filmov

tv

CS-AR1 Lecture 3 - Recap on Nested Form (Advanced Ruby/Rails)

Показать описание

Harley Trung

Рекомендации по теме

0:58:02

CS-AR1 Lecture 3 - Recap on Nested Form (Advanced Ruby/Rails)

0:54:12

CS-AR1 Lecture 3 - User Access Control (Advanced Ruby/Rails)

0:15:51

1 3 AR1 wtih R

0:00:20

1st yr. Vs Final yr. MBBS student 🔥🤯#shorts #neet

0:25:39

Lag Operator & AR(p) Stationarity

0:05:11

What is the Vector Autoregressive (VAR) Model

0:00:30

Example Video - Introduction Video for Applications

1:18:06

CS-AR1: Advanced Ruby/Rails Lecture 2

0:05:01

What are Autoregressive (AR) Models

0:17:33

Autocorrelation

0:09:33

Set -1 Problems on AR & MA

0:06:02

02417 Lecture 12 part G: AR(1) with observation noise

0:04:34

Smoothing 3: Differencing

0:08:14

ARMA Time Series Models

0:07:55

Solving Yule-Walker equations for AR(1)

0:04:06

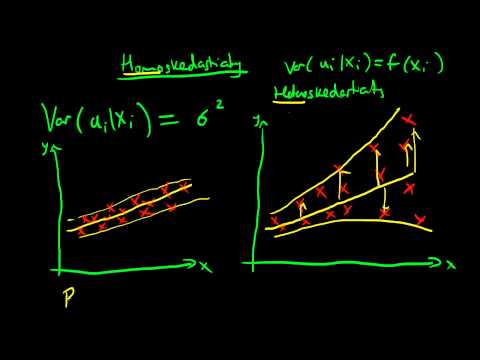

Heteroskedasticity summary

0:10:35

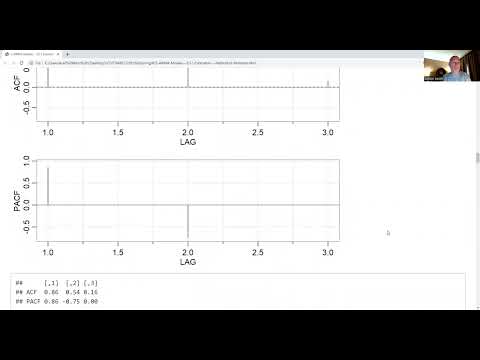

How to Use ACF and PACF to Identify Time Series Analysis Models

0:33:27

3 ARIMA Models - 3.5.1 Estimation - Method of Moments

0:07:16

S3 L1 Convert Non Stationary datasets to stationary datasets

0:14:45

2 3 Time Series with a Trend

0:40:06

ECE 302 Lecture A.3 Autocorrelation Function

0:01:45

Interpreting the ACF and PACF charts in Alteryx's TS Plot tool

0:09:13

Stationarity & Seasonality| Time Series Forecasting #1|

0:21:08

AR Model Revisited

0:58:02

0:58:02

0:54:12

0:54:12

0:15:51

0:15:51

0:00:20

0:00:20

0:25:39

0:25:39

0:05:11

0:05:11

0:00:30

0:00:30

1:18:06

1:18:06

0:05:01

0:05:01

0:17:33

0:17:33

0:09:33

0:09:33

0:06:02

0:06:02

0:04:34

0:04:34

0:08:14

0:08:14

0:07:55

0:07:55

0:04:06

0:04:06

0:10:35

0:10:35

0:33:27

0:33:27

0:07:16

0:07:16

0:14:45

0:14:45

0:40:06

0:40:06

0:01:45

0:01:45

0:09:13

0:09:13

0:21:08

0:21:08