filmov

tv

Perpetuity Lesson/Tutorial: Definition, Present Value of a Perpetuity Formula & Examples

Показать описание

In this Perpetuity Lesson I define what a perpetuity is, how to calculate the present value of a perpetuity, and also provide you with some examples of solving the present value of a perpetuity.

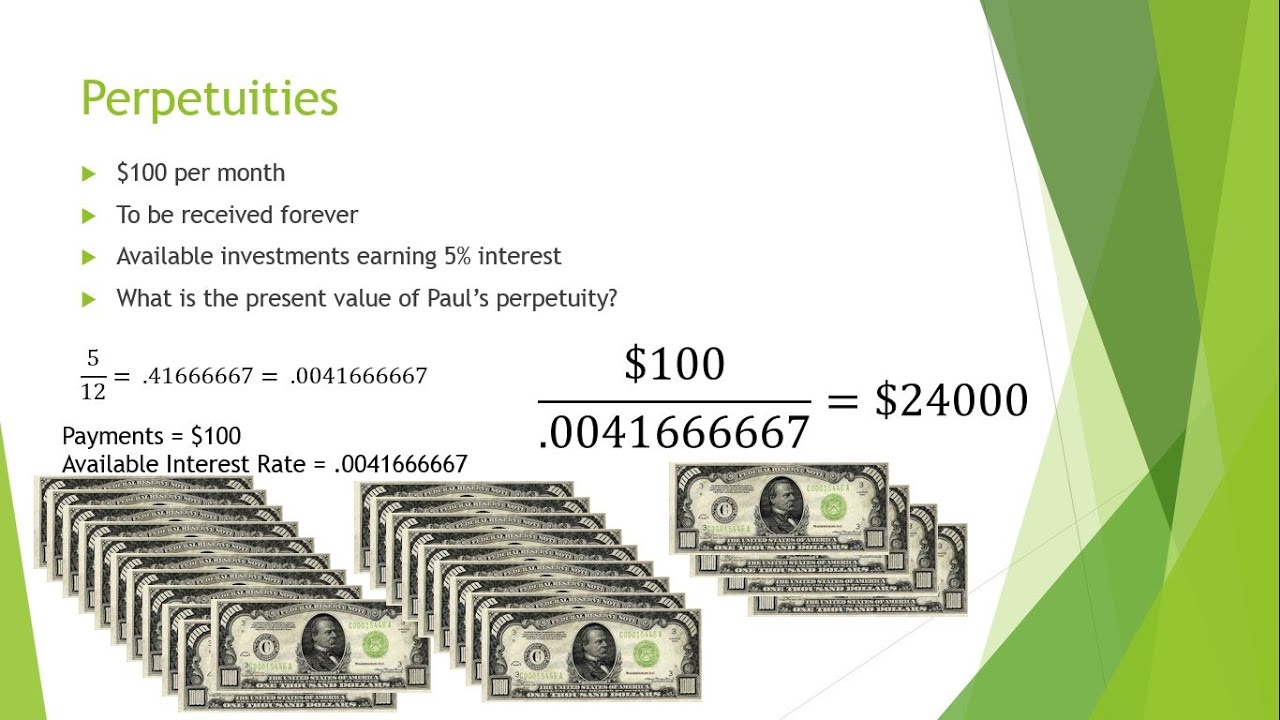

A perpetuity is a steady stream of Cash Flow s of equal amounts that are to be received or paid indefinitely. A perpetuity is a form of an ordinary annuity and is sometimes called a perpetuity annuity. A true perpetuity is rare but they are not non-existent. Around 1871 the British government issued a Bond that was a true perpetuity known as a Consol. The purchaser of a Consol was entitled to receive an annual coupon payment at a fixed rate forever. You may wonder why or how a government or any entity would want to agree to such a long-term commitment of payments. They do this because they can guarantee payment by reinvesting the money from the purchaser into Investment s that earn a higher return.

A perpetuity is a steady stream of Cash Flow s of equal amounts that are to be received or paid indefinitely. A perpetuity is a form of an ordinary annuity and is sometimes called a perpetuity annuity. A true perpetuity is rare but they are not non-existent. Around 1871 the British government issued a Bond that was a true perpetuity known as a Consol. The purchaser of a Consol was entitled to receive an annual coupon payment at a fixed rate forever. You may wonder why or how a government or any entity would want to agree to such a long-term commitment of payments. They do this because they can guarantee payment by reinvesting the money from the purchaser into Investment s that earn a higher return.

0:05:16

0:05:16

Perpetuity Lesson/Tutorial: Definition, Present Value of a Perpetuity Formula & Examples

0:09:59

0:09:59

Present Value of a Perpetuity (aka Ordinary Perpetuity)

0:03:23

0:03:23

Perpetuity: What is Perpetuity

0:06:00

0:06:00

Perpetuity and Its Present Value

0:03:47

0:03:47

Present Value of Perpetuity Formula

0:05:14

0:05:14

Time Value of Money - Present Value vs Future Value

0:02:28

0:02:28

Present value of a perpetuity - Example 1

0:02:49

0:02:49

What is Perpetuity? - Financial Definition, Formula and Examples.

0:05:30

0:05:30

Present value of a perpetuity

0:06:16

0:06:16

Present Value and Perpetuity Formulas

0:05:53

0:05:53

TVM 14: Perpetuity

0:04:17

0:04:17

Present value of Perpetual cash flow

0:02:20

0:02:20

Perpetuities

0:03:03

0:03:03

How to derive the present value formula for annuity and perpetuity

0:07:17

0:07:17

Present value of an annuity

0:03:02

0:03:02

Present value of perpetuity

0:03:41

0:03:41

PERPETUITIES

0:05:26

0:05:26

Net Present Value (NPV) explained

0:04:32

0:04:32

Present Value of a Perpetuity

0:04:36

0:04:36

Perpetuity: Concept and Calculation

0:16:15

0:16:15

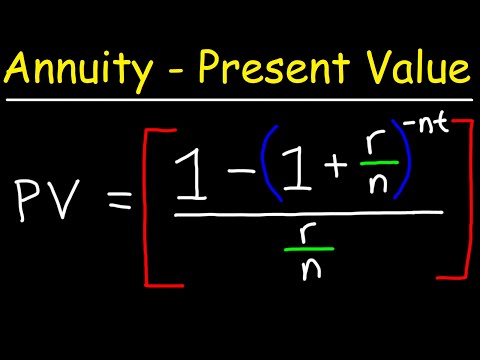

How To Calculate The Present Value of an Annuity

0:10:53

0:10:53

Module 3 Annuities and Perpetuities

0:21:53

0:21:53

Time Value of Money Finance - TVM Formulas & Calculations - Annuities, Present Value, Future Val...

0:02:34

0:02:34

Present Value of Ordinary Perpetuity and Perpetuity-due

Комментарии