filmov

tv

Accounting for Construction Contracts

Показать описание

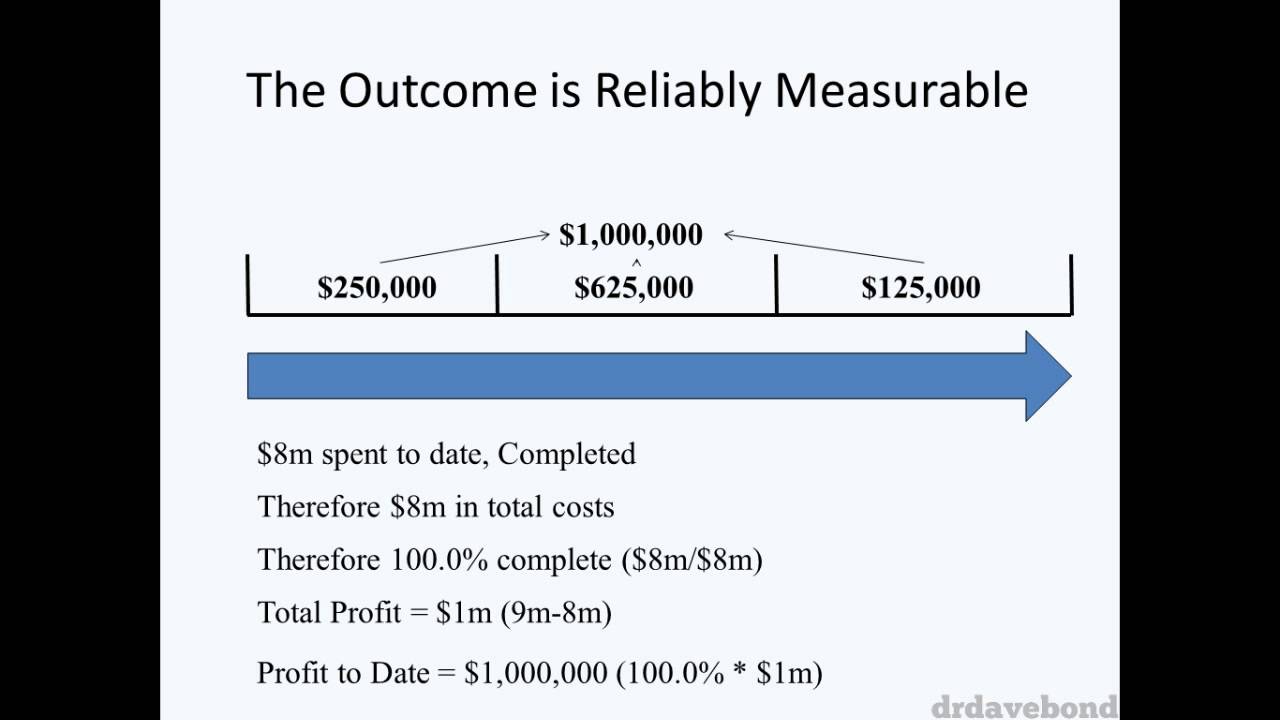

This video outlines how to account for fixed price construction contracts pursuant to AASB 111 Construction Contracts (please note that AASB 111 is equivalent to IAS 11 Construction Contracts).

Published 26/03/2014

Published 26/03/2014

0:05:24

0:05:24

Construction Accounting Vs Regular Accounting

0:08:39

0:08:39

Accounting for Construction Contracts

0:33:57

0:33:57

AFAR: LONG TERM CONSTRUCTION CONTRACTS (LTCC)

0:18:36

0:18:36

AS 7 in ENGLISH - Construction Contracts || CA Inter/IPCC || ADVANCE ACCOUNTS

1:31:50

1:31:50

AS 7 Construction Contracts Revision | With Questions | CA Inter | Advanced Accounts | Aakash Kandoi

0:08:11

0:08:11

IFRS 15 Construction Contracts Simple Explanation

0:10:08

0:10:08

10 important things to know about construction accounting

0:19:17

0:19:17

Accounting for Construction Contracts - IFRS 15

1:24:15

1:24:15

AS 1 | AS 2 | AS 4 | AS 5 | AS 12 | AS 17 | AS 18 | AS 24 | AS 25 | AS 29 | Adv. Accounting Revision

0:00:16

0:00:16

Accounting for construction contracts

0:01:31

0:01:31

What is accounting for construction contracts? | Bookkeeping for Contractors

0:20:28

0:20:28

Works Contract /construction Accounting Tally Prime class 8

0:20:30

0:20:30

long-term construction contract accounting

1:37:32

1:37:32

Ch 8 Unit 1 | AS 7 Construction Contracts | CA Inter Advanced Accounting by CA Parag Gupta

1:15:04

1:15:04

AS 7 Construction Contracts Full Revision + Questions | CA Inter Advanced Accounting

0:28:59

0:28:59

AS-7 | Construction Contracts Revision | Advanced Accounts | CA Inter |What is Construction Contract

0:12:39

0:12:39

#casalimarakkal AS 7 CONSTRUCTION CONTRACT ACCOUNTING in 12 minutes AS 7

0:04:21

0:04:21

Accounting Standard 7 | ACCOUNTING FOR CONSTRUCTION CONTRACTS | AS 7

0:14:04

0:14:04

Long-term construction contracts

0:05:31

0:05:31

Construction Contract | Accounting Standard

0:17:05

0:17:05

CIMA F2 Construction Contracts (IAS 11) - Profitable contracts

0:00:29

0:00:29

Fixed Priced OR Cost Plus Construction Contracts

0:34:15

0:34:15

#1 Contract Costing - Concept - B.COM / CMA / CA INTER - By Saheb Academy

0:09:37

0:09:37

Revenue Recognition For Long Term Contracts | Percentage Of Completion | Intermediate Accounting

Комментарии