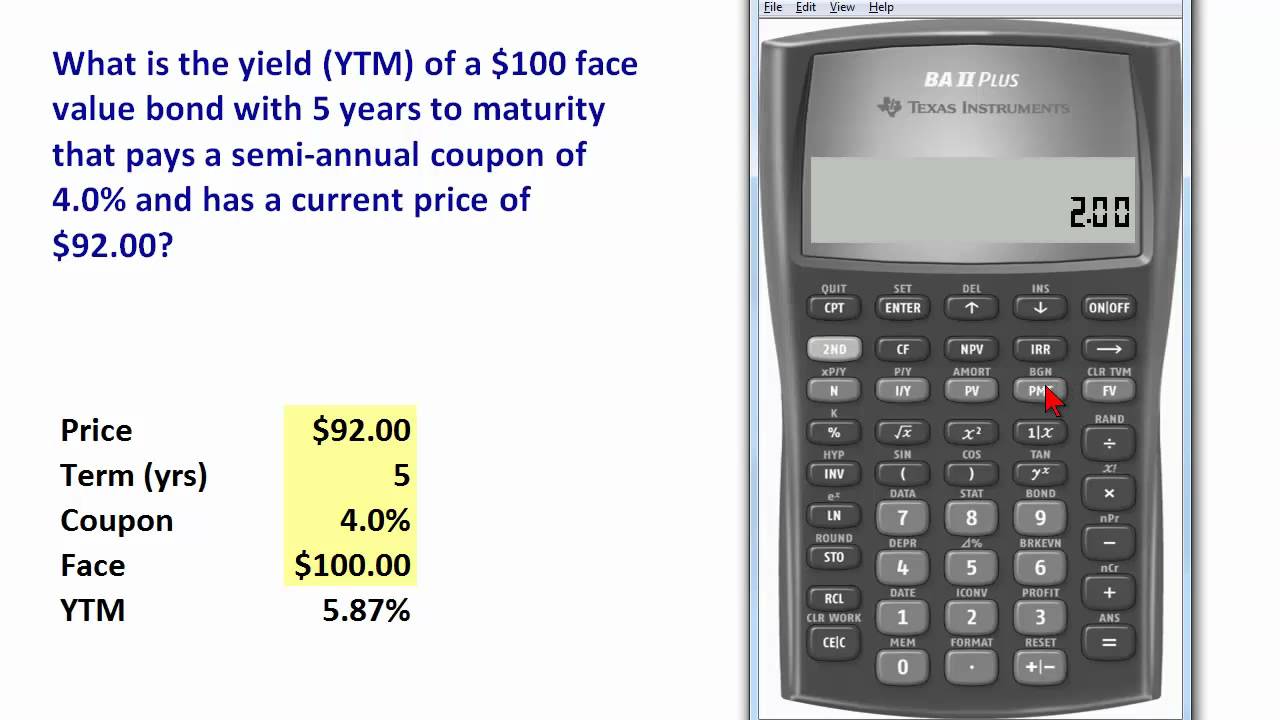

FRM: TI BA II+ to compute bond yield (YTM)

Показать описание

0:01:42

0:01:42

Which Calculator to choose for CFA/FRM exams?

0:34:50

0:34:50

How to use calculator in CFA and FRM | BA II Plus Calculator Tutorial

0:09:22

0:09:22

FRM: TI BA II+ to compute bond yield (YTM)

0:08:03

0:08:03

FRM: TI BA II+ to price a bond

0:00:11

0:00:11

BA 2 PLUS FINANCIAL CALCULATOR. #frm #cfa #shorts

0:01:53

0:01:53

Texas Instruments BA II Plus Tutorial for CFA and FRM - Square root function

0:01:00

0:01:00

Setting Up the Texas BA II Plus Financial Calculator for the CFA Exam

0:03:25

0:03:25

Texas Instruments BA II Plus Tutorial for CFA and FRM - Annuity Calculations!

0:03:56

0:03:56

Set up Texas instruments ba ii plus calculator for CFA FRM and other exams

0:06:56

0:06:56

Setting Up the Texas Instruments BA II Financial Calculator (CFA, MBA, FRM)

0:04:25

0:04:25

How to Calculate Future Value and Present Value with BA II Plus Calculator by Texas Instruments

0:02:59

0:02:59

BAII Plus Calculator - Finding Mean & Standard Deviation

0:12:33

0:12:33

Solving Statistical Problems with Texas Instruments BA II Calculator (CFA, MBA, FRM)

0:17:33

0:17:33

Basic Calculations with Texas Instruments BA II Financial Calculator (CFA, MBA, FRM)

0:08:16

0:08:16

Solving Cash Flows Problems with Texas Instruments BA II Calculator (CFA, MBA, FRM)

0:03:32

0:03:32

Texas Instruments BA II Plus Tutorial for CFA and FRM - How to format your calculator

0:01:09

0:01:09

Introduction to Texas Instruments BA II Financial Calculator (CFA, MBA, FRM)

0:05:06

0:05:06

Texas BA II Plus Financial Calculator: ICONV - Calculate Effective Annual Rate (EAR)

0:01:21

0:01:21

Texas Instruments BA II Plus Tutorial for CFA and FRM - Reset the calculator to factory settings

0:35:30

0:35:30

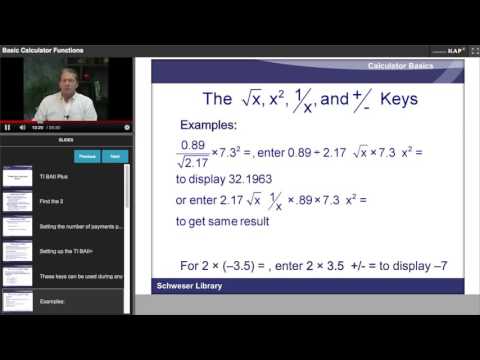

TI BAII Plus Calculator Basics for the CFA Exam

0:03:02

0:03:02

Texas Instruments BA II Plus Tutorial for CFA and FRM - Annuity Due

0:53:47

0:53:47

TI BA II Plus Professional Calculator Guide | FRM | CFA

0:04:24

0:04:24

Texas Instruments BA II Plus Tutorial for CFA and FRM - How to Use PMT Button from TVM row

0:02:37

0:02:37

How to use e on the BA II Plus Financial Calculator

Комментарии