filmov

tv

Budgeting Basics - Types of Budgets (2/3)

Показать описание

In this video, I’ll share a bunch of different kinds of budgeting systems.

Please subscribe and leave comments below!

Hi, everyone! This is Lara Hammock from the Marble Jar channel and in today’s video, I’ll talk about a bunch of different kinds of budgeting systems. This is the second in a three part series.

The first video in this series covers the basics of budgeting — what is it, why would you do, it and how does it work. For many people, budgeting is about as appealing as dieting. Which is to say — not very. In fact — they ARE very similar processes — in both you are required to follow a set of rules that change your behavior in order to achieve a goal — either to lose weight in the case of dieting or to save money, in the case of budgeting. As you know, there are a BILLION different diets out there - Atkins, South Beach, Weight Watchers, Keto, etc. Believe it or not — there are practically as many ways to budget as well. In the same way that not all diets work for everyone — not all budgeting systems work for everyone either.

In this video, I want to give you a high level overview of several different budgeting systems. The key is finding the system that works best for you with your unique brain, your lifestyle, and your goals. So, first off — just a quick visual to show what budgeting accomplishes for you. This is your income. Some portion of your income should be saved for short and long term savings — let’s say 30%. The remainder — this 70% can be used for living expenses. A budget helps you to determine how you are dividing up your living expenses now and how you want to divide that money up. For example, let’s say to make things easy, your income is $1,000 — you’ll notice that I haven’t given a time frame since different budgets use different time frames -- but generally budgets tend to be monthly. You put $300 of your $1,000 aside for savings. How do you split up this $700? $300 goes towards rent, $200 food, $25 gasoline, etc. These are called budget categories. First you have to figure out how you are actually using this money now and then you determine your plan for how you want to split this money up going forward.

Generally speaking, the more detailed and complicated the system, the more control you have, but the harder it is to maintain. The trick is finding the right balance for yourself.

Okay — let’s go through some of the budgeting systems! First

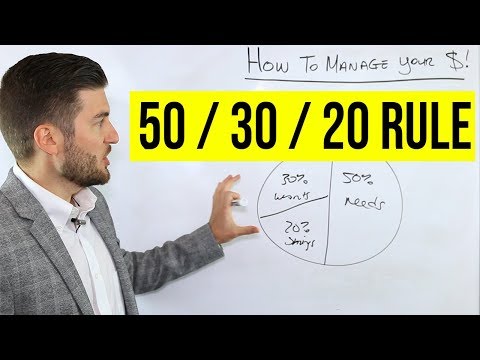

50/30/20

This budget system is both prescriptive and simple. The idea is that 50% of your income (after tax, of course) should be going to needs (mortgage, utilities, transportation, groceries, basic clothing), 30% should be going to wants (Netflix, dining out, electronics, etc.), and 20% should go towards goals or savings. There are only 3 budget categories, so it is simple and should be pretty easy to maintain. It may not be great for those who need more detailed info about where they can make cuts in their spending.

Zero Based

Zero Based budgeting was popularized by Dave Ramsey. It’s both a philosophy and a system. It requires that you set a new budget each month based on your projected income and expenses. The philosophy part is that it requires that you plan where every dollar will go. In other words, you establish in advance how each dollar will be used so that you are incredibly intentional about savings, goal planning, and expenses. A zero based budget never has anything “left over” — income minus spending/savings should equal zero. The unique component of this system is the fact that you set up a new budget every month, which helps you to stay on track and to know where every dollar is going.

Paycheck Budgeting

While most budgets tend to be monthly since we pay most of our bills monthly, paycheck budgeting uses your paycheck as the budgeting period. Say you get paid twice a month. Each of the monthly expenses like rent, car payment, or utilities is assigned to one of your paychecks with portions of ongoing expenses like groceries and gasoline being allocated as well. It has the benefit of being more concrete in matching income directly to expenses and covers a shorter time period, which can make it easier to control expenses. The drawback is that it requires more planning and calendaring then a monthly plan. . .

Please subscribe and leave comments below!

Hi, everyone! This is Lara Hammock from the Marble Jar channel and in today’s video, I’ll talk about a bunch of different kinds of budgeting systems. This is the second in a three part series.

The first video in this series covers the basics of budgeting — what is it, why would you do, it and how does it work. For many people, budgeting is about as appealing as dieting. Which is to say — not very. In fact — they ARE very similar processes — in both you are required to follow a set of rules that change your behavior in order to achieve a goal — either to lose weight in the case of dieting or to save money, in the case of budgeting. As you know, there are a BILLION different diets out there - Atkins, South Beach, Weight Watchers, Keto, etc. Believe it or not — there are practically as many ways to budget as well. In the same way that not all diets work for everyone — not all budgeting systems work for everyone either.

