filmov

tv

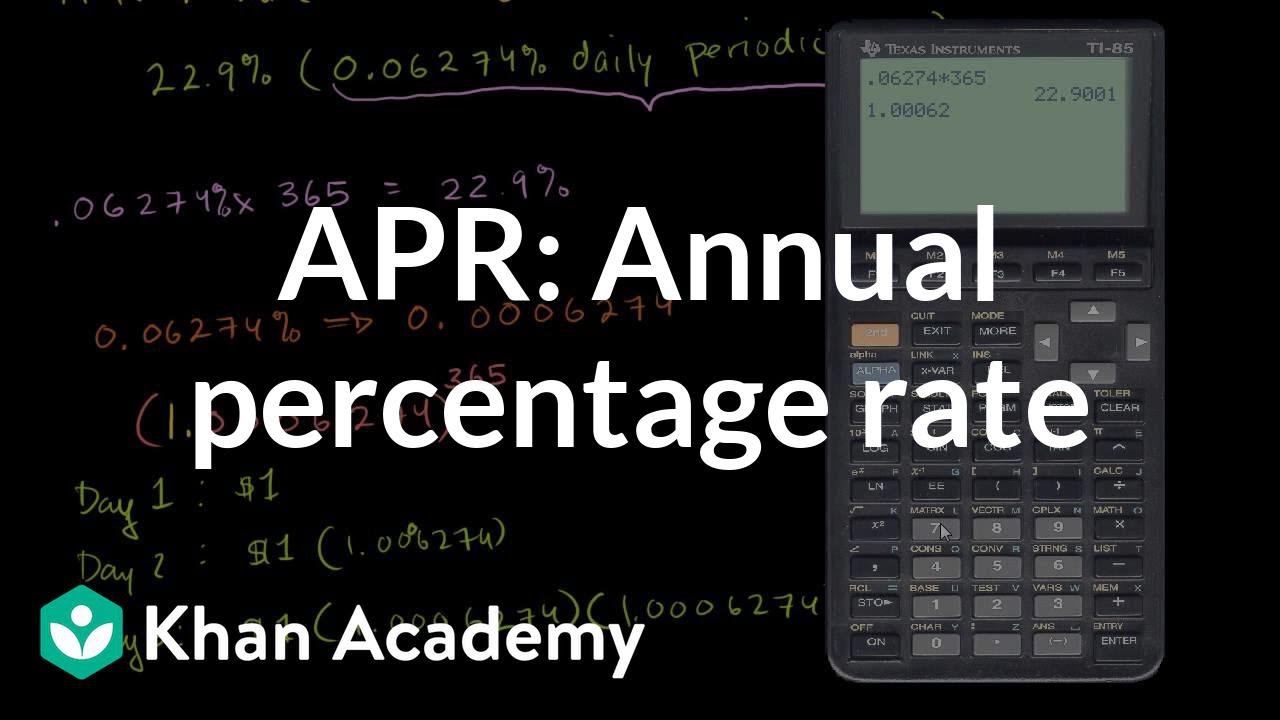

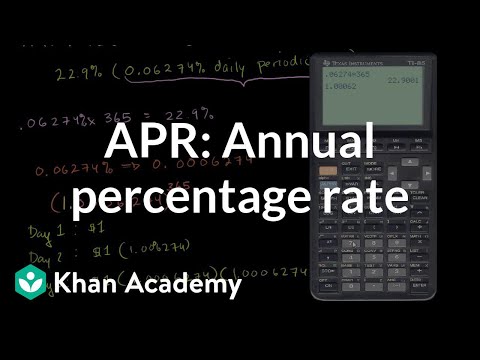

Annual Percentage Rate (APR) and effective APR | Finance & Capital Markets | Khan Academy

Показать описание

The difference between APR and effective APR. Created by Sal Khan.

Watch the next lesson:

Finance and capital markets on Khan Academy: Most of us have borrowed to buy something. Credit cards, in particular, can be quite convenient (but dangerous if not used in moderation). This tutorial explains credit card interest, how credit card companies make money and a far more silly way of borrowing money called "payday" loans.

About Khan Academy: Khan Academy offers practice exercises, instructional videos, and a personalized learning dashboard that empower learners to study at their own pace in and outside of the classroom. We tackle math, science, computer programming, history, art history, economics, and more. Our math missions guide learners from kindergarten to calculus using state-of-the-art, adaptive technology that identifies strengths and learning gaps. We've also partnered with institutions like NASA, The Museum of Modern Art, The California Academy of Sciences, and MIT to offer specialized content.

For free. For everyone. Forever. #YouCanLearnAnything

0:07:12

0:07:12

Annual Percentage Rate (APR) and effective APR | Finance & Capital Markets | Khan Academy

0:02:36

0:02:36

What Is APR (Annual Percentage Rate)?

0:01:04

0:01:04

What is APR on a Credit Card? | Discover | Card Smarts

0:13:24

0:13:24

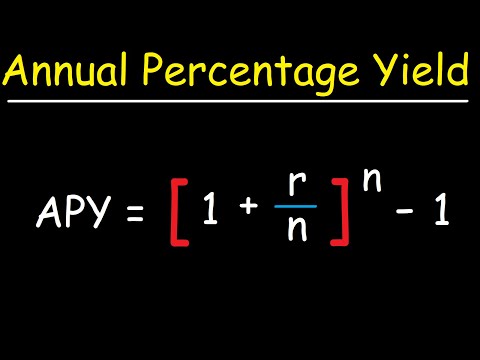

Annual Percentage Rate vs Annual Percentage Yield

0:04:45

0:04:45

The difference between APR and Interest Rate

0:08:56

0:08:56

APR and EAR Differences and Calculation (Intermediate Accounting I #7)

0:04:54

0:04:54

Calculating APR, Part 1 | Personal Finance Series

0:02:35

0:02:35

What Is Annual Percentage Rate (APR)? | Financial Terms

0:03:04

0:03:04

Anuncian millonaria inversión para infraestructura en APR en La Araucanía

0:01:18

0:01:18

SEAT - Car Finance Made Simple - Annual Percentage Rate (APR)

0:06:32

0:06:32

Annual Percentage Rate(APR)

0:04:35

0:04:35

Explaining APR vs. EAR | Annual Percentage Rate vs. Effective Annual Rate | Finance 101

0:00:41

0:00:41

Interest Rate vs APR

0:01:55

0:01:55

APR | Annual Percentage Rate | Helpful Animation Video | Your Online Finance Dictionary

0:04:23

0:04:23

Annual Percentage Rate or APR Explained with Example

0:01:17

0:01:17

Volkswagen – Car Finance Made Simple – Annual Percentage Rate (APR)

0:01:54

0:01:54

APR vs. APY: What’s the Difference?

0:03:18

0:03:18

What is APR or Annual Percentage Rate? A Simple Explanation for Kids and Beginners

0:02:30

0:02:30

Annual Percentage Rate APR vs Interest Rate: A Simple Explanation for Kids and Beginners

0:02:34

0:02:34

APR vs. Interest Rate: What You Need to Know

0:02:17

0:02:17

Car Loans - What's the difference between an Interest Rate & APR?

0:00:37

0:00:37

Have you ever wondered what APY and APR mean? #shorts

0:00:37

0:00:37

What is APR (Annual Percentage Rate)?

0:00:45

0:00:45

What is APR? (Annual Percentage Rate)

Комментарии