filmov

tv

The Money Multiplier Method | Brent Kesler

Показать описание

Brent Kessler was $984,711 in third party debt. Hearing this 200-year-old concept, he was able to pay all of it off in 39 months. Mr. Kesler will be going in-depth on The Money Multiplier Method and teaching individuals how to break the bonds of financial slavery they don't even realize they are in! This is a method that he travels all around the country to teach; how to recycle, recapture, and keep total control of your hard-earned dollars; a method to avoid fractional reserve banking about it! Mr. Kesler will be showing you how to get ALL the money back for every car you will ever buy, drive, and own for you and your family, for the rest of your life.

Social Links:

About MoneyShow

Founded in 1981, MoneyShow is a privately held financial media company headquartered in Sarasota, Florida. As a global network of investing and trading education, MoneyShow presents an extensive agenda of live and online events that attract over 75,000 investors, traders and financial advisors around the world. We are proud to bring together individuals, top market experts, analysts and media in dynamic, face-to-face and online learning forums that include highly acclaimed investment shows, conferences, and cruises.

For more than three decades, we've been empowering individuals with a passion for investing and trading. We arm individual investors and traders with state-of-the-art tools, a powerful skill set and a clear understanding of the markets so they can pave their own path to profitability.

#Investing#InvestSmarter#MoneyMultiplier

Social Links:

About MoneyShow

Founded in 1981, MoneyShow is a privately held financial media company headquartered in Sarasota, Florida. As a global network of investing and trading education, MoneyShow presents an extensive agenda of live and online events that attract over 75,000 investors, traders and financial advisors around the world. We are proud to bring together individuals, top market experts, analysts and media in dynamic, face-to-face and online learning forums that include highly acclaimed investment shows, conferences, and cruises.

For more than three decades, we've been empowering individuals with a passion for investing and trading. We arm individual investors and traders with state-of-the-art tools, a powerful skill set and a clear understanding of the markets so they can pave their own path to profitability.

#Investing#InvestSmarter#MoneyMultiplier

0:06:56

0:06:56

The Money Multiplier

1:43:39

1:43:39

The Money Multiplier Method | Brent Kesler

1:37:42

1:37:42

RALNA Presents: The Money Multiplier Method With Brent Kesler

1:26:34

1:26:34

The Money Multiplier Method

0:27:12

0:27:12

How to Set Up Your Own Infinite Banking Policy | Podcast 52 | The Money Multiplier

0:23:35

0:23:35

The Money Multiplier Method With Brent Kesler #MakingBank #S6E52

1:09:01

1:09:01

The Money Multiplier Method - How to keep, grow and multiply your money!

0:02:50

0:02:50

The Myth of the Money Multiplier - How Banking Really Works

0:02:56

0:02:56

Macro Minute -- The Money Multiplier

1:33:45

1:33:45

RALNA presents: The Money Multiplier Method With Brent Kesler

1:01:50

1:01:50

The Money Multiplier Method

1:40:45

1:40:45

The Money Multiplier Method w/ Brent Kesler!

0:32:44

0:32:44

Making YOU the Bank with The Money Multiplier Method with Brent Kesler

0:43:07

0:43:07

Infinite Banking Concept | Podcast Ep. 1 | The Money Multiplier

1:11:41

1:11:41

The Money Multiplier Method - Become Your Own Bank

0:03:49

0:03:49

The Money Multiplier Method (Canada)

0:04:31

0:04:31

Money Multiplier Method - [PART 1 of 10]

0:05:21

0:05:21

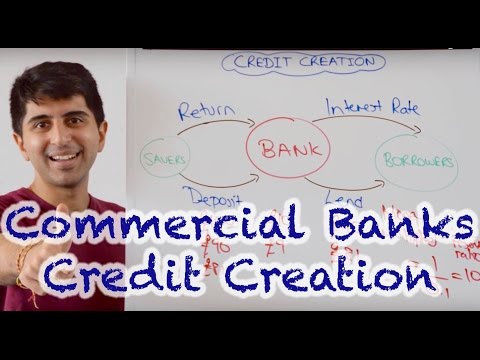

Credit Creation and the Money Multiplier - How do Commercial Banks Make Money?

0:04:08

0:04:08

Infinite Banking Strategy | The Money Multiplier

1:52:21

1:52:21

The Money Multiplier Method Presentation

1:40:14

1:40:14

The Money Multiplier w. Brent Kesler | FIBI Pasadena 2.20.20

1:23:59

1:23:59

Infinite Banking Explained - The Money Multiplier Method

0:05:15

0:05:15

Becoming Your Own Banker | The Money Multiplier

0:01:59

0:01:59

The Money Supply (Monetary Base, M1 and M2) Defined & Explained in One Minute

Комментарии