filmov

tv

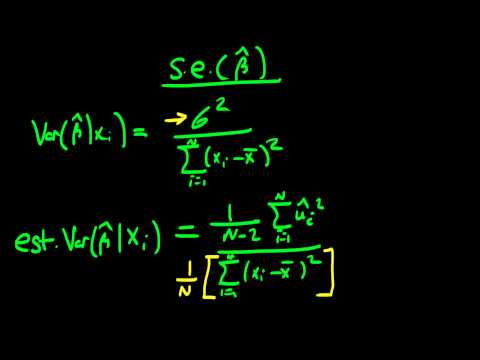

Least Square Estimators - Variance of Estimators, b0 and b1, Proof

Показать описание

** NOTE: At minute 11:48, I forgot to write the "squared" above X-bar. Later, at minute 28:26, when I summarize everything I found and solve for Var(b0), I do have X-bar squared. This was a mistake at minute 11:48, though it was not a mistake that I carried to my solution (the solution at the end of the video is correct).

0:30:11

0:30:11

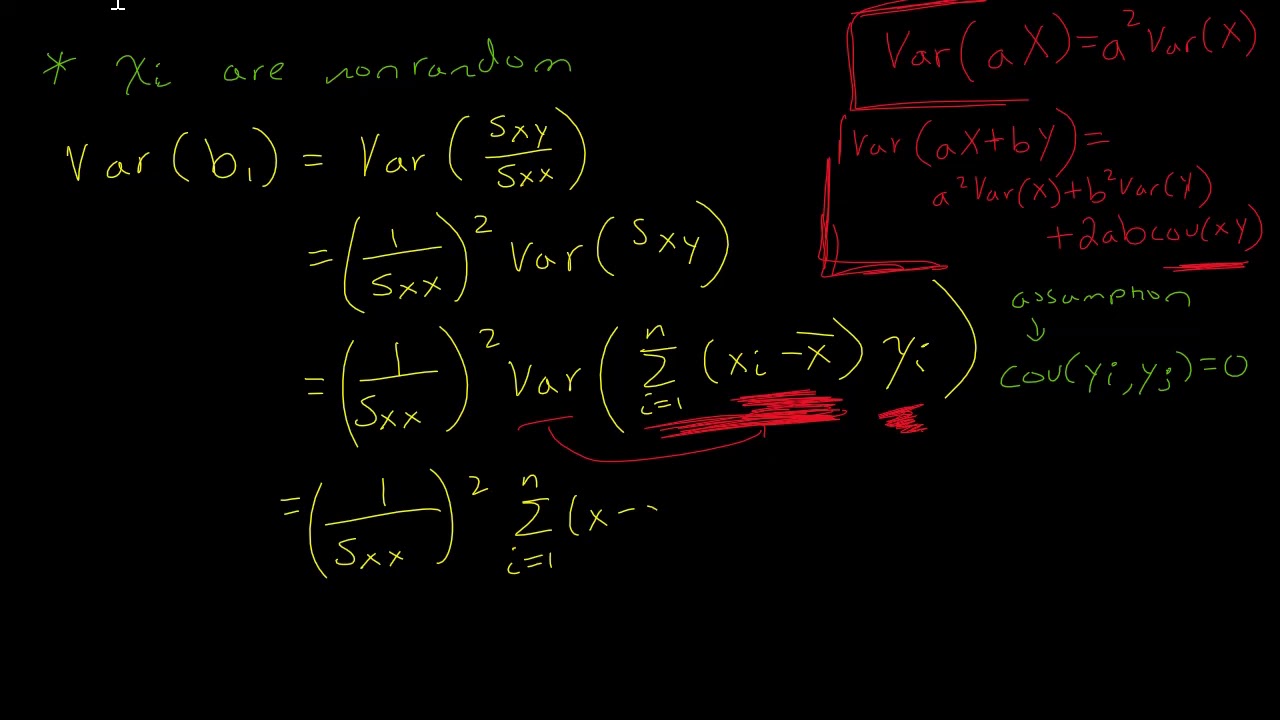

Least Square Estimators - Variance of Estimators, b0 and b1, Proof

0:09:04

0:09:04

Least Square Estimators - Estimator of Variance, sigma^2

0:10:54

0:10:54

Deriving the mean and variance of the least squares slope estimator in simple linear regression

0:05:32

0:05:32

Variance of Least Squares Estimators - Matrix Form

0:07:52

0:07:52

Least Square Estimators - Variance of Estimators Using Matrices

0:06:23

0:06:23

The variance of the least squares estimator

0:10:07

0:10:07

Variance of Least Squares Estimators (Part 2) | Simple Linear Regression

0:04:39

0:04:39

Variance of Least Squares Estimators (Part 1) | Simple Linear Regression

8:17:43

8:17:43

Linear regression full course tutorials part 14

0:08:49

0:08:49

Multiple Linear Regression Variance of Least Squares Estimator, b

0:12:13

0:12:13

Deriving the least squares estimators of the slope and intercept (simple linear regression)

0:07:19

0:07:19

Least Squares Estimators as BLUE

0:07:10

0:07:10

Variance of OLS estimators - part one

0:15:05

0:15:05

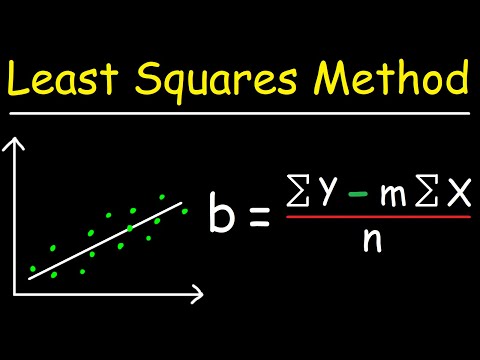

Linear Regression Using Least Squares Method - Line of Best Fit Equation

0:06:22

0:06:22

Estimating the Variance of the Error Term in a Least Squares Regression Line, problem 3

0:03:35

0:03:35

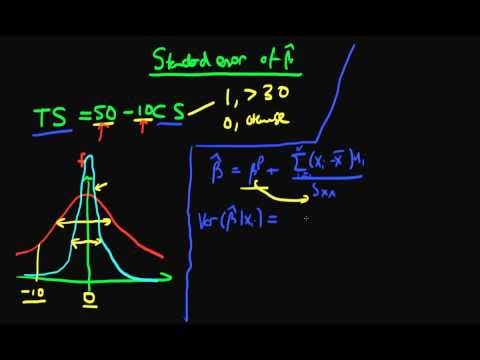

3.17 - The Variance of OLS Estimators

0:25:37

0:25:37

Least Squares Estimator - Unbiased Estimator and Variance

0:05:32

0:05:32

14 - Variance of Least Squares Estimators - Matrix Form

0:13:48

0:13:48

MLE vs OLS | Maximum likelihood vs least squares in linear regression

0:08:06

0:08:06

Lecture 9: Statistical Properties of Least Square Estimators

0:03:52

0:03:52

Estimated variance of OLS estimators - intuition behind maths

0:12:00

0:12:00

Least Square Estimators - Unbiased Proof

0:05:34

0:05:34

Lecture 11: Estimation of Sigma Square

0:02:16

0:02:16

Variance of the OLS estimator (Part 1)

Комментарии