filmov

tv

Binomial tree to price option Part 9

Показать описание

Using binomial tree to value american and european call and put options

0:16:51

0:16:51

Binomial Options Pricing Model Explained

0:05:31

0:05:31

CFA Level I Derivatives - Binomial Model for Pricing Options

0:15:39

0:15:39

What is the Binomial Option Pricing Model?

0:21:40

0:21:40

Binomial Option Pricing Model (Calculations for CFA® and FRM® Exams)

0:04:13

0:04:13

Binomial tree to price option Part 1

1:15:58

1:15:58

Chapter 13 - The Binomial Tree Option Pricing Model

0:14:11

0:14:11

Option Pricing Binomial Model

0:14:12

0:14:12

How to Price Options using a Binomial Tree (The Portfolio Approach)

0:05:29

0:05:29

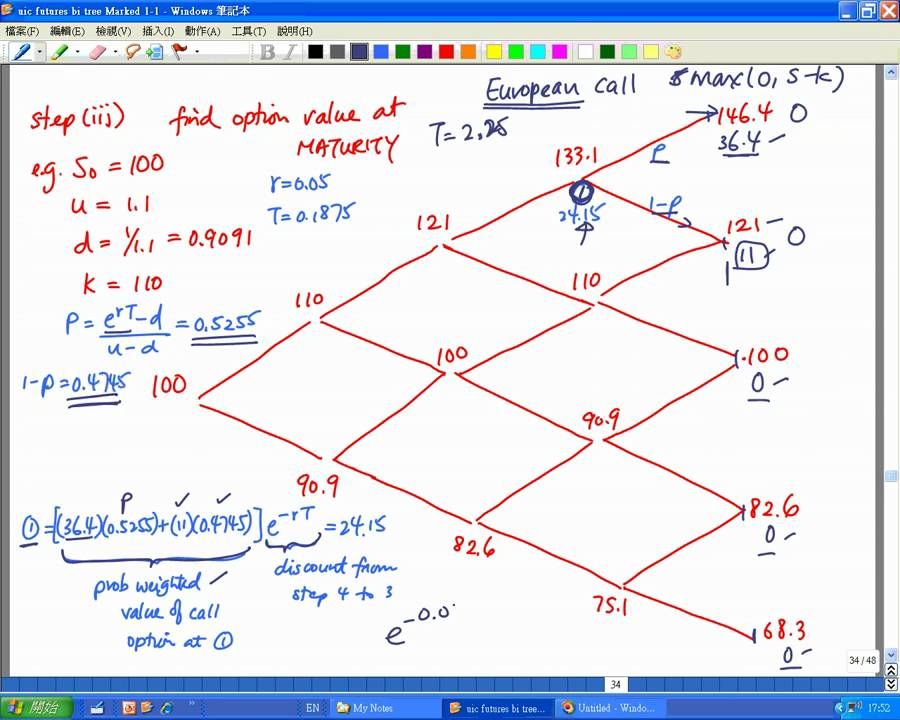

Binomial tree to price option Part 9

0:17:28

0:17:28

How to Choose Binomial Parameters - Binomial Option Pricing || Theory & Implementation in Python

0:11:01

0:11:01

Options pricing video 2 - Binomial method - Two-step - European call option price

0:04:10

0:04:10

Binomial tree to price option Part 13

0:04:20

0:04:20

Binomial tree to price option Part 12

0:04:55

0:04:55

Binomial tree to price option Part 6

0:49:03

0:49:03

Binomial Option Pricing Model || Theory & Implementation in Python

0:03:25

0:03:25

Binomial tree to price option Part 11

0:05:58

0:05:58

Binomial tree to price option Part 10

0:05:13

0:05:13

Binomial tree to price option Part 7

0:05:21

0:05:21

VsCap: How to create a Binomial Model in Excel

0:05:22

0:05:22

Binomial tree to price option Part 8

0:32:06

0:32:06

Binomial Tree to price options

0:06:22

0:06:22

The Cox-Ross-Rubinstein Binomial Option Pricing Model

0:09:35

0:09:35

Pricing American Options using the Binomial Tree Method. - Options Trading Classes

0:05:25

0:05:25

Binomial tree to price option Part 5

Комментарии