In this video, I want to give you a high level overview of several different budgeting systems. The key is finding the system that works best for you with your unique brain, your lifestyle, and your goals. So, first off — just a quick visual to show what budgeting accomplishes for you. This is your income. Some portion of your income should be saved for short and long term savings — let’s say 30%. The remainder — this 70% can be used for living expenses. A budget helps you to determine how you are dividing up your living expenses now and how you want to divide that money up. For example, let’s say to make things easy, your income is $1,000 — you’ll notice that I haven’t given a time frame since different budgets use different time frames -- but generally budgets tend to be monthly. You put $300 of your $1,000 aside for savings. How do you split up this $700? $300 goes towards rent, $200 food, $25 gasoline, etc. These are called budget categories. First you have to figure out how you are actually using this money now and then you determine your plan for how you want to split this money up going forward.

Generally speaking, the more detailed and complicated the system, the more control you have, but the harder it is to maintain. The trick is finding the right balance for yourself.

Okay — let’s go through some of the budgeting systems! First

50/30/20

This budget system is both prescriptive and simple. The idea is that 50% of your income (after tax, of course) should be going to needs (mortgage, utilities, transportation, groceries, basic clothing), 30% should be going to wants (Netflix, dining out, electronics, etc.), and 20% should go towards goals or savings. There are only 3 budget categories, so it is simple and should be pretty easy to maintain. It may not be great for those who need more detailed info about where they can make cuts in their spending.

Zero Based

Zero Based budgeting was popularized by Dave Ramsey. It’s both a philosophy and a system. It requires that you set a new budget each month based on your projected income and expenses. The philosophy part is that it requires that you plan where every dollar will go. In other words, you establish in advance how each dollar will be used so that you are incredibly intentional about savings, goal planning, and expenses. A zero based budget never has anything “left over” — income minus spending/savings should equal zero. The unique component of this system is the fact that you set up a new budget every month, which helps you to stay on track and to know where every dollar is going.

Paycheck Budgeting

While most budgets tend to be monthly since we pay most of our bills monthly, paycheck budgeting uses your paycheck as the budgeting period. Say you get paid twice a month. Each of the monthly expenses like rent, car payment, or utilities is assigned to one of your paychecks with portions of ongoing expenses like groceries and gasoline being allocated as well. It has the benefit of being more concrete in matching income directly to expenses and covers a shorter time period, which can make it easier to control expenses. The drawback is that it requires more planning and calendaring then a monthly plan. . .

0:05:13

0:05:13

Budgeting Basics!

0:06:12

0:06:12

Session 2 - Types of Budgets (Budgeting Basics)

0:08:38

0:08:38

Budgeting Basics - Types of Budgets (2/3)

0:07:16

0:07:16

Budgeting Basics - What, Why & How? (1/3)

0:00:51

0:00:51

50/30/20 Budget Rule for $20/hour #budgeting

0:03:17

0:03:17

Budgeting Basics

0:04:46

0:04:46

What Is A Budget? | Cash Course | PragerU Kids

0:02:06

0:02:06

Budgeting Basics

1:12:38

1:12:38

Economy Revision Series LIVE: Budget | Lecture 2| for UPSC, State PSC and other Govt. Exams

0:00:46

0:00:46

THIS is how you budget!

0:13:53

0:13:53

The One Simple Budgeting Method That Changed My Life

0:06:25

0:06:25

HOW TO: THE EASIEST AND SIMPLEST WAY TO CREATE A MONTHLY BUDGET! 6-MINUTES PROCESS

0:04:25

0:04:25

How Do I Make A Budget And Stick To It?

0:11:37

0:11:37

10 Budgeting Basics – How To Create A Budget

0:42:56

0:42:56

(L029) Basic Budgeting Concepts - Leadership and Management

0:02:26

0:02:26

Making a Budget : What Are the Different Types of Budgeting?

1:01:28

1:01:28

Budgeting Basics- Utah League of Cities and Towns

0:00:55

0:00:55

Budgeting basics - 50/30/20 rule. #financialfreedom #moneytips

0:01:54

0:01:54

Budgeting Basics

0:06:14

0:06:14

Financial Literacy for Kids | Learn the basics of finance and budgeting

0:01:21

0:01:21

Budgeting Basics

0:15:56

0:15:56

Business Budgeting 101 - Learn the basics of business budgeting

0:07:08

0:07:08

How To Manage Your Money (50/30/20 Rule)

0:00:23

0:00:23

My 5 Bank Accounts #budgeting #organizedlife #shorts

Комментарии