filmov

tv

Roth Conversions + IRMAA: How to Plan Correctly (Part 1)

Показать описание

Timestamps:

0:00 Roth Conversions + IRMAA

0:17 What is IRMAA?

1:18 2025 IRMAA Brackets

2:05 Step #1 in Retirement Tax Planning

4:21 Difficulties with IRMAA

5:17 A Common IRMAA Mistake

5:54 IRMAA Calculations the Right Way

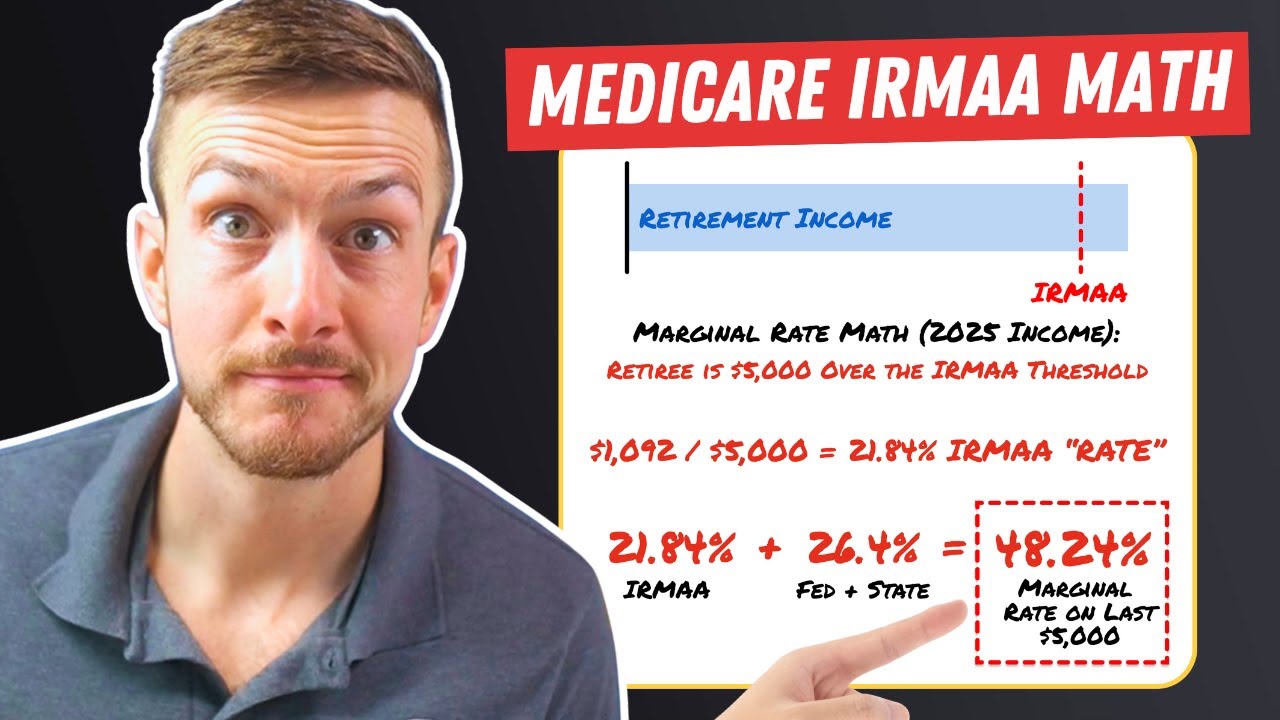

8:07 The Marginal Cost of Each IRMAA Zone

9:18 Best IRMAA Practices

- - - - - - - - - - - - - - - - -

Always remember, "You Don't Need More Money; You Need a Better Plan"

0:11:20

0:11:20

Roth Conversions + IRMAA: How to Plan Correctly (Part 1)

0:09:41

0:09:41

The Trickiest Variable In Roth Conversion Planning | The IRMAA Trap

0:09:38

0:09:38

Roth Conversions and Medicare Surcharges IRMAA

0:05:19

0:05:19

Can I Avoid IRMAA When Doing a Roth Conversion?

0:15:28

0:15:28

A Complete Guide to IRMAA Surcharges & Impact On Roth Conversions

0:04:21

0:04:21

Impact of Roth IRA Conversion on Social Security Benefits and Medicare IRMAA

0:01:52

0:01:52

What Types of Income is IRMAA Based on? How to Avoid the Medicare Surcharge

0:12:30

0:12:30

How to Avoid IRMAA the Right Way! | Medicare IRMAA Calculation Explained

0:08:16

0:08:16

Roth Conversion: Revealing IRMAA Implications

0:12:34

0:12:34

Roth Conversions to a Higher Tax Bracket Than in Retirement? What About IRMAA?

1:50:03

1:50:03

Roth IRA Conversion (Part 4) 2024 Tax Planning Strategies | IRMAA & Stock Trading

0:09:10

0:09:10

Why You SHOULD Take a Medicare Increase Penalty in this Scenario

0:14:50

0:14:50

Watch This Before Roth Converting in 2024…trust me.

0:15:23

0:15:23

Should You Roth Convert into the 32% Bracket for a More Tax Efficient Retirement?

0:00:59

0:00:59

Roth Conversions and IRMAA Explained

0:11:09

0:11:09

Watch This Before Roth Converting in 2023… | Roth Conversion Timing (Part 1)

0:15:27

0:15:27

What if a Roth Conversion causes you to owe a Medicare Penalty?

0:22:39

0:22:39

Is A Roth Conversion Right for You? New Retirement's New Tool Can Help You Decide

0:00:51

0:00:51

What Is IRMAA?: Roth Conversions

0:11:13

0:11:13

Roth Convert 100% of Your IRAs?! 3 Situations Where it Makes Sense...

0:01:00

0:01:00

Roth conversions can help reduce Medicare IRMAA premium surcharges

0:05:35

0:05:35

Should I Convert My Retirement To Roth?

0:10:09

0:10:09

I'm 58. When Should I Do Roth Conversions? [Case Study] ᴴᴰ

0:34:31

0:34:31

Live with Larry: IRMAA & Roth Conversions

Комментарии