filmov

tv

What is an insurance deductible

Показать описание

Deductible defined

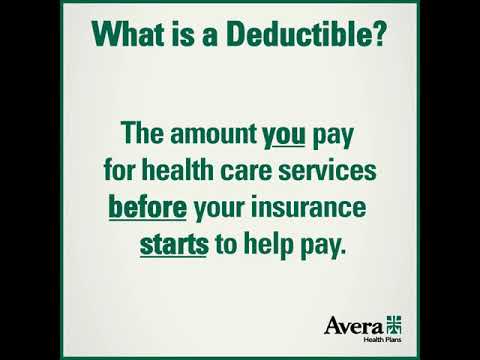

A deductible is an amount of money that you yourself are responsible for paying toward an insured loss. When a disaster strikes your home, or you have a car accident, the deductible amount is subtracted or “deducted” from your claim payment.

Deductibles are how risk is shared between you, the policyholder, and your insurer.

A deductible can be either a specific dollar amount or a percentage of the total amount of insurance on a policy. The amount is established by the terms of your coverage and can be found on the declarations (or front) page of standard homeowners and auto insurance policies.

How deductibles work

For dollar amount deductibles, a specific amount would come off the top of your claim payment.

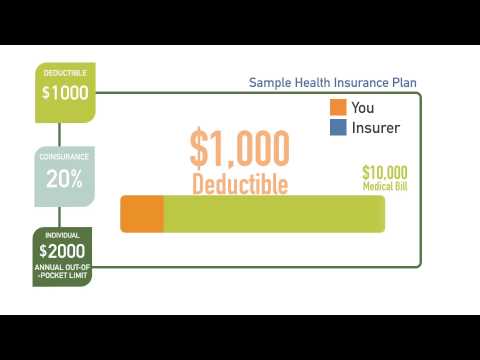

For example, if your policy states a $500 deductible, and your insurer has determined that you have an insured loss worth $10,000, you would receive a claims check for $9,500.

Percentage deductibles generally only apply to homeowner's policies and are calculated based on a percentage of the home’s insured value. So if your house is insured for $100,000 and your insurance policy has a 2 percent deductible, $2,000 would be deducted from any claim payment. In the event of the $10,000 insurance loss, you would be paid $8,000. In the event of a $25,000 loss, your claim check would be $23,000.

Note that the deductible applies with auto insurance or a homeowners policy each time you file a claim. The one major exception to this is Florida, where hurricane deductibles are specifically applied per season rather than for each storm.

Deductibles generally apply to property damage, not to the liability portion of homeowners or auto insurance policies. A deductible would apply to property damaged in a rogue outdoor grill fire to use a homeowners policy example. Still, there would be no deductible against the policy's liability portion if a burned guest made a medical claim or sued.

Raising your deductible can save money.

One way to save money on a homeowners or auto insurance policy is to raise the deductible so, if you're shopping for insurance, ask about the options for deductibles when comparing policies.

Increasing your auto insurance's dollar deductible from $200 to $500 can reduce collision and comprehensive coverage premium costs. Going to a $1,000 deductible may save you even more.

Most homeowners and renters insurers offer a minimum $500 or $1,000 deductible. Raising the deductible to more than $1,000 can save on the cost of the policy.

Of course, remember that you'll be responsible for the deductible in the event of loss, so make sure that you're comfortable with the amount.

Homeowners disaster deductibles

Wind/hail and hurricanes are covered by standard homeowners insurance; flood and earthquake policies are purchased separately by homeowners. But each of these disasters has its own deductible rules. If you're in an area that's high risk for one of these natural disasters, understand how much of a deductible you'll need to pay if a catastrophe strikes. Start here, check your policies and speak to your insurance professional to learn exactly how your particular deductibles work.

Wind/hail deductibles work similarly to hurricane deductibles and are most common in places that typically experience severe windstorms and hail. These include Midwestern states (like Ohio) and around Tornado Alley (Texas, Oklahoma, Kansas, and Nebraska). Wind/hail deductibles are most commonly paid in percentages, typically from one to 5 percent.

Flood insurance offers a range of deductibles. If you have—or are considering buying—flood insurance, make sure you understand your deductible. Flood insurance deductibles vary by state and insurance company and are available in dollar amounts or percentages. Furthermore, you can choose one deductible for your home's structure and another for its contents (note that your mortgage company may require that your flood insurance deductible is under a certain amount to help ensure you'll be able to pay it).

