filmov

tv

The Treynor-Black model - the balance between active and passive investment (Excel) (SUB)

Показать описание

Hello everyone!

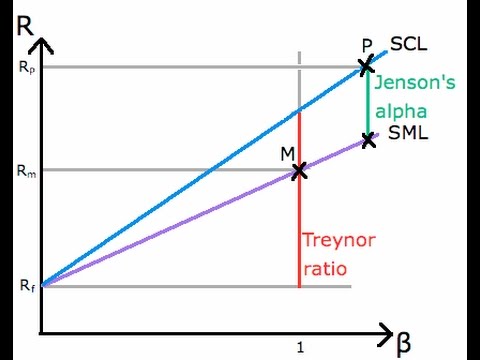

In today's video, I'm going to explain the Treynor-Black model, a portfolio-optimisation model that seeks to maximise a portfolio's Sharpe ratio. I will also demonstrate how to calculate it in Excel, using the data on Royal Dutch Shell and BP, the most famous UK energy companies.

Don't forget to subscribe to NEDL and give this video a thumbs up if you want more videos in Finance!

In today's video, I'm going to explain the Treynor-Black model, a portfolio-optimisation model that seeks to maximise a portfolio's Sharpe ratio. I will also demonstrate how to calculate it in Excel, using the data on Royal Dutch Shell and BP, the most famous UK energy companies.

Don't forget to subscribe to NEDL and give this video a thumbs up if you want more videos in Finance!

0:23:31

0:23:31

The Treynor-Black model - the balance between active and passive investment (Excel) (SUB)

0:04:00

0:04:00

Sharpe Ratio Vs Treynor Ratio Explained in 4 Minutes

0:04:58

0:04:58

Treynor ratio (for the @CFA Level 1 exam)

0:11:54

0:11:54

Applied Portfolio Construction (Treynor Black Model) Group 3

0:10:00

0:10:00

Treynor Black Model-07 by Amit Kumar Singh

0:30:42

0:30:42

Modelo Treynor Black

0:09:54

0:09:54

Treynor Black Model-06-Amit Kumar Singh

0:10:01

0:10:01

Treynor Black Model-03 by Amit Kumar Singh

0:10:00

0:10:00

Treynor Black Model-Session-02 by Amit Kumar Singh

0:10:00

0:10:00

Treynor Black Model Session-01-Amit Kumar Singh

0:10:00

0:10:00

Treynor Black Model-04 by Amit Kumar Singh

0:09:38

0:09:38

Treynor Black Model-05 by Amit Kumar Singh

0:01:14

0:01:14

What is The Treynor Ratio?

0:05:31

0:05:31

Treynor model : portfolio management

0:02:38

0:02:38

Treynor Ratio

0:04:47

0:04:47

Treynor ratio definition for investment modeling

0:01:34

0:01:34

Treynor Ratio with Excel

0:09:56

0:09:56

On models of active portfolio management

0:09:21

0:09:21

Excel Tutorial. Treynor Ratio Performance Metric

0:09:59

0:09:59

R Tutorial. Treynor Ratio Performance Metric

0:01:40

0:01:40

The optimal proportion to invest in the active portfolio is… (Google Sheets)

0:20:12

0:20:12

Portfolio Evaluation Sharpe & Treynor' Model 1

0:11:13

0:11:13

Portfolio Performance Evaluation Sharpe & Treynor Model 2

0:05:34

0:05:34

Calculating Treynor Index | Treynor Ratio

Комментарии