filmov

tv

AR Model Code Example : Time Series Talk

Показать описание

How do we fit an AR model to real data?

0:10:08

0:10:08

AR Model Code Example : Time Series Talk

0:05:01

0:05:01

What are Autoregressive (AR) Models

0:13:07

0:13:07

Auto Regression(AR) Model in Python| Time Series Forecasting #5|

0:00:09

0:00:09

Stories AR - Augmented Reality platform | Example of AR-photo - animated business card

0:21:49

0:21:49

Autoregressive (AR) model: estimation and stability tests (Excel)

0:00:18

0:00:18

AR Business Card Concept made with ARKit

0:08:31

0:08:31

CFA® Level II Quant - Autoregressive (AR) Models: Mean reversion, Covariance Stationarity

0:13:43

0:13:43

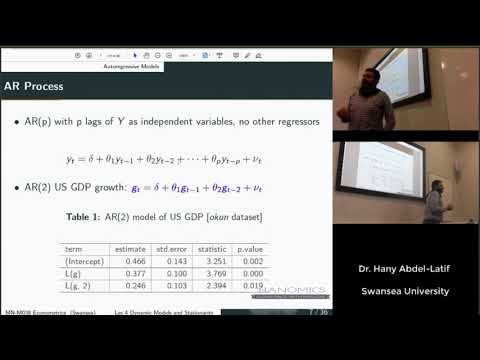

Econometrics - Autoregressive (AR) Models

0:32:48

0:32:48

All Forecasting Models in ONE Video | AR | MA | ARMA | ARIMA | SARIMA | VAR | VMA | VARIMA | Part 9

0:09:28

0:09:28

Example: AR(2) Model

0:04:10

0:04:10

Python Tutorial: Intro to AR, MA and ARMA models

0:00:06

0:00:06

IELTS Speaking recent questions | IELTS Exam preparation #shorts

0:00:27

0:00:27

How to Answer Any Question on a Test

0:00:33

0:00:33

Math Olympiad Question | You should know this trick!!

0:00:15

0:00:15

Me failing in my exam .....#bts @Purple_Population_7

0:00:25

0:00:25

PREGNANCY TEST LIVE! PREGNANCY TEST KIT RESULTS! Pregnancy negative vs positive #shorts

0:00:28

0:00:28

Chain stitch practice using aari iron needle #aarineedle #aaritutorial #aariembroidery

0:00:17

0:00:17

magnetic fields lines of solenoid #shorts #class10science #scienceexperiment

0:00:31

0:00:31

How to Answer Any Question on a Test

0:00:19

0:00:19

Snap Lens Studio AR Experience Anchored with an AR QR Code | ar-code.com

0:00:23

0:00:23

How to Draw in 3D 🤯

0:00:13

0:00:13

𝐓𝐨𝐦𝐦𝐲 𝐇𝐢𝐥𝐟𝐢𝐠𝐞𝐫 𝐋𝐚𝐮𝐧𝐜𝐡𝐞𝐬 𝐀𝐑 𝐓𝐫𝐲-𝐎𝐧 𝐌𝐢𝐫𝐫𝐨𝐫𝐬 𝐢𝐧 𝐒𝐭𝐨𝐫𝐞𝐬 𝐰𝐢𝐭𝐡 𝐙𝐄𝐑𝐎𝟏𝟎'𝐬 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐲 🚀🚀...

0:00:10

0:00:10

What is your UPSC Roll number 😱|UPSC Interview..#shorts

0:00:07

0:00:07

Gender of nouns in English grammar @Studyexperts5643

Комментарии