filmov

tv

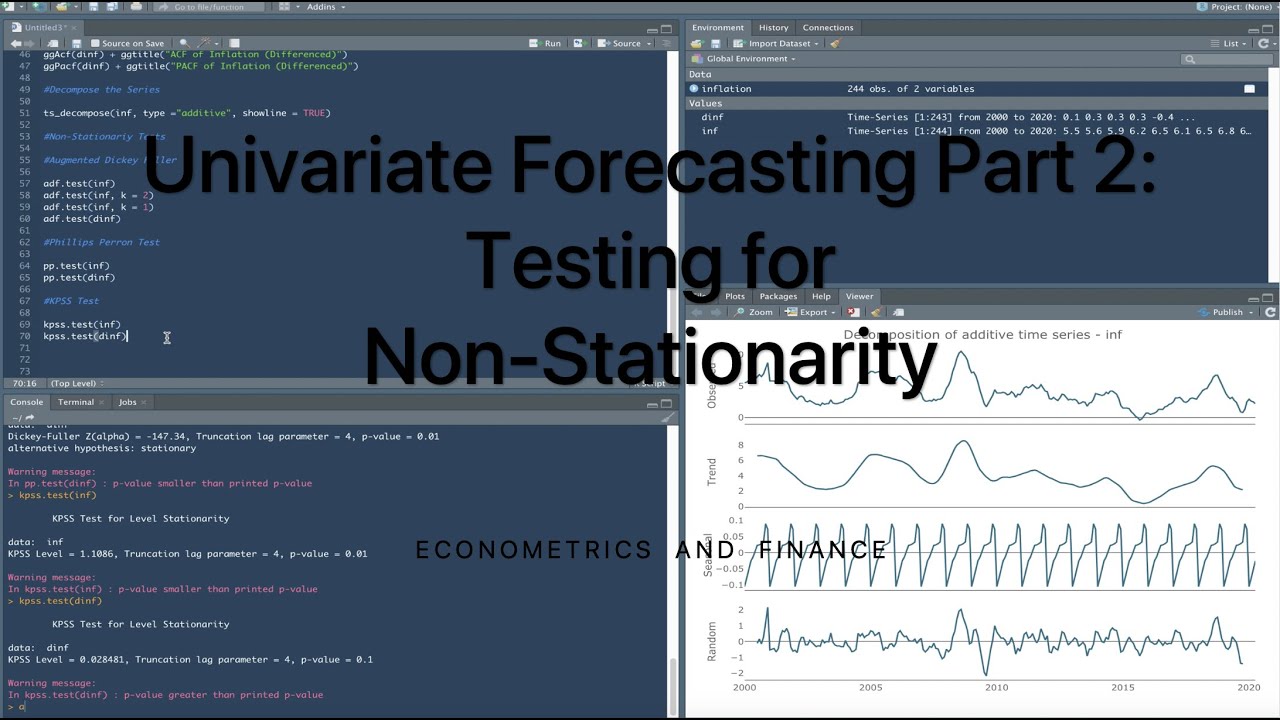

Testing for Non-Stationarity in R

Показать описание

In the second part of the series, we will be testing for non-stationarity using the Augmented Dickey-Fuller, the Phillips Perron Test, and the KPSS test.

Codes and Dataset are in here:

Created by Justin S. Eloriaga

Codes and Dataset are in here:

Created by Justin S. Eloriaga

0:07:46

0:07:46

Testing for Non-Stationarity in R

0:06:06

0:06:06

Testing stationarity by ADF Test

0:11:26

0:11:26

STATIONARITY IN R SOFTWARE

0:06:24

0:06:24

Transforming non-stationary data to stationary data by log returns and differencing in R Studio

0:09:39

0:09:39

Time Series Talk : Augmented Dickey Fuller Test + Code

0:07:16

0:07:16

S3 L1 Convert Non Stationary datasets to stationary datasets

0:17:28

0:17:28

Unit Roots and Tests for Non-Stationarity

0:07:57

0:07:57

The qualitative difference between stationary and non-stationary AR(1)

0:02:54

0:02:54

8.7: The KPSS test for time series stationarity in R

0:00:55

0:00:55

How Can I Identify Stationarity and Nonstationarity in R?

0:25:30

0:25:30

Lecture 25B: Models for Linear Non stationary Processes -6 (with R Demonstrations)

0:37:55

0:37:55

Time Series ARIMA model Using R | Stationarity | Non Stationarity

0:23:29

0:23:29

Tests for Non Stationarity (II)

0:04:35

0:04:35

ADF Test in R using urca Package

0:03:44

0:03:44

How to perform augmented dickey fuller test in R

0:11:08

0:11:08

Unit Root Test (or stationarity) For Panel Data in R

0:05:56

0:05:56

Stationary test in Rstudio/ADF & PP test

0:34:00

0:34:00

Tests for Non Stationarity

0:27:22

0:27:22

Stationary and nonstationary series, tools to determine ARMA models with R using Quarto

0:07:13

0:07:13

Estimating Panel Quantile ARDL with Cointegration in R for Non-Stationary Non-Normal & Outlier d...

0:06:44

0:06:44

Stationarity Test (ADF (Augmented Dickey-Fuller) Test) In R software

0:09:13

0:09:13

Stationarity & Seasonality| Time Series Forecasting #1|

0:10:35

0:10:35

How to Use ACF and PACF to Identify Time Series Analysis Models

0:28:58

0:28:58

Lecture 24A: Models for Linear Non stationary Processes -3 (with R Demonstrations)

Комментарии