filmov

tv

Portfolio of four assets: Optimization with Solver

Показать описание

#portfolioanalysis

Optimizing a portfolio of multiple assets in Excel using Solver

Optimizing a portfolio of multiple assets in Excel using Solver

0:15:53

0:15:53

Portfolio of four assets: Optimization with Solver

0:08:46

0:08:46

Calculating the Optimal Portfolio in Excel | Portfolio Optimization

0:15:02

0:15:02

Portfolio Optimization with 4 Stocks - Part 1

0:35:01

0:35:01

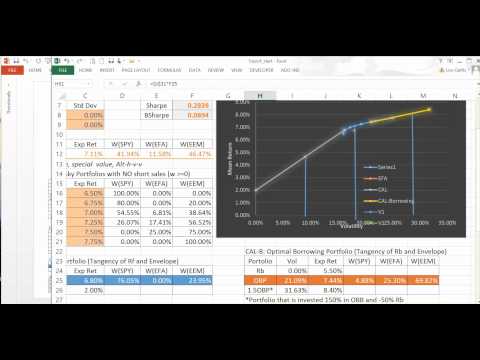

Four Stock Portfolio and Graphing Efficient Portfolio Frontier

0:17:10

0:17:10

Portfolio Optimization Seven Security Example with Excel Solver

0:15:07

0:15:07

Portfolio Optimization in Excel: Step by Step Tutorial

0:13:33

0:13:33

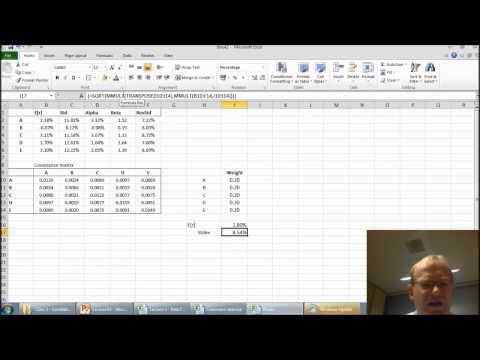

Portfolio of four assets: Variance-Covariance Matrix

0:17:02

0:17:02

Portfolio Optimization using Solver in Excel

0:11:53

0:11:53

The Shocking Financial Secrets of the Japanese Revealed

0:06:43

0:06:43

The Asset Investment Portfolio Optimization Problem

0:10:18

0:10:18

The Power of Portfolio Optimization

0:06:33

0:06:33

Mulplei Asset Portfolio Problem: optimization

0:07:42

0:07:42

Portfolio Optimization with 4 Stock Part 2

0:34:52

0:34:52

Modern Portfolio Concepts Part 4: Portfolio Optimization with MPT

0:31:12

0:31:12

Math 4.03 Portfolio Optimization with 3 assets using Excel Solver

0:17:36

0:17:36

Portfolio Optimization using five stocks in excel | FIN-ED

0:13:09

0:13:09

Minimum Variance Portfolio in Excel: Multi-asset case

0:20:42

0:20:42

Math 4.02 Portfolio optimization with 2 assets using Excel

0:27:02

0:27:02

Portfolio Optimization

0:06:22

0:06:22

Optimal portfolios with Excel Solver

0:15:02

0:15:02

Portfolio Optimization with 4 Stock - Part 3 - Adding CML Line

0:21:51

0:21:51

Portfolio Optimization in Excel Using Solver

0:52:38

0:52:38

FinMod 4 Portfolio Optimization

0:07:13

0:07:13

9. Portfolio Optimization using five stocks in excel: CALCULATING COVARIANCE MATRIX

Комментарии