filmov

tv

Modeling multivariate time series in economics: Autoregressions versus Recurrent Neural Networks

Показать описание

On August 23-24, 2018 the CMSA hosted our fourth annual Conference on Big Data. The Conference featured many speakers from the Harvard community as well as scholars from across the globe, with talks focusing on computer science, statistics, math and physics, and economics.

Speaker: Sergiy Verstyuk

Title: Modeling multivariate time series in economics: Autoregressions versus Recurrent Neural Networks

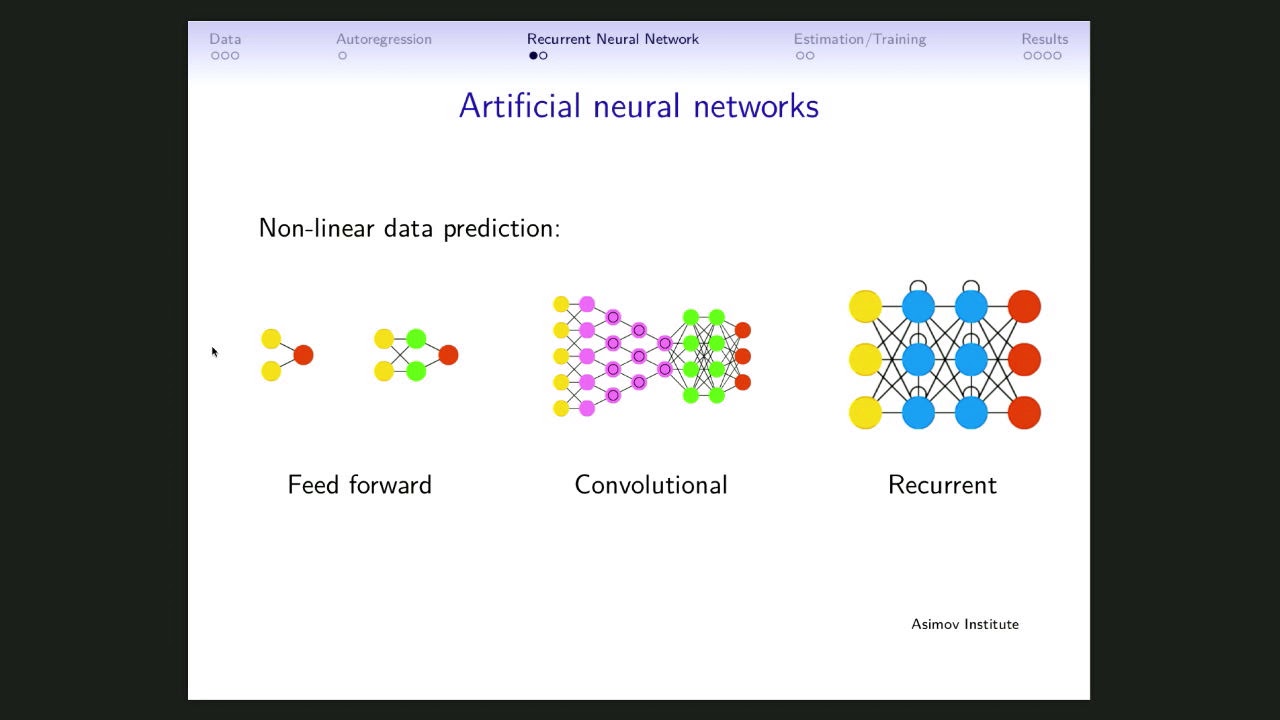

Abstract: Non-structural empirical modeling is important in economics. It is used extensively for such tasks as forecasting and policy analysis. I apply vector autoregression and multivariate recurrent neural network methods to economic variables and compare their results.

Speaker: Sergiy Verstyuk

Title: Modeling multivariate time series in economics: Autoregressions versus Recurrent Neural Networks

Abstract: Non-structural empirical modeling is important in economics. It is used extensively for such tasks as forecasting and policy analysis. I apply vector autoregression and multivariate recurrent neural network methods to economic variables and compare their results.

0:10:00

0:10:00

What are Multivariate Time Series Models || Data Science

0:22:40

0:22:40

181 - Multivariate time series forecasting using LSTM

0:34:20

0:34:20

Modeling multivariate time series in economics: Autoregressions versus Recurrent Neural Networks

0:07:38

0:07:38

Vector Auto Regression : Time Series Talk

0:00:31

0:00:31

mTSeer: Interactive Visual Exploration of Models on Multivariate Time-series Forecast

0:15:00

0:15:00

Multi-Variate Time Series Forecasting (VAR Model)| Complete Python Tutorial

0:05:11

0:05:11

What is the Vector Autoregressive (VAR) Model

0:34:42

0:34:42

Multivariate Time series using Vector Autoregression (VAR)

0:25:29

0:25:29

End to End Multivariate Time Series Modeling using LSTM

0:11:37

0:11:37

Time Series Forecasting Made Easy Using Dart Library - Perform Multivariate Forecasting In No Time

0:15:14

0:15:14

Univariate and Multivariate Time Series Forecasting With Facebook Prophet | Satyajit Pattnaik

0:32:27

0:32:27

Multivariate time series (QRM Chapter 14)

1:08:14

1:08:14

Multivariate Time Series Forecasting Using LSTM, GRU & 1d CNNs

0:13:52

0:13:52

Time Series Forecasting with Machine Learning

0:26:55

0:26:55

Multivariate Time Series Modeling using Facebook Prophet

0:07:29

0:07:29

What is Time Series Analysis?

0:04:33

0:04:33

R26 Creating a Multivariate Time Series in R World Development Indicators, Part III, R and RStudio

0:19:45

0:19:45

A Transformer-based Framework for Multivariate Time Series Representation Learning

1:13:46

1:13:46

Professor Mike West: Structured Dynamic Graphical Models & Scaling Multivariate Time Series

0:02:15

0:02:15

Toeplitz Inverse Covariance-Based Clustering of Multivariate Time Series Data

0:03:18

0:03:18

Rules from Multivariate Time Series

0:23:09

0:23:09

Time Series Forecasting with XGBoost - Use python and machine learning to predict energy consumption

0:05:28

0:05:28

mTSeer: Interactive Visual Exploration of Models on Multivariate Time-series Forecast

0:00:55

0:00:55

How Can I Model Multivariate Time Series with Facebook Prophet?

Комментарии