filmov

tv

Interpreting regression coefficients in log models part 1

Показать описание

0:05:04

0:05:04

Interpreting regression coefficients in log models part 1

0:05:36

0:05:36

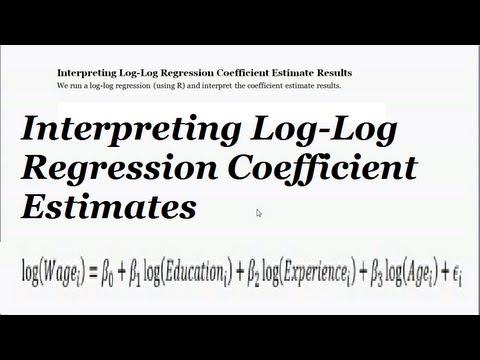

Log-Log Regression & Interpretation (What do the Regression Coefficient Estimate Results Mean?)

0:06:49

0:06:49

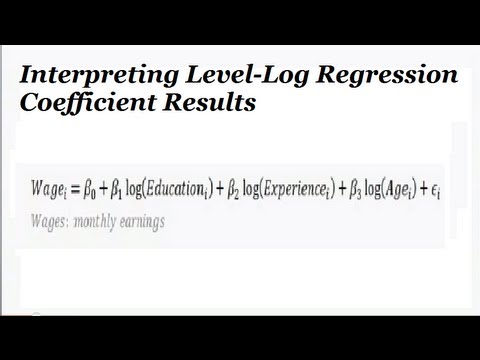

Level-Log Regression & Interpretation (What do the Regression Coefficient Estimate Results Mean?...

0:12:31

0:12:31

Interpretation of regression coefficients: Log-Log, Log-Linear and Linear-Log Model

0:06:38

0:06:38

Log-Level Regression & Interpretation (What do the Regression Coefficient Estimate Results Mean?...

0:08:30

0:08:30

Interpreting log coefficients in regression

0:04:40

0:04:40

Interpreting regression coefficients in log models part 2

0:08:06

0:08:06

Multiple Regression | Coefficients – Interpretation, C.I, Hypothesis Testing

0:06:50

0:06:50

how to interpret a regression coefficient for log variables?

0:05:41

0:05:41

Interpreting Regression Coefficients in Linear Regression

0:11:09

0:11:09

5.7 Logistic Regression: Interpreting Model Coefficients

0:16:29

0:16:29

6.2b Regression Model with Quadratic terms

0:19:02

0:19:02

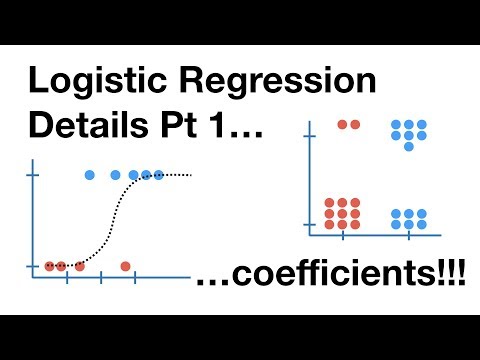

Logistic Regression Details Pt1: Coefficients

0:10:36

0:10:36

How to interpret regression coefficients.#simplified

0:05:03

0:05:03

Level-Level Regression & Interpretation (What do Coefficient Estimate Results Mean?)

0:11:36

0:11:36

Multiple Regression - Interpretation (3of3)

0:06:51

0:06:51

Understanding the Summary Output for a Logistic Regression in R

0:16:45

0:16:45

Video 8: Logistic Regression - Interpretation of Coefficients and Forecasting

0:04:17

0:04:17

Easiest method to interpreting Regression Coefficients!

0:05:25

0:05:25

Log odds interpretation of logistic regression

0:04:11

0:04:11

Interpreting Logistic Regression Tables

0:12:50

0:12:50

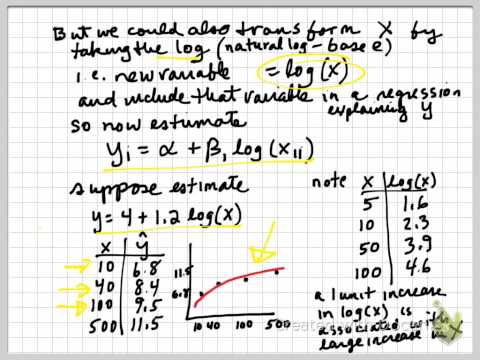

Nonlinear Functional Form 03: Log-Log Regression

0:14:22

0:14:22

Logistic Regression [Simply explained]

0:17:24

0:17:24

Interpreting a semi log regression

Комментарии