filmov

tv

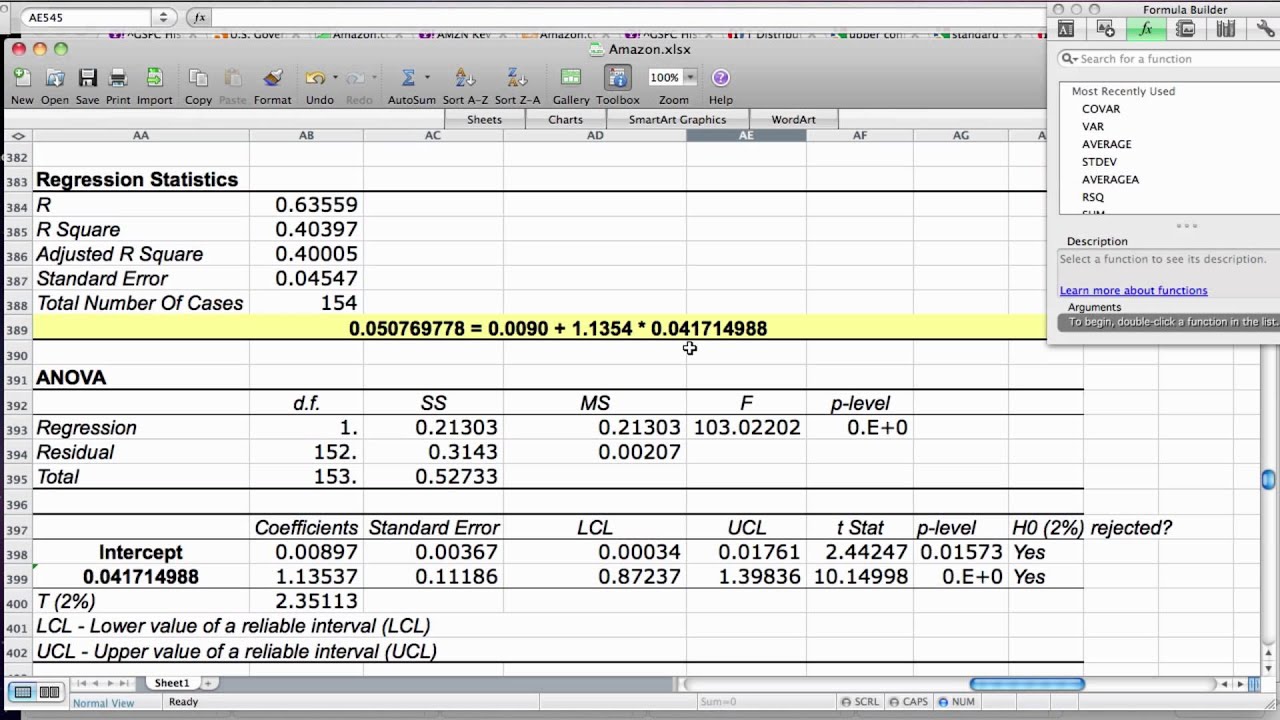

Explanation of Regression Analysis Results

Показать описание

0:06:14

0:06:14

Explanation of Regression Analysis Results

0:16:08

0:16:08

Interpreting Linear Regression Results

0:05:14

0:05:14

How to Report #Regression Analysis Results from #SPSS Output

0:33:19

0:33:19

Regression Output Explained

0:03:51

0:03:51

Regression analysis

0:12:57

0:12:57

Reading Regression Tables

0:45:17

0:45:17

Regression Analysis | Full Course

0:16:24

0:16:24

Regression Analysis Using SPSS - Analysis, Interpretation, and Reporting

0:02:21

0:02:21

Interpretation of Adjusted Odds Ratio from Logistic regression

0:11:36

0:11:36

Multiple Regression - Interpretation (3of3)

0:08:06

0:08:06

Multiple Regression | Coefficients – Interpretation, C.I, Hypothesis Testing

0:09:38

0:09:38

Regression Analysis: An introduction to Linear and Logistic Regression

0:05:32

0:05:32

Simple Linear Regressions

0:02:34

0:02:34

Linear Regression in 2 minutes

0:08:41

0:08:41

Interpreting Output for Multiple Regression in SPSS

0:05:48

0:05:48

019 What Does the StatsModels Summary Regression Table Tell us

0:18:08

0:18:08

Reading and Using STATA Regression Output (Step by step Explanation)

0:04:23

0:04:23

Linear Regression in Excel: How to Interpret a Model & Make Predictions

0:13:29

0:13:29

Video 1: Introduction to Simple Linear Regression

0:09:18

0:09:18

Summary of Interpreting a Regression Output from Stata

0:07:38

0:07:38

Simple linear regression in Excel | with interpretation of regression output

0:05:18

0:05:18

An Introduction to Linear Regression Analysis

0:27:27

0:27:27

Linear Regression, Clearly Explained!!!

0:27:59

0:27:59

Evaluating Regression Model Fit and Interpreting Model Results (2024 Level II CFA® Exam – Reading 2)...

Комментарии