filmov

tv

A Balanced Portfolio Destroyed My Parents' Retirement

Показать описание

The balanced, diversified portfolios advertised by big firms aren't as secure and reliable as one might assume.

Mike explains how a balanced portfolio destroyed his parents' retirement.

______________________

******

______________________

Mike:

When he went to the, his advisor, his advisor gave him the same advice you get today. If today you go to, you know, one of these big firms, they're all gonna tell you basically the same thing. They're gonna say, here's what you should do. You should take that $300,000 and you should have a diversified portfolio where approximately the numbers may change a little bit, but approx, ultimately 60% is in some diversified mix of stocks. And the other 40% is in a diversified mix of fi, which stands for fixed income or bonds. That's what the industry told my parents. It's the same thing. They tell them today. It's like, if hello to them today, they're gonna tell you something pretty darn close to that. Here's what happened to my parents. Remember they retired January 1st, 1999. And do you know what the stock market earned in 1999? It was like 20%, right?

Mike:

Mike:

Right. That's when like tech companies going under left and right doc then NASDAQ lost 75% of its value in like a year and a year and a half then 2001. Anyone remember nine? Yeah. What kind of impact did that have on the stock market? And then 2002, we had a recession in those three years, the stock market was down, you know, anywhere from 45% to 75%, the market got crushed right over, not fast. It was over three years. We started wondering if the market was ever gonna go up again. What was happening to my parents? Because remember what were they doing each of these years? It was like, well, we're, we're at three 20. Well, we gotta take out 12 K we gotta take out 12 K and we gotta take out 12 K right? We gotta take out $36,000 over those years. And we were having a loss loss loss. How much money do you think they had left over four years in retirement because remember the first year, 1999 was good year. Now we're four years into retirement. Now think about this. My dad worked for 30 some years at state farm. It took him over 30 you years just to get to this 300,000 number up here. How much did he have? Four years in retirement?

Mike explains how a balanced portfolio destroyed his parents' retirement.

______________________

******

______________________

Mike:

When he went to the, his advisor, his advisor gave him the same advice you get today. If today you go to, you know, one of these big firms, they're all gonna tell you basically the same thing. They're gonna say, here's what you should do. You should take that $300,000 and you should have a diversified portfolio where approximately the numbers may change a little bit, but approx, ultimately 60% is in some diversified mix of stocks. And the other 40% is in a diversified mix of fi, which stands for fixed income or bonds. That's what the industry told my parents. It's the same thing. They tell them today. It's like, if hello to them today, they're gonna tell you something pretty darn close to that. Here's what happened to my parents. Remember they retired January 1st, 1999. And do you know what the stock market earned in 1999? It was like 20%, right?

Mike:

Mike:

Right. That's when like tech companies going under left and right doc then NASDAQ lost 75% of its value in like a year and a year and a half then 2001. Anyone remember nine? Yeah. What kind of impact did that have on the stock market? And then 2002, we had a recession in those three years, the stock market was down, you know, anywhere from 45% to 75%, the market got crushed right over, not fast. It was over three years. We started wondering if the market was ever gonna go up again. What was happening to my parents? Because remember what were they doing each of these years? It was like, well, we're, we're at three 20. Well, we gotta take out 12 K we gotta take out 12 K and we gotta take out 12 K right? We gotta take out $36,000 over those years. And we were having a loss loss loss. How much money do you think they had left over four years in retirement because remember the first year, 1999 was good year. Now we're four years into retirement. Now think about this. My dad worked for 30 some years at state farm. It took him over 30 you years just to get to this 300,000 number up here. How much did he have? Four years in retirement?

0:08:22

0:08:22

A Balanced Portfolio Destroyed My Parents' Retirement

0:04:58

0:04:58

What Is the Best Way to Keep My Portfolio Balanced?

0:08:57

0:08:57

How Long Would It Take A Balanced Portfolio To Break Even in a Market Crash?

0:03:56

0:03:56

A Balanced Portfolio Will Always Make Money | Ray Dalio Interview

0:11:05

0:11:05

Why Retirees Need a Balanced Portfolio

0:01:00

0:01:00

The Biggest Portfolio Mistake Destroying Your Returns! | Fix It Now! 🚨📉 #sathishspeaks

0:00:48

0:00:48

How Many Stocks Should You Have In An Ideal Portfolio @bmtheequitydesk #shorts

0:10:43

0:10:43

I spent HOURS testing retirement portfolios. I learned these secrets!

0:23:10

0:23:10

This is What a Real $3.2M Retirement Portfolio Looks Like

0:08:54

0:08:54

This Score Could Destroy Your Portfolio – Trading 212 Rebalancing

0:00:28

0:00:28

How does Andy Hagans balance his public vs. private investment portfolio?

0:04:44

0:04:44

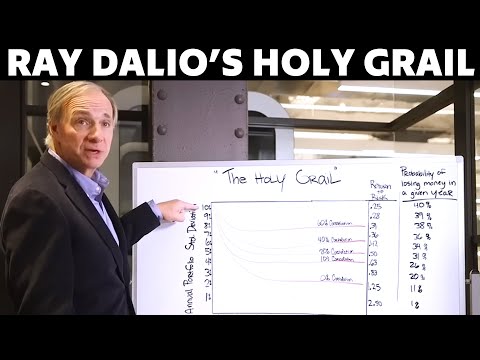

Ray Dalio Breaks Down His 'Holy Grail'

0:07:58

0:07:58

How To Create A Balanced Portfolio That Brings Profits | A Beginner Step By Step Guide

0:13:26

0:13:26

88% Of Your Roth IRA Returns Depend On This

0:02:20

0:02:20

Creating a balanced portfolio is the key to investment success

0:15:31

0:15:31

100% Stocks Portfolio: Smart Strategy or Risky Bet for Retirees?

0:48:39

0:48:39

LeBron James ATTACKS Stephen A. Smith | Candace Ep 156

0:21:31

0:21:31

Roasting My Subscribers’ Investment Portfolios

0:19:41

0:19:41

The Fed Just Killed Your Portfolio

0:05:18

0:05:18

How to Invest Once You Retire | Julia Lembcke, CFP® | URS Advisory

0:00:58

0:00:58

How to Make $100 Per Month in Dividends #shorts

0:18:21

0:18:21

How To Build a Financial Portfolio the PROPER Way

0:00:59

0:00:59

RAY DALIO: How To Make Millions in The Market

0:14:05

0:14:05

Balanced Funds vs Target Date Retirement Funds [Retire on Autopilot?]

Комментарии