filmov

tv

How to AVOID Taxes... Legally (Do This Now)

Показать описание

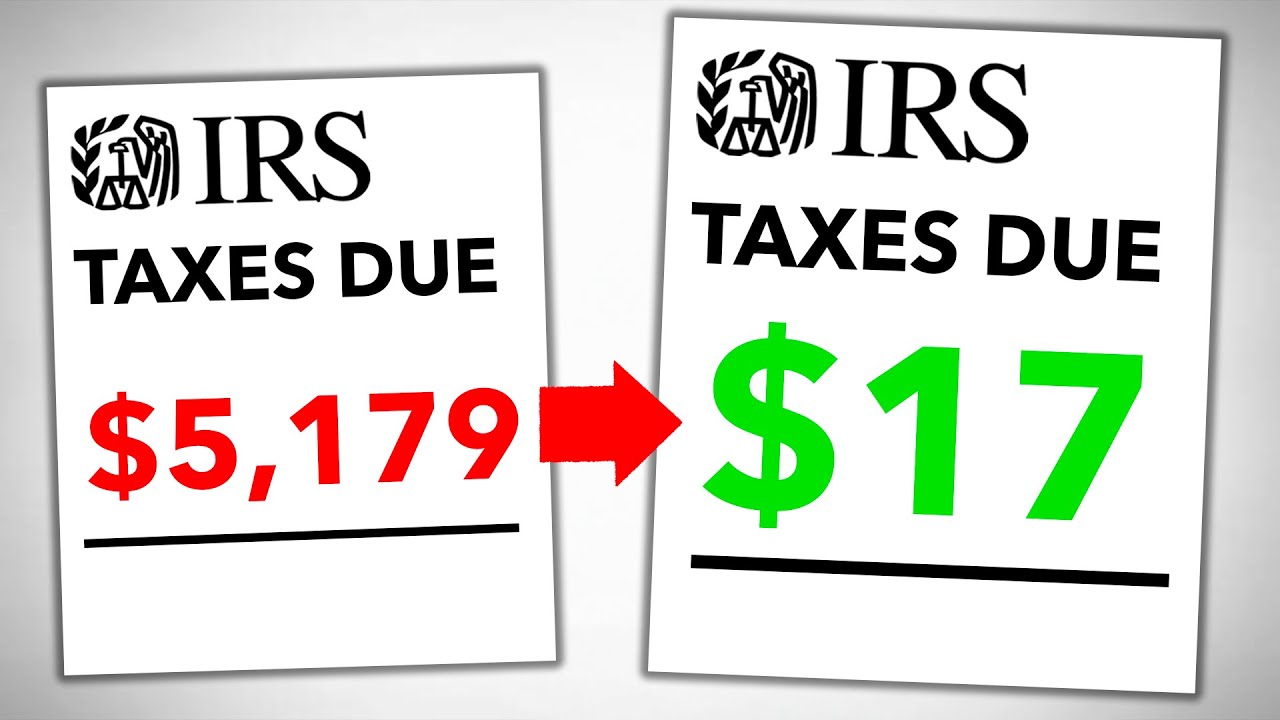

If you ever wanted to avoid or pay less in taxes to the IRS, you probably had no idea where to start. Here are 4.5 of my favorite strategies to pay less in taxes that anyone can understand.

LINKS MENTIONED IN THE VIDEO:

FREE STUFF FROM ME:

LET'S CONNECT:

00:00 Start Here

00:10 Step 1 - The Tax Process

02:25 Step 2 - The “X”

04:34 Step 2.5 - The New Process

06:38 Step 3.5 - Strategic Disbursement

11:03 Step 4.5 - The SBLOC Advantage

______

Some of the links on this page are affiliate links, meaning, at no additional cost to you, I may earn a commission if you click through and make a purchase and/or subscribe. Affiliate commissions help fund videos like this one.

All opinions expressed by Vincent Chan are solely Vincent Chan’s opinions. You should not treat any opinion expressed by Vincent Chan as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Vincent Chan’s opinions are based upon information he considers reliable, but does not warrant its completeness or accuracy, and it should not be relied upon as such. Vincent Chan is not under any obligation to update or correct any information provided. Vincent Chan’s statements and opinions are subject to change without notice.

