filmov

tv

Homeowner's Insurance Coverages Explained

Показать описание

A homeowners policy packages together the specific types of property and liability coverage that a homeowner is likely to need into a single policy. Typically, this includes 6 types of coverage – Coverages A through F

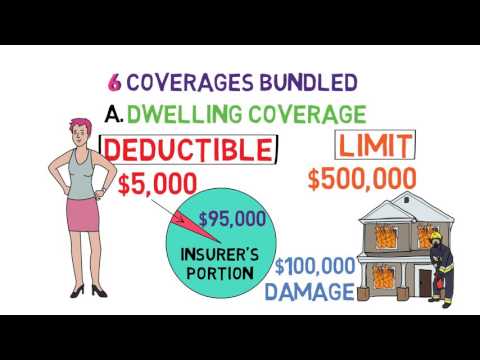

Coverage A also called Dwelling coverage, – is a large part of the homeowner’s policy for those that own their home. This is the coverage that protects the structure of the home in the event of a covered loss.

This part of your policy will cover you for up to the limits of liability as described in your policy. Typically, this is the amount that it would cost to rebuild your home, but that is not necessarily the case. Always talk to your agent about your limits of liability and what you can expect should you suffer a complete loss, such as the destruction of your home by fire.

Should your property include other structures, Coverage B will provide them protection up to 10% of the limits of liability as described in Coverage A.

Other structures include, but are not limited to:

Sheds

Fences

Detached Garage

While Coverage A protects the structure of your home it does not include your personal property, this is where Coverage C comes into the equation. For no additional premium, personal property is protected for up to 50% of the coverage you have from Coverage A. However, if your belonging exceeds the allotted amount of coverage, additional coverage can be purchased. Depending on your policy this coverage could be for actual cash value or replacement cost.

Personal Property includes, but is not limited to:

Household items

Clothing, and other items used and worn by the inhabitants.

Furniture and other large items that are not attached as part of the structure.

Other personal items

Should your home become uninhabitable due to a covered loss, Coverage D can help pay for expenses such as hotel accommodations for up to 10% or 30% of the limits of liability from Coverage A. The intent of this coverage is to pay for the additional expenses that occur as a direct result of you not being able to live in your home.

Coverage E, personal liability coverage, pays for all sums for which you become legally liable because of bodily injuries or property damage to a third party up to the limits of your policy.

However, it does not cover Personal Injury, such as libel or slander.

Finally, Coverage F pays for all medical expenses (up to your limits) incurred within 3 years of an accident that occurred on your property or because of your actions, those of a pet, or another person who resides at the dwelling.

This coverage pays the medical expenses regardless of legal responsibility.

However, it does not pay your medical expenses, or those of any member of the household should they be injured.

It is important to note that some policies have a maximum limit of liability that it will pay to all persons who are injured. This could be different than the limits of liability discussed in Coverage A.

It is important to note, not all coverages are included in every HO policy. For example, a HO5, or Renter’s policy, does not include Coverage A or B. Always discuss the details of your policy with your Insurance Agent.

And don't forget to follow us on social media:

The contents of this video and the information included in it are not intended to serve as a substitute for consultation with an attorney. For legal issues, concerns, and questions please seek the advice of an appropriate legal professional.

REQUESTING COVERAGE DOES NOT GUARANTEE COVERAGE CAN BE PROVIDED. COVERAGE CAN BEGIN ONLY WITH SPECIFIC STATEMENT BY A LICENSED MEMBER OF CONCKLIN INSURANCE AGENCY.

NONE OF THE INFORMATION PROVIDED ON THIS VIDEO IS A GUARANTEE THAT INSURANCE WILL BE PROVIDED OR THAT CONCKLIN INSURANCE AGENCY IS OBLIGATED TO PROCURE INSURANCE FOR ANY VIEWERS.

Coverage A also called Dwelling coverage, – is a large part of the homeowner’s policy for those that own their home. This is the coverage that protects the structure of the home in the event of a covered loss.

This part of your policy will cover you for up to the limits of liability as described in your policy. Typically, this is the amount that it would cost to rebuild your home, but that is not necessarily the case. Always talk to your agent about your limits of liability and what you can expect should you suffer a complete loss, such as the destruction of your home by fire.

Should your property include other structures, Coverage B will provide them protection up to 10% of the limits of liability as described in Coverage A.

Other structures include, but are not limited to:

Sheds

Fences

Detached Garage

While Coverage A protects the structure of your home it does not include your personal property, this is where Coverage C comes into the equation. For no additional premium, personal property is protected for up to 50% of the coverage you have from Coverage A. However, if your belonging exceeds the allotted amount of coverage, additional coverage can be purchased. Depending on your policy this coverage could be for actual cash value or replacement cost.

Personal Property includes, but is not limited to:

Household items

Clothing, and other items used and worn by the inhabitants.

Furniture and other large items that are not attached as part of the structure.

Other personal items

Should your home become uninhabitable due to a covered loss, Coverage D can help pay for expenses such as hotel accommodations for up to 10% or 30% of the limits of liability from Coverage A. The intent of this coverage is to pay for the additional expenses that occur as a direct result of you not being able to live in your home.

Coverage E, personal liability coverage, pays for all sums for which you become legally liable because of bodily injuries or property damage to a third party up to the limits of your policy.

However, it does not cover Personal Injury, such as libel or slander.

Finally, Coverage F pays for all medical expenses (up to your limits) incurred within 3 years of an accident that occurred on your property or because of your actions, those of a pet, or another person who resides at the dwelling.

This coverage pays the medical expenses regardless of legal responsibility.

However, it does not pay your medical expenses, or those of any member of the household should they be injured.

It is important to note that some policies have a maximum limit of liability that it will pay to all persons who are injured. This could be different than the limits of liability discussed in Coverage A.

It is important to note, not all coverages are included in every HO policy. For example, a HO5, or Renter’s policy, does not include Coverage A or B. Always discuss the details of your policy with your Insurance Agent.

And don't forget to follow us on social media:

The contents of this video and the information included in it are not intended to serve as a substitute for consultation with an attorney. For legal issues, concerns, and questions please seek the advice of an appropriate legal professional.

REQUESTING COVERAGE DOES NOT GUARANTEE COVERAGE CAN BE PROVIDED. COVERAGE CAN BEGIN ONLY WITH SPECIFIC STATEMENT BY A LICENSED MEMBER OF CONCKLIN INSURANCE AGENCY.

NONE OF THE INFORMATION PROVIDED ON THIS VIDEO IS A GUARANTEE THAT INSURANCE WILL BE PROVIDED OR THAT CONCKLIN INSURANCE AGENCY IS OBLIGATED TO PROCURE INSURANCE FOR ANY VIEWERS.

0:02:57

0:02:57

0:25:48

0:25:48

0:03:17

0:03:17

0:06:18

0:06:18

0:01:28

0:01:28

0:06:31

0:06:31

0:01:48

0:01:48

0:03:28

0:03:28

0:02:48

0:02:48

0:01:40

0:01:40

0:01:54

0:01:54

0:01:48

0:01:48

0:05:41

0:05:41

0:01:40

0:01:40

0:01:43

0:01:43

0:04:00

0:04:00

0:08:31

0:08:31

0:03:23

0:03:23

0:17:02

0:17:02

0:20:32

0:20:32

0:36:50

0:36:50

0:01:38

0:01:38

0:22:45

0:22:45

0:15:05

0:15:05