filmov

tv

Lecture 1: Introduction

Показать описание

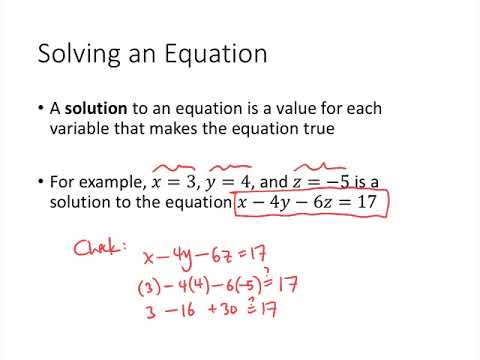

Lecture 1 of the series Optimization in vector spaces for economists serves as the introduction. First of all, we go over the textbook and the set of additional readings. Second, we understand that when describing and solving optimization problems in economics, especially in dynamic programming and optimal control, we work in various vector spaces. In the second part of the introduction, therefore, we line up four examples to illustrate the diversity of vector spaces we work with in optimization problems. The first example is the basic static income allocation problem we are all familiar with from elementary microeconomics. Then we jump to more advanced examples of the utility maximizing economy to identify the relevant vector spaces of infinite sequences and continuous functions to work with in dynamic programming and optimal control. In the final example for the day, we turn to an example from variational calculus just to mention the third major technique in solving dynamic optimization problems. The archetype of this problem is by Eisner and Strotz who were the first to apply strictly convex investment cost functions to penalize too rapid capital adjustment hence to force the firm to take a staggered capital adjustment path. This idea has proved to be of profound influence in the subsequent literature of firm investment. These examples taken together help the students to embark on more advanced topics in deterministic dynamic programming.

Title page:(00:00)

Agenda:(00:10)

An introduction to the introduction:(06:22)

Optimization by vector space methods:(10:29)

Example 1. Static income allocation:(24:41)

A draft solution of Example 1:(26:35)

Example 2. Utility maximization in dynamic programming:(33:41)

A draft solution of Example 2:(37:41)

Example 3. Utility maximization in optimal control:(58:56)

A draft solution of Example 3:(60:06)

Example 4. Utility maximization in variational calculus with convex costs:(68:57)

A draft solution of Example 4:(74:43)

Title page:(00:00)

Agenda:(00:10)

An introduction to the introduction:(06:22)

Optimization by vector space methods:(10:29)

Example 1. Static income allocation:(24:41)

A draft solution of Example 1:(26:35)

Example 2. Utility maximization in dynamic programming:(33:41)

A draft solution of Example 2:(37:41)

Example 3. Utility maximization in optimal control:(58:56)

A draft solution of Example 3:(60:06)

Example 4. Utility maximization in variational calculus with convex costs:(68:57)

A draft solution of Example 4:(74:43)

1:19:35

1:19:35

Lecture 1: Introduction

0:56:15

0:56:15

Lecture 1: Introduction to Power and Politics in Today’s World

1:16:07

1:16:07

Lecture 1: Introduction to Superposition

1:03:53

1:03:53

Lecture #1: Introduction — Brandon Sanderson on Writing Science Fiction and Fantasy

0:46:28

0:46:28

DVD - Lecture 1: Introduction

1:17:25

1:17:25

Lecture 1: Introduction to Cryptography by Christof Paar

0:29:32

0:29:32

Biochemistry Lecture 1 Introduction

0:24:46

0:24:46

Biomechanics Lecture 1: Intro

0:29:25

0:29:25

CCC Chapter-6 Introduction to Internet & WWW (Part-1) | CCC Chapter-Wise Questions | CCC Lecture...

2:38:28

2:38:28

Lecture: Biblical Series I: Introduction to the Idea of God

0:58:44

0:58:44

Lecture 1: Introduction and Overview I (14.13 Psychology and Economics, Spring 2020)

0:34:03

0:34:03

Lecture 1: Introduction to Private Pilot Ground School

0:36:42

0:36:42

Lecture 1 Introduction to Operations Management

0:10:12

0:10:12

Linear Algebra - Lecture 1 - Introduction

0:33:10

0:33:10

Lecture 1 Part 1 - Introduction

1:29:11

1:29:11

Classical Mechanics | Lecture 1

0:48:17

0:48:17

Lecture 1: Course Overview + The Shell (2020)

1:35:47

1:35:47

Cosmology Lecture 1

0:22:39

0:22:39

Introduction to Philosophy (PHI 101: Lecture 1)

1:03:08

1:03:08

Lecture 1, Introduction to History Painting

0:01:52

0:01:52

L01.1 Lecture Overview

0:47:48

0:47:48

Introduction to University Mathematics: Lecture 1 - Oxford Mathematics 1st Year Student Lecture

0:39:32

0:39:32

Lecture 1 : Introduction

0:39:13

0:39:13

Introduction to Radar Systems – Lecture 1 – Introduction; Part 1

Комментарии