filmov

tv

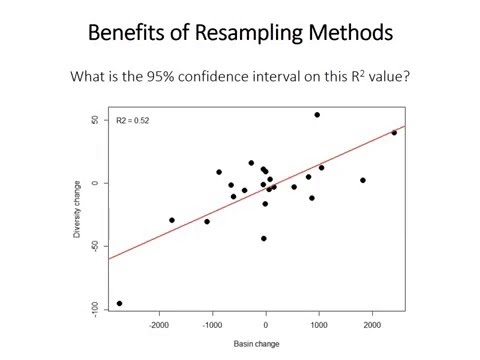

R10: How to Bootstrap. The case of R-squared (Econometrics in R)

Показать описание

In this video, I demonstrate how to write a for loop in R to perform a simple bootstrap calculation. My working example is computing a bootstrap approximation to the sampling distribution for R-squared from a simple linear regression model.

I embed all of my R video tutorials on my econometrics blog here:

A description of this video and the code I used with comments is available here:

I embed all of my R video tutorials on my econometrics blog here:

A description of this video and the code I used with comments is available here:

0:14:11

0:14:11

R10: How to Bootstrap. The case of R-squared (Econometrics in R)

0:05:33

0:05:33

Chapter 5: Constructing Bootstrap Distribution with R

0:15:31

0:15:31

066 Regression coefficients by Bootstrap in R and Excel

0:01:00

0:01:00

R: Bootstrapping for Regression in 60 Seconds

0:08:41

0:08:41

Bootstrapping

0:15:23

0:15:23

How to apply Bootstrap in Statistical Learning

0:05:59

0:05:59

Installing your Bootstrap game on a Windows PC

0:05:53

0:05:53

Bootstrap confidence interval for a proportion

0:02:11

0:02:11

Bootstrapping (Simplified Chinese subtitles)

0:03:13

0:03:13

A bootstrap to test the statistic

0:01:17

0:01:17

R Tutorial: Re-centering a bootstrap distribution for hypothesis testing

0:15:14

0:15:14

bayesboot: An R package for easy Bayesian bootstrapping

0:05:31

0:05:31

Bootstrap confidence interval for the population mean

0:02:31

0:02:31

Time Series Bootstrap - Statistical Inference

0:08:08

0:08:08

R: One-sample bootstrap CI for the mean

0:16:33

0:16:33

Intro R: Bootstrapping

0:06:54

0:06:54

Bootstrapping.

0:18:35

0:18:35

Bootstrap Resampling: Confidence Intervals and One-Sample Example

0:11:26

0:11:26

R Tutorial 5: Cross-Validation and Bootstrap

0:16:30

0:16:30

Bootstrap Confidence Intervals in R

0:09:40

0:09:40

26: Resampling methods (bootstrapping)

0:02:47

0:02:47

Histogram of bootstrap values

0:01:13

0:01:13

What is Bootstrapping

0:10:33

0:10:33

bootstrap-example-intro: theses are us

Комментарии