Past performance is not indicative of future results. Vincent Chan does not guarantee any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment discussed. Strategies or investments discussed may fluctuate in price or value. Investors may get back less than invested. Investments or strategies mentioned may not be suitable for you. This material does not take into account your particular investment objectives, financial situation or needs and is not intended as recommendations appropriate for you. You must make an independent decision regarding investments or strategies mentioned. Before acting on information, you should consider whether it is suitable for your particular circumstances and strongly consider seeking advice from your own financial or investment adviser.

LINKS MENTIONED IN THE VIDEO:

FREE STUFF FROM ME:

LET'S CONNECT:

00:00 Start Here

00:10 Step 1 - The Tax Process

02:25 Step 2 - The “X”

04:34 Step 2.5 - The New Process

06:38 Step 3.5 - Strategic Disbursement

11:03 Step 4.5 - The SBLOC Advantage

______

Some of the links on this page are affiliate links, meaning, at no additional cost to you, I may earn a commission if you click through and make a purchase and/or subscribe. Affiliate commissions help fund videos like this one.

All opinions expressed by Vincent Chan are solely Vincent Chan’s opinions. You should not treat any opinion expressed by Vincent Chan as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Vincent Chan’s opinions are based upon information he considers reliable, but does not warrant its completeness or accuracy, and it should not be relied upon as such. Vincent Chan is not under any obligation to update or correct any information provided. Vincent Chan’s statements and opinions are subject to change without notice.

Past performance is not indicative of future results. Vincent Chan does not guarantee any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment discussed. Strategies or investments discussed may fluctuate in price or value. Investors may get back less than invested. Investments or strategies mentioned may not be suitable for you. This material does not take into account your particular investment objectives, financial situation or needs and is not intended as recommendations appropriate for you. You must make an independent decision regarding investments or strategies mentioned. Before acting on information, you should consider whether it is suitable for your particular circumstances and strongly consider seeking advice from your own financial or investment adviser.

0:06:07

0:06:07

How the rich avoid paying taxes

0:10:41

0:10:41

How to Avoid Taxes Legally in The US (Do This Now!)

0:13:54

0:13:54

How to AVOID Taxes... Legally (Do This Now)

0:00:46

0:00:46

How to AVOID paying taxes (LEGAL)

0:13:37

0:13:37

How Big Earners Reduce their Taxes to Zero

0:10:57

0:10:57

How to Avoid Taxes Legally in the U.S.

0:10:15

0:10:15

How to (LEGALLY) Pay $0 In Taxes | Why The Rich Don’t Pay Taxes?

0:00:30

0:00:30

How Large Companies Avoid Taxes legally 😯

0:00:57

0:00:57

How Rich People LEGALLY Pay NO Taxes!

0:13:13

0:13:13

7 Ways To (LEGALLY) Avoid Taxes | Tax Loopholes Of The Rich

0:07:20

0:07:20

How to Avoid Paying Taxes LEGALLY

0:20:19

0:20:19

15 Ways Rich People AVOID Paying Taxes

0:14:12

0:14:12

5 ways to avoid taxes...legally

0:10:29

0:10:29

How Rich People Avoid Paying Taxes - Robert Kiyosaki and Tom Wheelwright @TomWheelwrightCPA

0:00:41

0:00:41

How To Avoid Paying Taxes...Legally

0:09:12

0:09:12

How to AVOID Taxes (Legally) When you SELL Stocks

0:11:08

0:11:08

How The Rich Avoid Paying Taxes

0:27:35

0:27:35

How To (LEGALLY) Never Pay Taxes - Do This Today

0:09:18

0:09:18

CPA Explains Secrets To AVOID Taxes... Legally (Do This Now!)

0:12:36

0:12:36

IRS 'You'll NEVER Need to Pay Taxes Again... Legally'

1:28:39

1:28:39

How To Avoid Taxes (Legally) as a Real Estate Investor

0:03:59

0:03:59

How the rich avoid paying taxes - the Augusta Rule LOOPHOLE

0:04:00

0:04:00

Get An LLC To Avoid Paying High Taxes?

0:11:21

0:11:21

10 Ways Billionaires Avoid Tax On A Massive Scale - How Money Works

Комментарии