filmov

tv

Accounting - for Overheads - Allocation, Apportionment and Absorption rate - AAT

Показать описание

In this video I discuss accounting for overheads through the three stages, allocation, apportionment and absorption. If you are struggling with apportionment of overheads then this video may help. This would be useful to anyone studying AAT Level 3 or Level 4 (AAT level 4).

Overheads can be split into direct costs and indirect costs. Direct costs are directly attributable to a cost centre whereas indirect costs are more difficult to attribute and need to be apportioned across many different cost centres.

Indirect costs can be variable, fixed or semi-variable (which include both fixed and variable elements).

Here I walk you through an example of apportionment with rent of £200k and how we might apportion this across three different cost centres based on their square footage.

We also need to ensure that in the third step of apportionment, we re-charge service cost centre costs to the various other production cost centres.

Here I also discuss rate per unit and the alternative rate of absorption as well as the advantages and disadvantages to the various different cost basis.

Overheads can be split into direct costs and indirect costs. Direct costs are directly attributable to a cost centre whereas indirect costs are more difficult to attribute and need to be apportioned across many different cost centres.

Indirect costs can be variable, fixed or semi-variable (which include both fixed and variable elements).

Here I walk you through an example of apportionment with rent of £200k and how we might apportion this across three different cost centres based on their square footage.

We also need to ensure that in the third step of apportionment, we re-charge service cost centre costs to the various other production cost centres.

Here I also discuss rate per unit and the alternative rate of absorption as well as the advantages and disadvantages to the various different cost basis.

0:19:16

0:19:16

ACCOUNTING FOR OVERHEADS (PART 1)

0:08:49

0:08:49

Accounting - for Overheads - Allocation, Apportionment and Absorption rate - AAT

0:22:59

0:22:59

Accounting for overheads part 1 - ACCA Management Accounting (MA)

0:48:18

0:48:18

ACCA F2/MA - Chapter 7 - Accounting for Overheads (Part 1)

0:26:22

0:26:22

ACCOUNTING FOR OVERHEADS (PART 3)

0:16:37

0:16:37

ACCA FMA - Accounting for Overheads Part 1 | What is the Overhead Method of Accounting in ACCA?

0:04:25

0:04:25

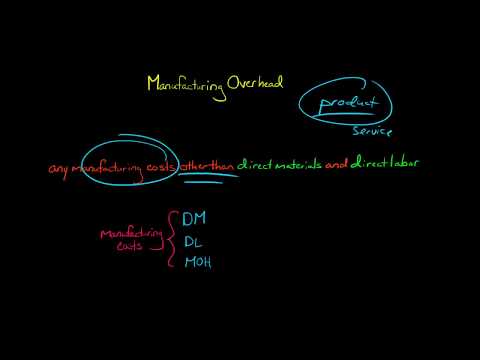

Manufacturing Overhead

0:08:05

0:08:05

ACCOUNTING FOR OVERHEADS (PART 6)

0:00:09

0:00:09

Class 12 account chapter 14 accounting for overheads numerical problems solutions

0:04:15

0:04:15

How to calculate and track overhead costs for your business | Start your business

0:19:07

0:19:07

ACCOUNTING FOR OVERHEADS (PART 2)

0:18:13

0:18:13

ACCOUNTING FOR OVERHEADS (PART 5)

0:21:32

0:21:32

ACCOUNTING FOR OVERHEADS (PART 4)

0:40:14

0:40:14

MANAGEMENT ACCOUNTING (Accounting for overheads) - Reapportionment of of service department OHDs.

0:33:09

0:33:09

Overhead Allocation & Apportionment | Overhead Distribution | CMA | ACCA | CA | CPA |CIA | CIM...

1:35:48

1:35:48

MA { OVERHEADS 1}

0:55:47

0:55:47

ACCA F2/MA - Chapter 7 - Accounting for Overheads (Part 2 complete)

0:41:14

0:41:14

Accounting for Overhead Cost || BBS 2nd year Accounting || Chapter 5 || Format || TU 2076 Solution

0:08:20

0:08:20

MA10 - Predetermined Overhead Rate - Sample problem - Management Accounting

0:04:26

0:04:26

Overhead Definition - What is overhead?

0:27:42

0:27:42

AS/A Level Accounting - Absorption Costing (Part 2 - Allocation and Apportionment of Overheads)

0:10:39

0:10:39

Over & Under Absorbed Overheads | Absorption of Overheads | Overhead Absorption | Absorption Cos...

0:13:01

0:13:01

19. 'Overheads Chapter Introduction' from Cost Accounting Subject

0:49:08

0:49:08

Accounting for Overheads

Комментарии