filmov

tv

Closing Entries Definition - What are Closing Entries?

Показать описание

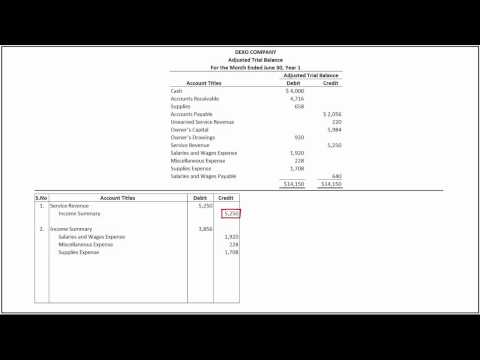

Closing entries definition including break down of areas in the definition. Analyzing the definition of key term often provides more insight about concepts. Closing entries can be defined as: Entries recorded at the end of each accounting period to transfer end-of-period balances in revenue, gain, expense, loss, and withdrawal (dividend for a corporation) accounts to the capital account (to retained earnings for a corporation). The closing process happens at the end of the accounting cycle after financial statements are created the temporary account needing to be closed out so that the new accounting process can start. The closing process will close out temporary accounts, temporary account including income statement accounts and the draws accounts. The reason temporary accounts need to be closed is that they report how the company is doing over time. Once the time period has ended these accounts need to be adjusted to zero, or closed out, so that the new time period can start.

Why Learn Accounting - Financial Accounting / Managerial Accounting

101 Double Entry Accounting System Explained - Accounting Equation

101 Cash vs Accrual - Cash Method / Accrual method differenc

101 Revenue Recognition Principle

Double Entry Accounting System Explained - Balance Sheet

101 Income Statement Introduction

101 Accounting Objectives - Relevance Reliability Comparability

101 Transaction Rules - Accounting Equation

101 Transaction Throught Process / Steps - Accounting Equation

101 Owner Deposits Cash Transaction Accounting Equation

101 Work Completed for Cash Transaction Accounting Equation

100.110 Pay Employee with Cash Transaction Accounting Equati

200 Debits & Credits Normal Balance - Double Entry Accounting Sy

200 Debits & Credits - One Rule to Rule Them All

Why Learn Accounting - Financial Accounting / Managerial Accounting

101 Double Entry Accounting System Explained - Accounting Equation

101 Cash vs Accrual - Cash Method / Accrual method differenc

101 Revenue Recognition Principle

Double Entry Accounting System Explained - Balance Sheet

101 Income Statement Introduction

101 Accounting Objectives - Relevance Reliability Comparability

101 Transaction Rules - Accounting Equation

101 Transaction Throught Process / Steps - Accounting Equation

101 Owner Deposits Cash Transaction Accounting Equation

101 Work Completed for Cash Transaction Accounting Equation

100.110 Pay Employee with Cash Transaction Accounting Equati

200 Debits & Credits Normal Balance - Double Entry Accounting Sy

200 Debits & Credits - One Rule to Rule Them All

0:13:59

0:13:59

0:03:00

0:03:00

0:07:15

0:07:15

0:01:33

0:01:33

0:04:13

0:04:13

0:04:20

0:04:20

0:01:01

0:01:01

0:06:24

0:06:24

0:38:58

0:38:58

0:00:16

0:00:16

0:08:27

0:08:27

0:00:15

0:00:15

0:09:34

0:09:34

0:00:20

0:00:20

0:08:31

0:08:31

0:11:07

0:11:07

0:13:26

0:13:26

0:23:42

0:23:42

0:02:06

0:02:06

0:09:21

0:09:21

0:02:21

0:02:21

0:26:37

0:26:37

0:05:01

0:05:01

0:04:34

0:04:34