filmov

tv

Optimising Your Stocks & Shares ISA

Показать описание

In the UK we have two primary tax-efficient savings vehicles: ISAs and SIPPs. In this video, I’ll show you how the two actually work very well together and how you can use ISAs both before and after retirement to provide flexibility and boost your income in a tax-efficient way.

Capital at risk. InvestEngine (UK) Limited is Authorised and Regulated by the Financial Conduct Authority (FRN: 801128)

This video is for educational purposes only and is not financial advice. If you need financial advice then please seek the help of an independent financial adviser.

Timestamps

0:00 Introduction

0:35 Types of ISA

1:50 Changes In The ISA Rules for 2024

3:17 Benefits of an ISA

4:30 Pre-Retirement Benefits & Contrasts With A SIPP

5:54 Illustration of Tax Efficiency of SIPP vs ISA

6:51 ISA vs SIPP fees

7:36 What To Invest In A SIPP

8:41 Complex So Advice or Our Membership May Help

9:40 Benefits of Combining an ISA & SIPP in Retirement

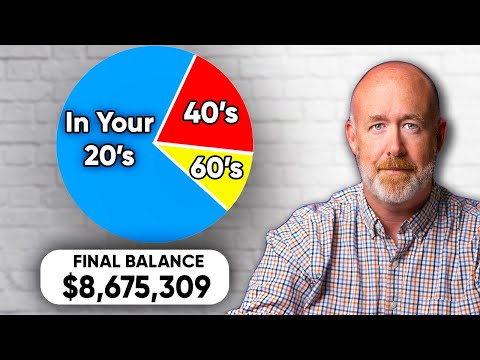

11:01 Illustration of ISA Growth and Income It Can Generate

12:58 Inheritance of ISAs and SIPPs

What Else PensionCraft Offers:

I Use The Following Data Sources To Help Me Create My Videos

(These links provide new users with a special offer and may also provide me with a small commission)

Where Else You Can Find Me

Take A Look At Some Of My Other Videos & Playlists

DISCLAIMER

All information is given for educational purposes and is not financial advice. Ramin does not provide recommendations and is not responsible for investment actions taken by viewers. Figures that are quoted refer to the past and past performance is not a reliable indicator of future results.

Capital at risk. InvestEngine (UK) Limited is Authorised and Regulated by the Financial Conduct Authority (FRN: 801128)

This video is for educational purposes only and is not financial advice. If you need financial advice then please seek the help of an independent financial adviser.

Timestamps

0:00 Introduction

0:35 Types of ISA

1:50 Changes In The ISA Rules for 2024

3:17 Benefits of an ISA

4:30 Pre-Retirement Benefits & Contrasts With A SIPP

5:54 Illustration of Tax Efficiency of SIPP vs ISA

6:51 ISA vs SIPP fees

7:36 What To Invest In A SIPP

8:41 Complex So Advice or Our Membership May Help

9:40 Benefits of Combining an ISA & SIPP in Retirement

11:01 Illustration of ISA Growth and Income It Can Generate

12:58 Inheritance of ISAs and SIPPs

What Else PensionCraft Offers:

I Use The Following Data Sources To Help Me Create My Videos

(These links provide new users with a special offer and may also provide me with a small commission)

Where Else You Can Find Me

Take A Look At Some Of My Other Videos & Playlists

DISCLAIMER

All information is given for educational purposes and is not financial advice. Ramin does not provide recommendations and is not responsible for investment actions taken by viewers. Figures that are quoted refer to the past and past performance is not a reliable indicator of future results.

0:14:12

0:14:12

Optimising Your Stocks & Shares ISA

0:00:29

0:00:29

How To Optimise Your Trading Strategy In 2025 🔥

0:16:09

0:16:09

Is Your Portfolio Optimized for Your Age? The Perfect Strategy And Portfolio

0:16:36

0:16:36

5 must-dos to sharpen your portfolio now! | Strategies to optimise your investment portfolio in 2024

0:11:18

0:11:18

5 Expert Tips to Optimize Your Investment Portfolio

0:03:43

0:03:43

How to Optimize Your Trading Performance

0:11:35

0:11:35

How to Optimize Your Stock Portfolio with Python: Boost Returns & Lower Risk

0:05:02

0:05:02

How do investors choose stocks? - Richard Coffin

0:08:29

0:08:29

Best Stocks to Buy: Nvidia Stock vs. Apple Stock vs. Google Stock vs. Microsoft Stock

0:16:55

0:16:55

How to Optimize Your Portfolio for Maximum Returns | VectorVest

1:26:28

1:26:28

5 Steps to Optimize the Performance of Your Stock Portfolio

0:00:14

0:00:14

How to Optimize Your Day Trades | Stock Market Trading Tips

0:30:44

0:30:44

Optimize Your Stock Portfolio With Python

0:09:56

0:09:56

How to Optimize your Portfolio Faster and Better from the Stock Market Crash?

0:22:33

0:22:33

How To Optimize Your Trading From Day 1

0:15:28

0:15:28

How to Optimize Research with a Stock Screener

0:00:52

0:00:52

3 Ways to Optimize Your Portfolio!! #anujgupta #taginvestments #portfoliomanagement

0:00:49

0:00:49

Optimizing Your Retirement Savings Strategy: The Power of Asset Allocation

0:06:08

0:06:08

Optimizing Your Stock Investing through Elimination

0:00:57

0:00:57

AI Optimized GG Shot Indicator, most accurate buy sell Indicator Tradingview.

0:00:46

0:00:46

#CHR/USDT - 30m | AI Optimized Strategy, most accurate buy sell indicator, Tradingview.#crypto

0:19:46

0:19:46

How to optimize your trades for bigger monthly gains

0:00:59

0:00:59

Maximize or Optimize Your Investment Strategy? A mental guide for investors choosing ETFs or Stocks

0:00:53

0:00:53

Optimize Your Stock Options with @AlisonWealth: The ISO Exercise Sweet Spot for AMT

Комментарии