filmov

tv

Computing the Sortino Ratio Excel

Показать описание

0:06:25

0:06:25

Computing the Sortino Ratio Excel

0:18:57

0:18:57

Adjusting for downside risk: Calmar, Sterling, and Sortino (Excel)

0:22:51

0:22:51

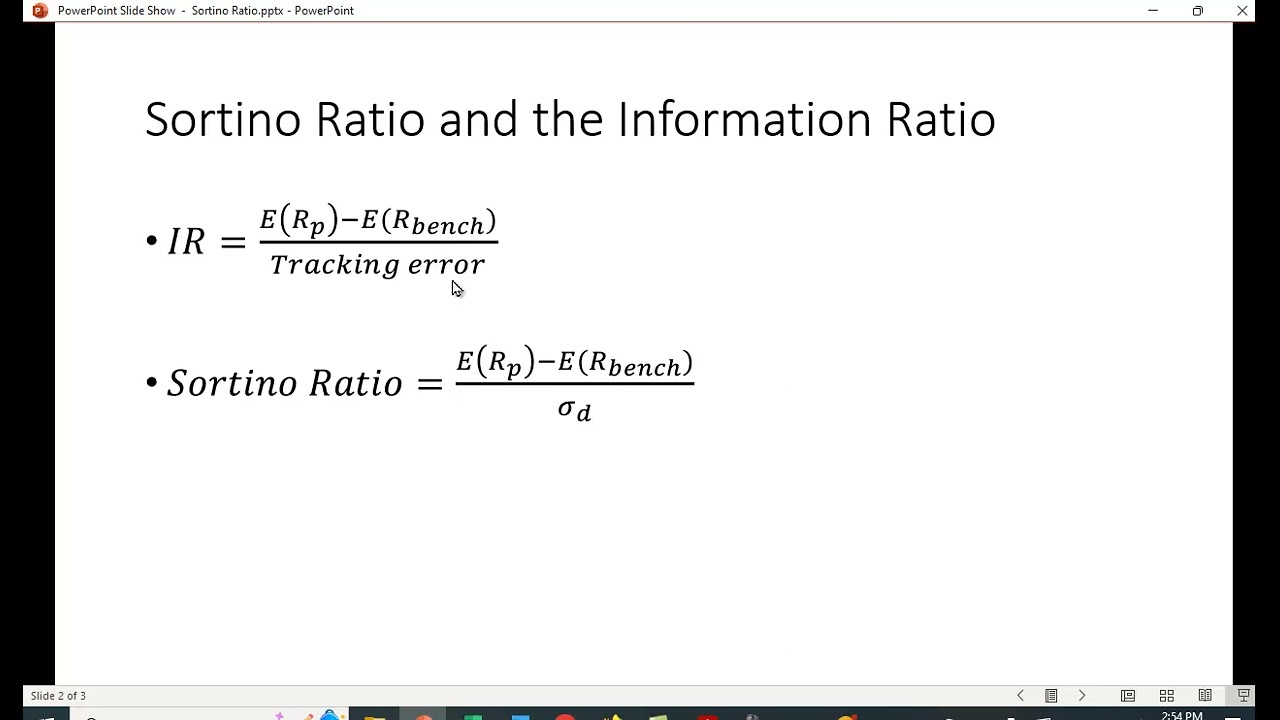

Calculate performance ratios in Excel! Sharpe, Sortino, Treynor, and Information Ratio!

0:01:43

0:01:43

How to calculate the Sortino Ratio.

0:16:24

0:16:24

Sortino Ratio | About Sir Frank A Sortino | Calculation of Sortino Ratio in Excel

0:08:26

0:08:26

Berechnung Sortino Ratio

0:11:23

0:11:23

8 Sortino Ratio

0:22:22

0:22:22

Post-modern portfolio theory explained: Sortino ratio and volatility skewness (Excel)

0:08:52

0:08:52

Investment Performance Evaluation in Excel: Sharpe Ratio, Treynor Ratio & Jensen's Alpha

0:03:14

0:03:14

Sortino Ratio: How to Calculate the Sortino Ratio

0:01:46

0:01:46

Sharpe vs Sortino Ratio | Differences Explained

0:07:43

0:07:43

How to ANALYSE Hedge Funds' Performance | Sharpe, Sortino, Treynor Ratios Explained

![[FRM-11] Video 3](https://i.ytimg.com/vi/NfSRpmr8hPM/hqdefault.jpg) 0:05:12

0:05:12

[FRM-11] Video 3 : Applying CAPM - Sortino Ratio

0:07:16

0:07:16

Calculating Downside Risk in Excel

0:10:36

0:10:36

Computing the Information and Sharpe Ratios in Excel

0:26:42

0:26:42

Portfolio Optimization for Expected Sortino ratio

0:04:50

0:04:50

Calculate Sharpe Ratio In Excel

0:06:12

0:06:12

Sortino Ratio

0:00:57

0:00:57

The Sortino Ratio In Stock Market Explained 2023 #SortinoRatio #Sortino

0:01:44

0:01:44

BILLIONS S3E12 Explained - Axe Capital's Pitch: Sortino Ratio & VIX Trade

0:00:57

0:00:57

The Sortino Ratio In Stock Market Explained 2023 #SortinoRatio #Sortino

0:02:11

0:02:11

How to calculate the Sharpe ratio in Excel

0:11:30

0:11:30

STARR ratio in portfolio management

0:04:01

0:04:01

Understanding Beta | Investopedia

Комментарии