filmov

tv

Cross Currency Swap Explained

Показать описание

What Is Cross Currency Swap?

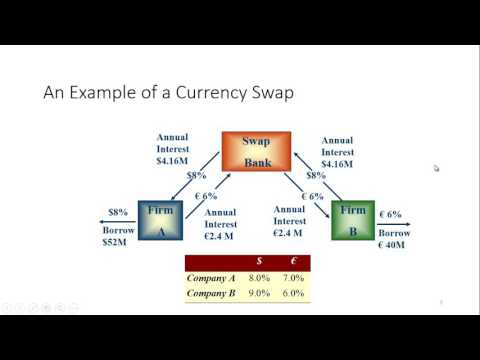

Cross currency swap is a special financial derivative which indicates an agreement between two parties in different countries to swap currencies they borrowed from their domestic market. This means that both parties will get the loan from their domestic banks using their own currency, and then they will swap the debt based on the agreement. Usually, the swap will have a term, say 2 years. During this period, both parties will still need to pay interest payments periodically on the currencies they swapped. For example, an European company A has a Euro loan with an interest rate of 1% and an American company B has a US Dollar loan with an interest rate of 2%. If company A will do a cross currency swap with company B, then company A needs to pay the interest payment of 2% and company B needs to pay 1% accordingly. On the maturity date, the same amount of borrowed principal will be exchanged back.

Why Do Companies Use Cross Currency Swap?

You may have the question. If a company can get foreign currency directly from the foreign loan market, why do they need to do the cross currency swap with a company from another country? The answer is that cross currency swap is based on comparative advantages of borrowing. This means that both parties can borrow money from their domestic currency at a low rate but will be facing a higher cost for borrowing foreign currencies from the foreign loan market. Let's get back to the previous example. European company A can get their Euro loan with a rate of 1% from their domestic market. However, if they want to get a US dollar loan for their US business, they may have to pay a 4% rate from the foreign loan market. At the same time, company B can get a rate of 2% for their US dollar loan from its domestic market, and it also needs to get some Euro loans for their expansion in Europe. However, they need to pay 3% for the Euro loan if they do it from the foreign loan market. If that is the case, they can easily swap their loan with the low rates and get the currencies they need, and both parties can enjoy more favorable rates. Regarding the gain during the process, there is a term called Quality Spread Differential which is used to calculate the actual gain from the cross currency swap compared with direct loan from the foreigh loan market.

From the above example, we can see the final QSD = (4% - 2%) + (%3 - 1%) = 4%. This value means that, through a cross currency swap, the two companies can get a combined 4% gain in total. Let's assume that the exchange rate between Euro and US dollar is 1.2. This means that, at year 0, company A will borrow 1 million Euro and company B will borrow 1.2 million US dollars from their domestic market and those principal will be swapped. Both parties will pay the interest payments based on the counterparty rates over the term, which means company A will pay company B's borrowing rate 2% and vice versa. At maturity date, both the principal will be repaid back which will end the swap obligation.

The Role Of Swap Bank

Although cross currency swap is a good idea to lower the borrowing cost, it is very hard for a company to find a counterparty from another country that needs the same amount and maturity in the foreign market. Swap banks will be working as an agent to help companies in their countries to find matching parties from another country. In exchange, all swap banks will charge some fees for their services. Of course, those fees will be less than the quality spread differential. Otherwise, the parties entering the swap will not get any gain and they will have no incentive to do that.

Benefits & Risks of Cross Currency Swap

Obviously, the biggest benefit of cross currency swap is that both parties can get a favorable loan rate for the foreign currencies. Moreover, swap will be using a fixed exchange rate to repay the loan during the term. This means that both parties can cement the exchange rate at origin on the maturity date, which can eliminate the unfavorable fluctuation of the exchange rate. On the other side, the biggest risk of the Cross Currency Swap is the risk of Counterparty Default Risk from another party. If the counterparty entering the swap fails to meet their payments, the party's credit rating will be negatively affected. A general solution for this issue is to use a swap bank who can thoroughly assess both parties' creditworthiness to ensure their ability to meet their obligations before the swap.

Cross currency swap is a special financial derivative which indicates an agreement between two parties in different countries to swap currencies they borrowed from their domestic market. This means that both parties will get the loan from their domestic banks using their own currency, and then they will swap the debt based on the agreement. Usually, the swap will have a term, say 2 years. During this period, both parties will still need to pay interest payments periodically on the currencies they swapped. For example, an European company A has a Euro loan with an interest rate of 1% and an American company B has a US Dollar loan with an interest rate of 2%. If company A will do a cross currency swap with company B, then company A needs to pay the interest payment of 2% and company B needs to pay 1% accordingly. On the maturity date, the same amount of borrowed principal will be exchanged back.

