filmov

tv

5 Things Your Homeowner's Insurance May NOT Pay

Показать описание

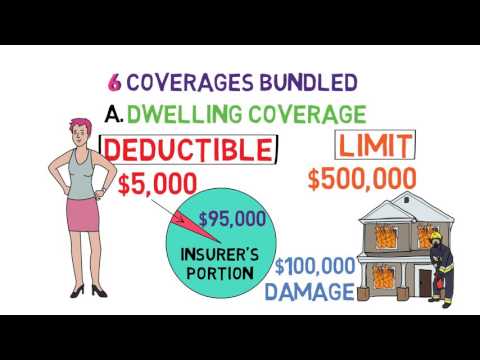

There are a few things that Homeowner's insurance might not pay for. These include flooding, insect damage, earthquakes, sewer backups, and other natural disasters. Homeowners insurance also might not mold, unless it came from a defect from your house, like your hot water heater flooding. If the nearby river overflows and your house gets mold, most homeowner's policies don't cover that.

00:00 Homeowner's Insurance Coverage

00:25 Are Floods covered by Insurance?

01:40 Earthquake insurance

02:21 Mold covered by homeowner insurance

03:30 Wear and tear covered by insurance

03:40 what does a home warranty cover

05:20 roof leaks and pool equipment

06:50 hot water heater home warranty

Companies that give homeowners insurance are companies like Lemonade, USAA, Erie Insurance, State Farm, Amica, American Family, Nationwide, and Farmers Insurance

00:00 Homeowner's Insurance Coverage

00:25 Are Floods covered by Insurance?

01:40 Earthquake insurance

02:21 Mold covered by homeowner insurance

03:30 Wear and tear covered by insurance

03:40 what does a home warranty cover

05:20 roof leaks and pool equipment

06:50 hot water heater home warranty

Companies that give homeowners insurance are companies like Lemonade, USAA, Erie Insurance, State Farm, Amica, American Family, Nationwide, and Farmers Insurance

0:25:48

0:25:48

Insurance 101 - Homeowners Insurance Coverage | The Ultimate Guide to Home Insurance

0:08:14

0:08:14

5 Things Your Homeowner's Insurance May NOT Pay

0:08:50

0:08:50

The 5 Things You Need to Know About Homeowners Insurance

0:15:23

0:15:23

5 Things You Should Know About Your Homeowners Insurance

0:06:48

0:06:48

5 Things To Consider When Looking For The Best Homeowners Insurance

0:00:50

0:00:50

5 Things Your Homeowners Insurance Won't Cover | Home Insurance Uxbridge

0:10:34

0:10:34

5 items for your homeowners insurance policy to consider

0:02:57

0:02:57

Homeowners Insurance 101 (Home Shopping 4/6)

0:01:22

0:01:22

5 Quick Financial Tips to Supercharge Your Finances

0:05:11

0:05:11

Should I Keep Paying My Homeowners Insurance?

0:00:27

0:00:27

5 Things that Impact Homeowners Insurance

0:00:09

0:00:09

Top 4 things to look at on your homeowners insurance policy

0:04:51

0:04:51

5 Tips for Maximizing your Homeowners Insurance Coverage

0:06:08

0:06:08

Top 5 Homeowners Insurance Claims

0:01:09

0:01:09

Surprising Things Covered by Homeowners Insurance

0:00:54

0:00:54

6 Odd Things Your Homeowners Insurance Covers

0:01:32

0:01:32

5 Important Things About Homeowners Insurance | Move Faster

0:02:22

0:02:22

5 Things to Know About Your Homeowners Policy - HFC Insurance | Insurance Agency in Lancaster SC

0:05:56

0:05:56

Tips on protecting your home, best-rated homeowners insurance

0:02:20

0:02:20

5 Main Components of Homeowners Insurance Policy | Insurance Tips by Jason Newell

0:01:00

0:01:00

5 Tips to Help you Save Money on your Homeowners Insurance #shortsyoutube

0:00:20

0:00:20

10 things to know about homeowners insurance

0:00:58

0:00:58

5 Common Things Covered by Homeowners Insurance Policy

0:00:41

0:00:41

Homeowners Insurance Hacks: 5 Ways To Save Big!

Комментарии