filmov

tv

DEBT IS CRIPPLING SOUTH AFRICAN CONSUMERS!

Показать описание

According to The Experian Consumer Default Index (CDIx), which measures the rolling default behavior of South African consumers with Home Loans, Vehicle Loan, Personal Loan, Credit Card, and Retail Loan accounts, as of the end of 2023, South African households had close to R2 trillion in outstanding debt, with R25.8 billion being in default.

Something concerning is happening—Experian says that mid-to-high-affluence consumers, who normally qualify for high-end credit products and home loans, are finding it increasingly difficult to repay debt and continue to use their credit cards extensively.

There has also been a surge in Debt Review applications in South Africa, as higher-affluence consumer groups are increasingly struggling to honor their debt commitments.

In many instances, despite various avenues available where consumers can seek assistance, households are avoiding it, leaving debt to spiral out of control.

Collectively, South African households owed a mind-boggling R305bn in arrears to local municipalities as of December 2022 (reported by the National Treasury). This greatly impacts service delivery and contributes to major challenges in maintenance and infrastructure in our country.

FNB estimates that it takes an average of five days for a middle-income consumer to spend up to 80% of their monthly salary.

From the same report, we see that the average middle-income SA consumer, earning between R180 000 – R500 000 per annum, survives on 20% of their monthly salary for more than 20 days in a month. In addition, salaried middle-income consumers with secured and unsecured credit spend, on average, 30% of their income on unsecured credit and 35% on secured credit.

How are you with your money, do you follow good money habits?

Something concerning is happening—Experian says that mid-to-high-affluence consumers, who normally qualify for high-end credit products and home loans, are finding it increasingly difficult to repay debt and continue to use their credit cards extensively.

There has also been a surge in Debt Review applications in South Africa, as higher-affluence consumer groups are increasingly struggling to honor their debt commitments.

In many instances, despite various avenues available where consumers can seek assistance, households are avoiding it, leaving debt to spiral out of control.

Collectively, South African households owed a mind-boggling R305bn in arrears to local municipalities as of December 2022 (reported by the National Treasury). This greatly impacts service delivery and contributes to major challenges in maintenance and infrastructure in our country.

FNB estimates that it takes an average of five days for a middle-income consumer to spend up to 80% of their monthly salary.

From the same report, we see that the average middle-income SA consumer, earning between R180 000 – R500 000 per annum, survives on 20% of their monthly salary for more than 20 days in a month. In addition, salaried middle-income consumers with secured and unsecured credit spend, on average, 30% of their income on unsecured credit and 35% on secured credit.

How are you with your money, do you follow good money habits?

0:07:49

0:07:49

DEBT IS CRIPPLING SOUTH AFRICAN CONSUMERS!

0:09:28

0:09:28

HOW I GOT OUT OF DEBT REVIEW|MY STORY|SA YOUTUBER

0:09:18

0:09:18

'I had a DEBT of $800,000 Dollars' How to Pay off your Debts | Robert Kiyosaki

0:12:11

0:12:11

Debt Consolidation | South African Youtuber

0:13:07

0:13:07

Rand Manipulation: How The Banks Screwed Over South Africa

0:02:34

0:02:34

Service Delivery | Enoch Mgijima Local Municipality grappling with crippling debt

0:12:41

0:12:41

The 10 Most Indebted African Countries. DROWNING IN DEBTS.

0:02:23

0:02:23

Loan sharks prey on poor South Africans

0:10:34

0:10:34

Debt Review Process

0:10:11

0:10:11

How To Make Money With Debt (2024)

0:03:19

0:03:19

Tongaat Hulett Faces Uphill Battle Amid Business Rescue Trouble and Crippling Debt

0:22:24

0:22:24

Financial Freedom | My strategies to reach Financial Freedom | Debt, Savings & Living below my m...

0:06:25

0:06:25

How Do I Pay Off Debt When I Can't Afford The Minimum Payments?

0:03:38

0:03:38

Budget 2023 | Focus was on crippling electricity crisis and Eskom's high debt

0:03:00

0:03:00

WHO IS RESPONSIBLE FOR A DECEASED PERSON'S DEBT?

0:03:49

0:03:49

Louisiana woman accused of refusing to return $1.2M after bank error

0:05:25

0:05:25

What's The Fastest Way To Pay Off Debt?

0:02:53

0:02:53

WION Fineprint: South Africa crippling energy crisis deepens, protests in Johannesburg | World News

0:02:05

0:02:05

17-Year-Old Returns Woman’s Lost Purse and Gets $3K Reward

0:15:10

0:15:10

South African University Students Crippled By Government-Made Disaster

0:13:03

0:13:03

Why China Is in Africa - If You Don’t Know, Now You Know | The Daily Show

0:43:15

0:43:15

#NoToGalamsey: Prof. Bokpin Explains How The Menace Is Crippling Economy and Citizens’ Pockets

0:10:22

0:10:22

I Married My Sister To Save My Family Now We Have 4 Children : THE SIBLINGS COUPLE

0:01:38

0:01:38

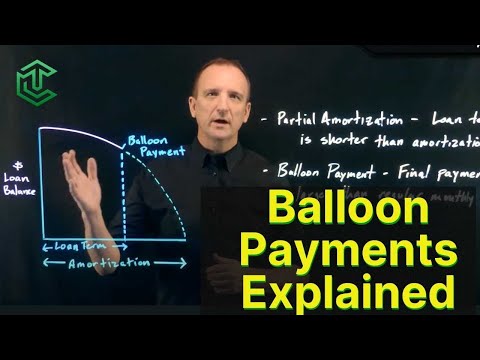

Balloon Payment Explained

Комментарии