filmov

tv

PCA 6 - Relationship to SVD

Показать описание

Errata:

1:35 - Both the rows and columns of U are actually orthonormal.

0:09:14

0:09:14

PCA 6 - Relationship to SVD

0:10:34

0:10:34

6 - Correlation and PCA

0:02:39

0:02:39

PCA 6: Principal component analysis

0:20:09

0:20:09

Data Analysis 6: Principal Component Analysis (PCA) - Computerphile

0:06:28

0:06:28

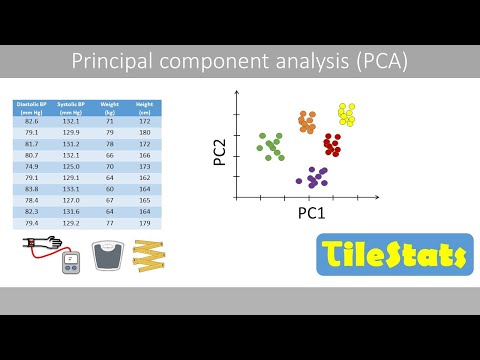

Principal Component Analysis (PCA)

0:02:28

0:02:28

Interpreting a PCA model

0:10:54

0:10:54

Principal Component Analysis (PCA) | Ordination Analysis | Multivariate Analysis | OriginPro 2022

0:21:58

0:21:58

StatQuest: Principal Component Analysis (PCA), Step-by-Step

0:00:47

0:00:47

PCA Peel play-by-play

0:04:08

0:04:08

PCA (video 6): Summary

0:03:55

0:03:55

How to create index using Principal component analysis (PCA) in Stata

0:10:56

0:10:56

Principal Component Analysis (PCA) - easy and practical explanation

0:09:36

0:09:36

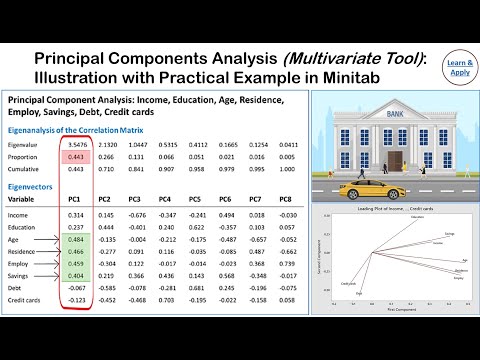

Principal Component Analysis (PCA): With Practical Example in Minitab

0:06:14

0:06:14

Creating Index of Multiple Variables using Principal Component Analysis (PCA) in 6 MINUTES

0:03:10

0:03:10

PCA 6: coordinates in low-dimensional space

0:02:36

0:02:36

CcpNmr AnalysisMetabolomics V3 - 6 Principal Component Analysis (PCA)

0:03:33

0:03:33

6 Visium data: PCA and clustering

0:20:22

0:20:22

PCA : the math - step-by-step with a simple example

0:22:11

0:22:11

PCA : the basics - explained super simple

0:09:06

0:09:06

6- 4 Activity PCA Example with the Iris data set

0:19:27

0:19:27

Principal Component Analysis (PCA) using Microsoft Excel video

0:23:19

0:23:19

#8 ( Principal Component Analysis ) || Section - 6 || PCA

0:06:07

0:06:07

PCA and SVD | Appearance Matching

0:25:49

0:25:49

Harvard AM205 video 2.13 - An example of PCA

Комментарии