Earthquake insurance has percentage deductibles that are anywhere from 2 percent to 20 percent of the replacement value of your home, depending on location. Insurers in states with a higher than average risk of earthquakes (for example, Washington, Nevada, and Utah) often set minimum deductibles at around 10 percent. In California, the basic California Earthquake Authority (CEA) policy includes a deductible that is 15 percent of the replacement cost of the main home structure and starting at 10 percent for additional coverages (such as on a garage or other outbuildings).

A deductible is an amount of money that you yourself are responsible for paying toward an insured loss. When a disaster strikes your home, or you have a car accident, the deductible amount is subtracted or “deducted” from your claim payment.

Deductibles are how risk is shared between you, the policyholder, and your insurer.

A deductible can be either a specific dollar amount or a percentage of the total amount of insurance on a policy. The amount is established by the terms of your coverage and can be found on the declarations (or front) page of standard homeowners and auto insurance policies.

How deductibles work

For dollar amount deductibles, a specific amount would come off the top of your claim payment.

For example, if your policy states a $500 deductible, and your insurer has determined that you have an insured loss worth $10,000, you would receive a claims check for $9,500.

Percentage deductibles generally only apply to homeowner's policies and are calculated based on a percentage of the home’s insured value. So if your house is insured for $100,000 and your insurance policy has a 2 percent deductible, $2,000 would be deducted from any claim payment. In the event of the $10,000 insurance loss, you would be paid $8,000. In the event of a $25,000 loss, your claim check would be $23,000.

Note that the deductible applies with auto insurance or a homeowners policy each time you file a claim. The one major exception to this is Florida, where hurricane deductibles are specifically applied per season rather than for each storm.

Deductibles generally apply to property damage, not to the liability portion of homeowners or auto insurance policies. A deductible would apply to property damaged in a rogue outdoor grill fire to use a homeowners policy example. Still, there would be no deductible against the policy's liability portion if a burned guest made a medical claim or sued.

Raising your deductible can save money.

One way to save money on a homeowners or auto insurance policy is to raise the deductible so, if you're shopping for insurance, ask about the options for deductibles when comparing policies.

Increasing your auto insurance's dollar deductible from $200 to $500 can reduce collision and comprehensive coverage premium costs. Going to a $1,000 deductible may save you even more.

Most homeowners and renters insurers offer a minimum $500 or $1,000 deductible. Raising the deductible to more than $1,000 can save on the cost of the policy.

Of course, remember that you'll be responsible for the deductible in the event of loss, so make sure that you're comfortable with the amount.

Homeowners disaster deductibles

Wind/hail and hurricanes are covered by standard homeowners insurance; flood and earthquake policies are purchased separately by homeowners. But each of these disasters has its own deductible rules. If you're in an area that's high risk for one of these natural disasters, understand how much of a deductible you'll need to pay if a catastrophe strikes. Start here, check your policies and speak to your insurance professional to learn exactly how your particular deductibles work.

Wind/hail deductibles work similarly to hurricane deductibles and are most common in places that typically experience severe windstorms and hail. These include Midwestern states (like Ohio) and around Tornado Alley (Texas, Oklahoma, Kansas, and Nebraska). Wind/hail deductibles are most commonly paid in percentages, typically from one to 5 percent.

Flood insurance offers a range of deductibles. If you have—or are considering buying—flood insurance, make sure you understand your deductible. Flood insurance deductibles vary by state and insurance company and are available in dollar amounts or percentages. Furthermore, you can choose one deductible for your home's structure and another for its contents (note that your mortgage company may require that your flood insurance deductible is under a certain amount to help ensure you'll be able to pay it).

Earthquake insurance has percentage deductibles that are anywhere from 2 percent to 20 percent of the replacement value of your home, depending on location. Insurers in states with a higher than average risk of earthquakes (for example, Washington, Nevada, and Utah) often set minimum deductibles at around 10 percent. In California, the basic California Earthquake Authority (CEA) policy includes a deductible that is 15 percent of the replacement cost of the main home structure and starting at 10 percent for additional coverages (such as on a garage or other outbuildings).

0:00:57

0:00:57

0:02:33

0:02:33

0:06:07

0:06:07

0:03:01

0:03:01

0:01:01

0:01:01

0:02:34

0:02:34

0:02:32

0:02:32

0:01:49

0:01:49

0:02:26

0:02:26

0:00:26

0:00:26

0:00:53

0:00:53

0:01:14

0:01:14

0:01:18

0:01:18

0:00:31

0:00:31

0:00:28

0:00:28

0:04:08

0:04:08

0:02:14

0:02:14

0:02:51

0:02:51

0:03:58

0:03:58

0:00:21

0:00:21

0:04:55

0:04:55

0:03:47

0:03:47

0:00:48

0:00:48

0:03:01

0:03:01