filmov

tv

How To Manage Your Money Like The Top 1% (The 60/30/10 Rule)

Показать описание

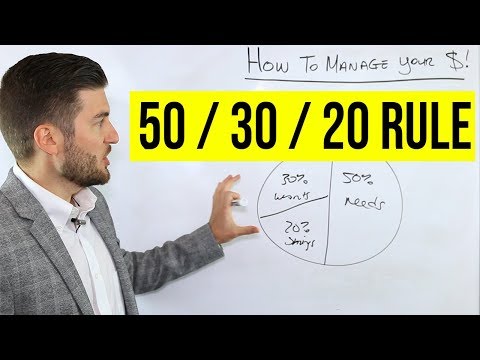

In this video, we talk about one of the personal finance rules of money management that even the wealthy will use. This is called the 60/30/10 rule and it's an updated version of the 50/30/20 because personally, I think the 50/30/20 rule is dead with most Americans dealing with higher costs of living. However, even though the rule has changed a little bit, I show you with math that we can still get to financial independence, and ultimately try to earn our way into the top 1%

FREE STOCKS:

RESOURCES:

MY SOCIALS:

WHO AM I?

Hello 👋 I’m Humphrey, I used to be a financial advisor, worked in gaming/tech, and started my own eCommerce business. I make practical, rational content on investing, personal finance, the news, and much more with a data-backed approach. My goal is to help you with financial literacy and creating wealth.

PS: I am no longer a current Financial Advisor, any investment commentary are my opinions only. Some of the links in this description are affiliate links that I do receive a commission for & they help support the channel!

⏱️ Timestamps:

0:00 - Start Here

0:33 - The 50/30/20 Rule Is Outdated

2:51 - Introducing the 60/30/10 & Needs

5:35 - Wants

7:00 - Why 10% Is Still Sufficient

10:13 - Habits of the Wealthy

FREE STOCKS:

RESOURCES:

MY SOCIALS:

WHO AM I?

Hello 👋 I’m Humphrey, I used to be a financial advisor, worked in gaming/tech, and started my own eCommerce business. I make practical, rational content on investing, personal finance, the news, and much more with a data-backed approach. My goal is to help you with financial literacy and creating wealth.

PS: I am no longer a current Financial Advisor, any investment commentary are my opinions only. Some of the links in this description are affiliate links that I do receive a commission for & they help support the channel!

⏱️ Timestamps:

0:00 - Start Here

0:33 - The 50/30/20 Rule Is Outdated

2:51 - Introducing the 60/30/10 & Needs

5:35 - Wants

7:00 - Why 10% Is Still Sufficient

10:13 - Habits of the Wealthy

0:12:58

0:12:58

How to Manage Your Money So You Never Go Broke

0:07:08

0:07:08

How To Manage Your Money (50/30/20 Rule)

0:12:45

0:12:45

How To Manage Your Money Like The 1%

0:13:59

0:13:59

How To Manage Your Money Like The 1%

0:12:03

0:12:03

4 KEYS TO MANAGE YOUR MONEY by Sam Adeyemi

0:11:54

0:11:54

10 Ways To MANAGE Your MONEY Better

0:11:23

0:11:23

ACCOUNTANT EXPLAINS: How I manage my money on payday: Income, Expenses & Savings

0:14:46

0:14:46

How To Manage Your Money Like The Top 1% (The 60/30/10 Rule)

0:32:53

0:32:53

How To Manage Your Finances

0:05:17

0:05:17

Managing Your Money Using The 50-30-20 Rule

0:14:05

0:14:05

Do This EVERY Time You Get Paid (Paycheck Routine)

0:04:44

0:04:44

How To Start Getting Your Finances In Order

0:08:56

0:08:56

These Are The Steps To Manage Your Money | Personal Finance Basics

0:08:06

0:08:06

ACCOUNTANT EXPLAINS: Money Habits Keeping You Poor

0:41:10

0:41:10

How to Take Control of Your Money! | Ep. 1 | The Best of The Ramsey Show

0:15:38

0:15:38

How I Manage My Money on a Low Income (Budgeting + Saving)

0:32:16

0:32:16

How to Take Hold of Your Money | Dave Ramsey

0:11:36

0:11:36

10 Money Rules for Financial Success

0:09:53

0:09:53

5 Rules To Manage Your Money Like The Rich — Dave Ramsey

0:21:14

0:21:14

the student guide to personal finance 💸 adulting 101

0:10:57

0:10:57

The Chinese Secret to Saving Money Revealed

0:15:58

0:15:58

Managing Our Money (God's Way) | Debt, Budgeting, Savings, more | Melody Alisa

1:30:37

1:30:37

MASTERCLASS: How To ACTUALLY Manage Your Money Like The 1%

0:10:38

0:10:38

How I manage my personal finances as a minimalist.

Комментарии