filmov

tv

IFRS (4): Accruals, Provisions, and Contingent Liabilities | IAS 37 Explained | KRESS COOPER

Показать описание

Master the concepts of Accruals, Provisions, and Contingent Liabilities with this comprehensive guide to IAS 37 under IFRS standards. This video explains the definitions, recognition criteria, and practical applications of provisions and contingent liabilities, along with real-world examples to help you understand financial reporting requirements. Perfect for accountants, students, and professionals looking to enhance their knowledge of IFRS compliance. Stay informed with this in-depth tutorial on IAS 37 Explained by KRESS COOPER.

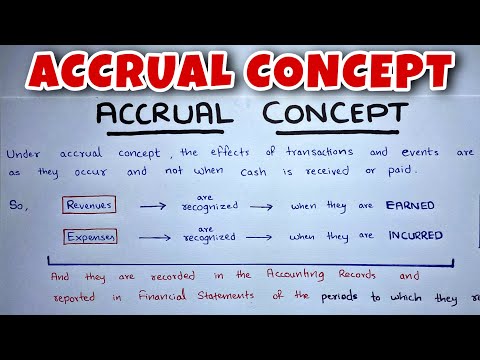

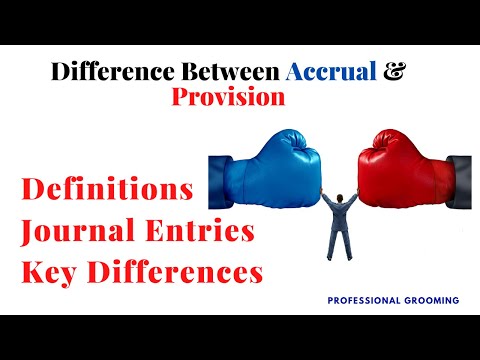

Accruals, provisions, and contingent liabilities are critical concepts in accounting that help accurately reflect a company's financial position. Accruals recognize revenues and expenses when they occur, regardless of cash flow, ensuring a proper match between income and expenses. Provisions are liabilities of uncertain timing or amount, created for anticipated future obligations, such as warranty claims or restructuring costs. In contrast, contingent liabilities are potential obligations contingent on future events, disclosed in financial statements if the likelihood of occurrence is more than remote. Together, these elements enhance transparency and provide stakeholders with a clear understanding of a company's financial health.

🟨 Connect with Me 🟨

#IFRS #IAS37 #AccrualsAndProvisions #ContingentLiabilities #AccountingStandards #FinancialReporting #KressCooper #IFRS #IAS37 #Accruals #Provisions #ContingentLiabilities #FinancialReporting #AccountingStandards

Accruals, provisions, and contingent liabilities are critical concepts in accounting that help accurately reflect a company's financial position. Accruals recognize revenues and expenses when they occur, regardless of cash flow, ensuring a proper match between income and expenses. Provisions are liabilities of uncertain timing or amount, created for anticipated future obligations, such as warranty claims or restructuring costs. In contrast, contingent liabilities are potential obligations contingent on future events, disclosed in financial statements if the likelihood of occurrence is more than remote. Together, these elements enhance transparency and provide stakeholders with a clear understanding of a company's financial health.

🟨 Connect with Me 🟨

#IFRS #IAS37 #AccrualsAndProvisions #ContingentLiabilities #AccountingStandards #FinancialReporting #KressCooper #IFRS #IAS37 #Accruals #Provisions #ContingentLiabilities #FinancialReporting #AccountingStandards

0:58:55

0:58:55

0:09:00

0:09:00

0:06:26

0:06:26

0:03:26

0:03:26

0:09:57

0:09:57

0:15:08

0:15:08

0:03:52

0:03:52

0:09:18

0:09:18

0:11:00

0:11:00

0:06:26

0:06:26

0:35:11

0:35:11

0:07:52

0:07:52

0:02:48

0:02:48

0:07:21

0:07:21

0:04:34

0:04:34

0:15:13

0:15:13

0:31:46

0:31:46

0:03:13

0:03:13

0:03:57

0:03:57

3:14:45

3:14:45

0:28:35

0:28:35

0:11:50

0:11:50

![[Financial Accounting]: Chapter](https://i.ytimg.com/vi/gr-7eRjZolo/hqdefault.jpg) 0:22:36

0:22:36

0:20:03

0:20:03