Why Do Companies Use Cross Currency Swap?

You may have the question. If a company can get foreign currency directly from the foreign loan market, why do they need to do the cross currency swap with a company from another country? The answer is that cross currency swap is based on comparative advantages of borrowing. This means that both parties can borrow money from their domestic currency at a low rate but will be facing a higher cost for borrowing foreign currencies from the foreign loan market. Let's get back to the previous example. European company A can get their Euro loan with a rate of 1% from their domestic market. However, if they want to get a US dollar loan for their US business, they may have to pay a 4% rate from the foreign loan market. At the same time, company B can get a rate of 2% for their US dollar loan from its domestic market, and it also needs to get some Euro loans for their expansion in Europe. However, they need to pay 3% for the Euro loan if they do it from the foreign loan market. If that is the case, they can easily swap their loan with the low rates and get the currencies they need, and both parties can enjoy more favorable rates. Regarding the gain during the process, there is a term called Quality Spread Differential which is used to calculate the actual gain from the cross currency swap compared with direct loan from the foreigh loan market.

From the above example, we can see the final QSD = (4% - 2%) + (%3 - 1%) = 4%. This value means that, through a cross currency swap, the two companies can get a combined 4% gain in total. Let's assume that the exchange rate between Euro and US dollar is 1.2. This means that, at year 0, company A will borrow 1 million Euro and company B will borrow 1.2 million US dollars from their domestic market and those principal will be swapped. Both parties will pay the interest payments based on the counterparty rates over the term, which means company A will pay company B's borrowing rate 2% and vice versa. At maturity date, both the principal will be repaid back which will end the swap obligation.

The Role Of Swap Bank

Although cross currency swap is a good idea to lower the borrowing cost, it is very hard for a company to find a counterparty from another country that needs the same amount and maturity in the foreign market. Swap banks will be working as an agent to help companies in their countries to find matching parties from another country. In exchange, all swap banks will charge some fees for their services. Of course, those fees will be less than the quality spread differential. Otherwise, the parties entering the swap will not get any gain and they will have no incentive to do that.

Benefits & Risks of Cross Currency Swap

Obviously, the biggest benefit of cross currency swap is that both parties can get a favorable loan rate for the foreign currencies. Moreover, swap will be using a fixed exchange rate to repay the loan during the term. This means that both parties can cement the exchange rate at origin on the maturity date, which can eliminate the unfavorable fluctuation of the exchange rate. On the other side, the biggest risk of the Cross Currency Swap is the risk of Counterparty Default Risk from another party. If the counterparty entering the swap fails to meet their payments, the party's credit rating will be negatively affected. A general solution for this issue is to use a swap bank who can thoroughly assess both parties' creditworthiness to ensure their ability to meet their obligations before the swap.

0:04:46

0:04:46

Cross Currency Swap Explained

0:03:08

0:03:08

Cross currency basis swap - CFA level 3 tutorial

0:05:19

0:05:19

Cross-Currency Interest Rate Swap (CCIRS)

0:01:04

0:01:04

QUICK STUDY DERIVATIVES - CROSS CURRENCY SWAP CONTRACT

0:05:13

0:05:13

What are Currency Swaps?

0:10:35

0:10:35

Currency Swaps

0:02:52

0:02:52

How swaps work - the basics

0:14:17

0:14:17

Valuing Cross Currency Swaps (Solved Example) (FRM Part 1, Book 3, Financial Markets and Products)

1:12:09

1:12:09

Hedging Currency Risk Part 1 IIFT

0:02:32

0:02:32

LFS Webcast series - The Mechanics of Cross Currency Basis Swaps

0:08:40

0:08:40

Cross currency swaps - why you get it wrong

0:04:50

0:04:50

Currency Swap Agreement Explained with Example

0:02:47

0:02:47

What is a currency swap?

0:02:09

0:02:09

What is Currency Swap?

0:14:54

0:14:54

What is a swap? - MoneyWeek Investment Tutorials

0:16:08

0:16:08

Currency Swaps - A comprehensive understanding

0:02:47

0:02:47

Central Bank Swap Arrangements, Explained

0:05:05

0:05:05

CFA Level 3 FREE Lesson on Currency Swaps (Derivatives)

0:03:43

0:03:43

What is a Basis Swap?

0:13:15

0:13:15

FX Swaps Explained | FRM Part 1, FRM Part 2 | CFA Level 1, CFA Level 3

0:08:47

0:08:47

Currency Swaps - Explained in Hindi

0:00:48

0:00:48

Bloomberg. Cross currency Swap. Basis Swap.

0:03:51

0:03:51

Interest rate swap 1 | Finance & Capital Markets | Khan Academy

0:07:06

0:07:06

Interest Rate Hedging - Cross Currency Interest Rate Swaps (CCIRS)

Комментарии