filmov

tv

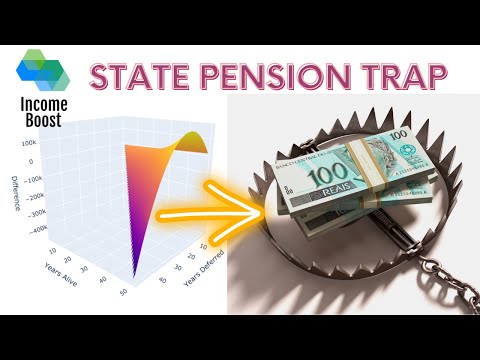

How the UK govt TRAPS pensioners!

Показать описание

Explore whether pension deferral is beneficial in the UK and the US. Understand why deferring your pension might make you financially worse off, and learn strategies to avoid this potential trap.

Video related Links:

Sources used in the video:

US GOVT:

UK GOVT:

========================================================

– – – My personal finance calculators: – – –

– – – Coding and Software: – – –

My personal finance calculators were built purely through Python with ZERO prior knowledge. I believe Python is the best programming language for beginners to learn. If I can do it, you can do it!

If you want to know more about what I actually use to do video animation, editing and coding, follow the links below:

– – – Support & Affiliate Links: – – –

– – – Let’s Connect: – – –

– – – Disclaimer: – – –

This video does not constitute financial or legal advice and merely represents the opinion of the creator.

Links included in this description include affiliate links. If you purchase a product or service with the links that I provide, I may receive a small commission. There is no additional charge to you! Thank you for supporting me so I can continue to provide you with free content each week!

Video related Links:

Sources used in the video:

US GOVT:

UK GOVT:

========================================================

– – – My personal finance calculators: – – –

– – – Coding and Software: – – –

My personal finance calculators were built purely through Python with ZERO prior knowledge. I believe Python is the best programming language for beginners to learn. If I can do it, you can do it!

If you want to know more about what I actually use to do video animation, editing and coding, follow the links below:

– – – Support & Affiliate Links: – – –

– – – Let’s Connect: – – –

– – – Disclaimer: – – –

This video does not constitute financial or legal advice and merely represents the opinion of the creator.

Links included in this description include affiliate links. If you purchase a product or service with the links that I provide, I may receive a small commission. There is no additional charge to you! Thank you for supporting me so I can continue to provide you with free content each week!

0:06:11

0:06:11

How the UK govt TRAPS pensioners!

0:04:03

0:04:03

Britain stuck in a slow-growth trap, former UK business secretary says

0:04:27

0:04:27

The Great British Debt Trap!

0:04:35

0:04:35

The UK Pension Trap Is Snapping Shut

0:03:24

0:03:24

The GOP Must Avoid This Trap | What's Ahead

0:02:03

0:02:03

The Calorie Reduction Trap: Government Good Intentions

0:00:48

0:00:48

Tory MP's Honey Trap Scandal Explained

0:04:46

0:04:46

Why is it so hard to escape poverty? - Ann-Helén Bay

0:08:44

0:08:44

Tory Tax Trap for Pensioners

0:04:50

0:04:50

UK Income Tax System Exposed! | Personal Allowance Trap | 60% Marginal Tax Explained

0:04:38

0:04:38

UK Government 2019 Tax Trap

0:05:37

0:05:37

Reeves 'Could Trigger A Liz Truss Moment' By Changing UK Fiscal Rules

0:08:08

0:08:08

CANZUK: the post-Brexit opportunities and trap doors

0:01:25

0:01:25

#Brexit Checks Shelved Again on EU Imports. Brexit Is An Inflation Trap!

0:03:30

0:03:30

The Poverty Trap

0:00:16

0:00:16

THINK! Activate Pint Block - Wrap Trap

0:13:00

0:13:00

DON'T Fall for Poverty Trap - Do This Instead!

1:28:11

1:28:11

The Post-history of Brexit: Britain's Growth Trap and the Limits of Economic Strategy post-Brex...

0:00:17

0:00:17

Wales Will Ban Snaring and Glue Traps #shorts

0:07:41

0:07:41

Is Brexit Trapping the UK Economy in No Man's Land?

0:01:01

0:01:01

Poison Free Rat Trap

0:10:37

0:10:37

General Election Polls and Analysing Tory's 'Tax Trap: Labour's 18 Tax Rises'

1:01:29

1:01:29

Charles Moore on the woke “assault” on Britain, abolishing history & fighting back | Off Script...

0:13:45

0:13:45

Can Labour Avoid Brexit Traps?

Комментарии