filmov

tv

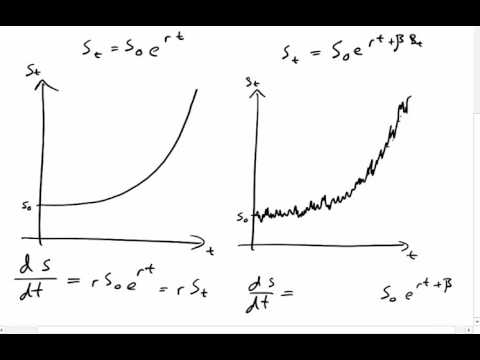

Stochastic Calculus Simplified Part 5: Linear Stochastic Differential Equations

Показать описание

To support our channel, please like, comment, subscribe, share with friends, and use our affiliate links!

Don't forget to check out our patreon:

Affiliate link:

Timestamps:

0:00 Intro

0:58 About the Books

1:34 ODE Review

5:15 Linear SDE

6:34 Example 1

10:16 Example 2

16:33 Exercise

17:48 Two Important SDE

Don't forget to check out our patreon:

Affiliate link:

Timestamps:

0:00 Intro

0:58 About the Books

1:34 ODE Review

5:15 Linear SDE

6:34 Example 1

10:16 Example 2

16:33 Exercise

17:48 Two Important SDE

0:20:47

0:20:47

Stochastic Calculus Simplified Part 5: Linear Stochastic Differential Equations

0:30:28

0:30:28

Stochastic Calculus Lecture 5 Part 1 Basics of Markov Chains; motivation and examples

0:01:58

0:01:58

Stochastic Calculus by Kamil Zajac

0:26:33

0:26:33

Stochastic Calculus: Lecture 1 (Part 5): Characteristic function for random walk

0:12:32

0:12:32

Stochastic Calculus Simplified Part 4: Using Ito's Formula to Find Expectation of Random Variab...

0:20:38

0:20:38

Stochastic Calculus Simplified: Variation of Parameters

0:10:38

0:10:38

5 3 Stochastic integral Part 1

0:26:29

0:26:29

Stochastic Calculus Simplified: Intro to Stochastic Differential Equations - Integration Method

0:18:28

0:18:28

Stochastic Calculus Lecture 5 Part 2 Markov chain notation, transition probabilities and matrix

0:12:56

0:12:56

5 4 Stochastic integral Part 2

0:30:29

0:30:29

Lecture 12 (Part 5): Class of stochastic processes to define stochastic integral; Ito Isometry

0:16:24

0:16:24

Stochastic Calculus Simplified: Probability, Brownian Motion, and Ito Integrals - Part 1

0:00:35

0:00:35

How REAL Men Integrate Functions

0:12:02

0:12:02

Outline of Stochastic Calculus

0:00:12

0:00:12

IIT Bombay Lecture Hall | IIT Bombay Motivation | #shorts #ytshorts #iit

0:10:28

0:10:28

Stochastic Calculus Lecture 3 Part 5 First hitting time to Borel set is stopping time; 2

0:23:15

0:23:15

Stochastic Calculus Simplified: Ito's Formula and Stochastic Integration - Part 2

0:30:27

0:30:27

Lecture 14 (Part 5): Multidimensional Itô's lemma; Itô's product rule; Itô's lemma an...

0:00:20

0:00:20

Bro’s hacking life 😭🤣

0:00:16

0:00:16

This chapter closes now, for the next one to begin. 🥂✨.#iitbombay #convocation

0:22:20

0:22:20

Stochastic Calculus for Quants | Understanding Geometric Brownian Motion using Itô Calculus

1:17:41

1:17:41

5. Stochastic Processes I

0:00:38

0:00:38

Why greatest Mathematicians are not trying to prove Riemann Hypothesis? || #short #terencetao #maths

2:03:36

2:03:36

Lecture 5-Stochastic calculus, APM466/MAT1856 University of Toronto, Feb 6, 2023

Комментарии