filmov

tv

Linear Regression: Time Series Analysis

Показать описание

Linear Regression: Time Series Analysis

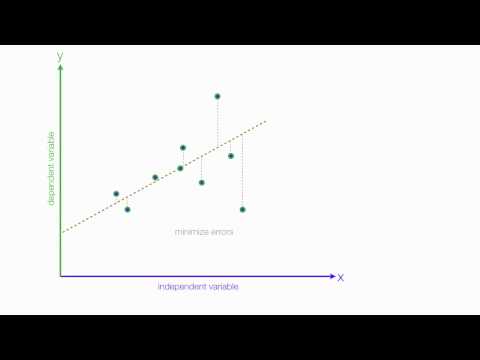

Hi everyone! This is a quick and simple Time Series: Linear Regression analysis - Output interpretation in Eviews. Learn how to estimate a simple linear regression and how to interpret the linear regression output results - how to estimate and interpret ols!

Summary of the video: Using real GDP data for Argentina and Brazil, I show you how to estimate a linear regression in eviews and how to interpret the regression estimation output. Estimate the linear regression yourself and obtain the linear regression results by downloading the data in the description. I hope you enjoy it!

📈 Download the dataset for free and replicate the content of the video:

✅ Visit my website to see all my FREE tutorials:

☕️ If you value my content and would like to show a recognition, you can make a donation:

---------------------------------------------------------------------------------------------------------

🕘 Timestamps:

🎬 In this video the following analysis is performed:

👋 Video introduction 0:00

📊 (i)How to estimate linear regression in Eviews 1:05

📊 (ii)How to interpret eviews regression output: 1:53

📊 (ii)Regression residuals: 11:30

---------------------------------------------------------------------------------------------------------

🎬 More EViews related videos:

---------------------------------------------------------------------------------------------------------

Doubts or comments? Please leave your comment and I will be pleased to provide you an answer.

👍 Like and subscribe for more videos!

🛎If you would like to contact me for research purposes, or work related issues, please feel to send me a message at:

---------------------------------------------------------------------------------------------------------

Thanks!

Hi everyone! This is a quick and simple Time Series: Linear Regression analysis - Output interpretation in Eviews. Learn how to estimate a simple linear regression and how to interpret the linear regression output results - how to estimate and interpret ols!

Summary of the video: Using real GDP data for Argentina and Brazil, I show you how to estimate a linear regression in eviews and how to interpret the regression estimation output. Estimate the linear regression yourself and obtain the linear regression results by downloading the data in the description. I hope you enjoy it!

📈 Download the dataset for free and replicate the content of the video:

✅ Visit my website to see all my FREE tutorials:

☕️ If you value my content and would like to show a recognition, you can make a donation:

---------------------------------------------------------------------------------------------------------

🕘 Timestamps:

🎬 In this video the following analysis is performed:

👋 Video introduction 0:00

📊 (i)How to estimate linear regression in Eviews 1:05

📊 (ii)How to interpret eviews regression output: 1:53

📊 (ii)Regression residuals: 11:30

---------------------------------------------------------------------------------------------------------

🎬 More EViews related videos:

---------------------------------------------------------------------------------------------------------

Doubts or comments? Please leave your comment and I will be pleased to provide you an answer.

👍 Like and subscribe for more videos!

🛎If you would like to contact me for research purposes, or work related issues, please feel to send me a message at:

---------------------------------------------------------------------------------------------------------

Thanks!

0:02:34

0:02:34

Linear Regression in 2 minutes

0:06:28

0:06:28

Linear Regression in Excel for Time Series Data

0:07:29

0:07:29

What is Time Series Analysis?

0:12:57

0:12:57

Linear Regression: Time Series Analysis

0:24:59

0:24:59

Time Series Forecasting with Regression Model

0:13:29

0:13:29

Video 1: Introduction to Simple Linear Regression

0:12:23

0:12:23

Using Linear Regression in Excel for Time Series Forecasting

0:03:00

0:03:00

Introducing Time Series Analysis and forecasting

0:26:41

0:26:41

REGRESSION MODELING || DATA ANALYTICS || LECTURE 01 BY DR. NEHA SINGH || AKGEC

0:42:47

0:42:47

Wooldridge Econometrics for Economics BSc students Ch. 10: Regression Analysis with Time Series Data

0:12:44

0:12:44

Forecasting in Excel using Linear Regression

0:04:48

0:04:48

Regression 1: Regression for forecasting

0:11:09

0:11:09

Time Series Vs Non Time Series Problems- Why Time Series Forecasting Is Difficult?

0:23:21

0:23:21

Lecture 10. Time series forecasting with Multiple Linear Regression

0:07:38

0:07:38

Vector Auto Regression : Time Series Talk

0:08:54

0:08:54

Time Series Talk : Autoregressive Model

0:15:05

0:15:05

Linear Regression Using Least Squares Method - Line of Best Fit Equation

1:16:19

1:16:19

8. Time Series Analysis I

0:09:38

0:09:38

Regression Analysis: An introduction to Linear and Logistic Regression

0:07:42

0:07:42

MLfT 1 : Wk 3.2.1 - ARIMA compared to linear regression

0:23:09

0:23:09

Time Series Forecasting with XGBoost - Use python and machine learning to predict energy consumption

1:22:13

1:22:13

6. Regression Analysis

0:06:22

0:06:22

5.1: Time series regression models introduction

0:05:18

0:05:18

An Introduction to Linear Regression Analysis

Комментарии