filmov

tv

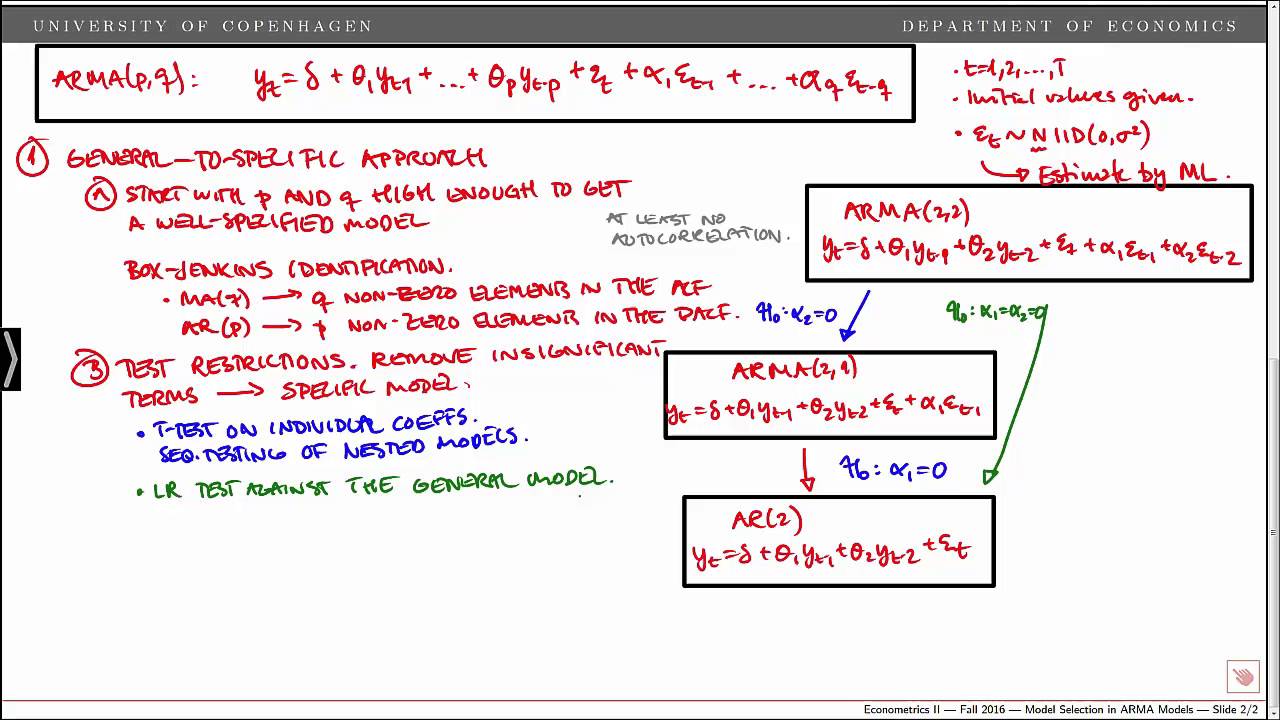

Model Selection in Autoregressive Moving Average (ARMA) Models

Показать описание

In the video we discuss the properties of the moving average process with q lags, MA(q). We explain how to derive the unconditional mean, variance, and autocovariances of the process. We derive an expression for the autocorrelation function and show that the process has a memory of exactly q periods.

0:09:04

0:09:04

Model Selection in Autoregressive Moving Average (ARMA) Models

0:05:01

0:05:01

What are Autoregressive (AR) Models

0:08:54

0:08:54

Time Series Talk : Autoregressive Model

0:05:11

0:05:11

What is the Vector Autoregressive (VAR) Model

0:09:42

0:09:42

Time Series Model Selection (AIC & BIC) : Time Series Talk

0:03:22

0:03:22

ARIMA models: Information criteria for model selection (Part 7)

0:45:06

0:45:06

Fitting and Selecting ARIMA models

0:07:38

0:07:38

Vector Auto Regression : Time Series Talk

0:12:29

0:12:29

Video # || 356 || Automatic Model Selection || Using Simulated Data in Eviews

0:13:38

0:13:38

02417 Lecture 6 part B: Identifying order of ARIMA models

0:10:28

0:10:28

Lesson 27f Time-Series: ARIMA

0:14:02

0:14:02

AR and MA models in EViews

0:18:32

0:18:32

Model Selection for Time Series

0:07:12

0:07:12

Time Series Talk : ARMA Model

0:05:07

0:05:07

What are ARIMA Models

0:45:52

0:45:52

02417 Lecture 10 part A: Marima package in R for multivariate ARMA models

0:23:49

0:23:49

ARIMA Model Parameter Selection

0:18:55

0:18:55

Model Selection

0:24:45

0:24:45

Eviews PC Lab Tutorial (model selection/estimation)

0:03:07

0:03:07

ARIMA Modeling

0:20:14

0:20:14

Model selection: Information criteria

0:59:29

0:59:29

ATSA21 Lecture 14: Multi-model inference and selection

0:10:51

0:10:51

Model Selection in ARMA using Information Criteria

0:31:11

0:31:11

5 1 Introduction to Dynamic Regression

Комментарии