filmov

tv

Treynor Ratio

Показать описание

This video shows how to calculate the Treynor Ratio.

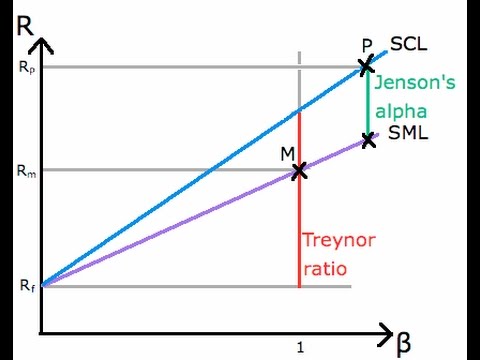

The Treynor Ratio is a percentage that measures the reward-to-risk ratio of a portfolio, where risk refers only to the systematic risk of the portfolio. The Treynor Ratio is calculated as follows:

Treynor Ratio = Excess Return of the Portfolio / Beta of the Portfolio

The excess return of the portfolio is the portfolio's expected return minus the risk-free rate.

The Treynor Ratio is similar to the Sharpe Ratio in that it can be used to rank portfolios based on their reward versus their risk. However, the Treynor Ratio uses systematic risk whereas the Sharpe Ratio uses volatility (total risk) to measure risk. Thus, the Treynor Ratio is best used with well-diversified portfolios (because in those portfolios nonsystematic risk has been diversified away).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

The Treynor Ratio is a percentage that measures the reward-to-risk ratio of a portfolio, where risk refers only to the systematic risk of the portfolio. The Treynor Ratio is calculated as follows:

Treynor Ratio = Excess Return of the Portfolio / Beta of the Portfolio

The excess return of the portfolio is the portfolio's expected return minus the risk-free rate.

The Treynor Ratio is similar to the Sharpe Ratio in that it can be used to rank portfolios based on their reward versus their risk. However, the Treynor Ratio uses systematic risk whereas the Sharpe Ratio uses volatility (total risk) to measure risk. Thus, the Treynor Ratio is best used with well-diversified portfolios (because in those portfolios nonsystematic risk has been diversified away).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

0:04:58

0:04:58

Treynor ratio (for the @CFA Level 1 exam)

0:04:00

0:04:00

Sharpe Ratio Vs Treynor Ratio Explained in 4 Minutes

0:02:38

0:02:38

Treynor Ratio

0:01:14

0:01:14

What is The Treynor Ratio?

0:08:52

0:08:52

Investment Performance Evaluation in Excel: Sharpe Ratio, Treynor Ratio & Jensen's Alpha

0:05:10

0:05:10

CFA® Level I Portfolio Management - Sharpe ratio, Treynor ratio, M2 , and Jensen’s alpha

0:07:43

0:07:43

How to ANALYSE Hedge Funds' Performance | Sharpe, Sortino, Treynor Ratios Explained

0:17:42

0:17:42

Sharpe ratio, Treynor Ratio, M Squared and Jensens Alpha - Portfolio Risk and Return : Part Two

0:19:48

0:19:48

Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams)

0:03:41

0:03:41

Treynor Ratio

0:01:34

0:01:34

Treynor Ratio with Excel

0:11:26

0:11:26

How to calculate Treynor ratio in Excel / Analyzing stock returns / Episode 11

0:04:10

0:04:10

Treynor Ratio

0:02:29

0:02:29

Treynor Ratio Explained in 3 minutes

0:05:10

0:05:10

Treynor Ratio & Alpha | Risk Adjusted Return | Mutual funds

0:22:51

0:22:51

Calculate performance ratios in Excel! Sharpe, Sortino, Treynor, and Information Ratio!

0:02:24

0:02:24

Treynor ratio • Investing concepts explained in 2 minutes • #financialeducation

0:09:21

0:09:21

Excel Tutorial. Treynor Ratio Performance Metric

0:02:45

0:02:45

Understanding Treynor Ratio

0:01:37

0:01:37

Video Blog 19: Technical Analysis - Treynor Ratio - Market Risk & Volatility

0:07:44

0:07:44

Sharpe Ratio, Treynor Ratio and Jenson's Alpha - Mutual Fund and Portfolio Management

0:04:47

0:04:47

Treynor ratio definition for investment modeling

0:05:55

0:05:55

Treynor Ratio kya hota hai ? | What is Treynor Ratio | @pradeepSchokhani

0:20:58

0:20:58

Treynor measure, treynor ratio, Performance Evaluation of existing portfolio, investment analysis

Комментарии