filmov

tv

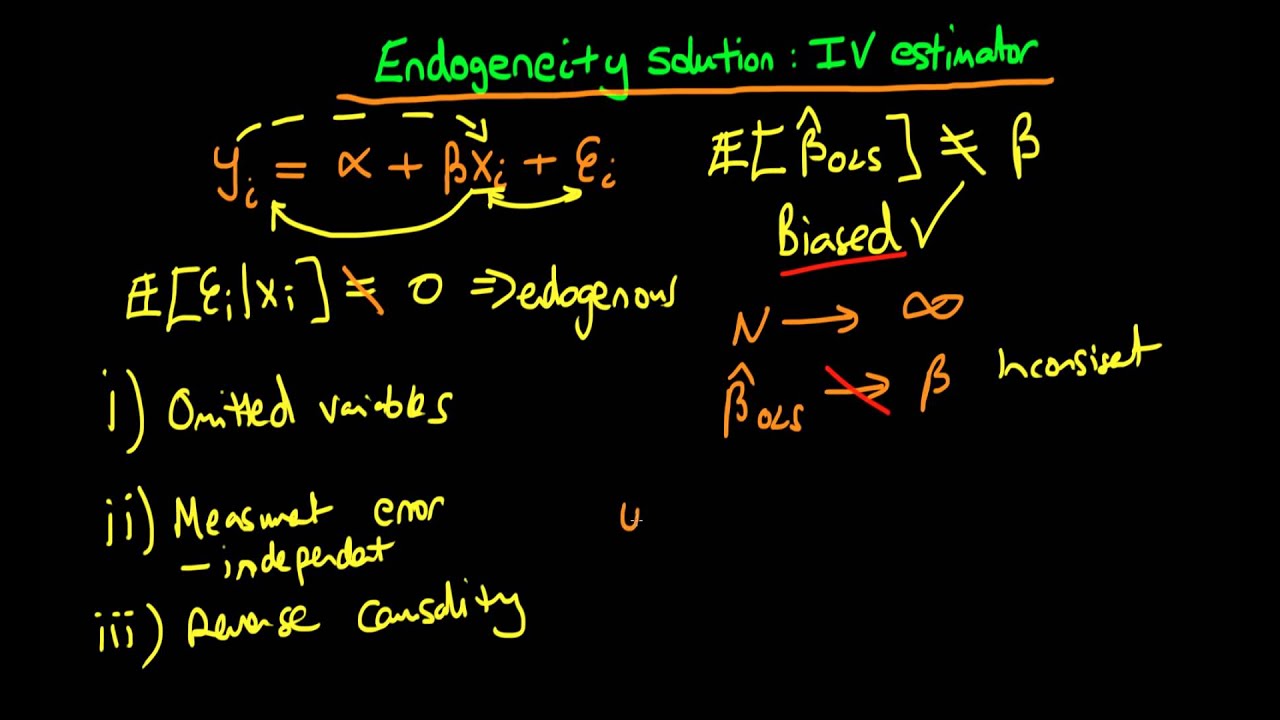

Endogeneity and Instrumental Variables

Показать описание

0:06:30

0:06:30

Endogeneity and Instrumental Variables

0:04:26

0:04:26

Endogeneity lecture 1: What is an endogeneity problem?

0:04:39

0:04:39

Identification, Part 3: Instrumental Variables

1:09:22

1:09:22

Lecture 21: Endogeneity and Instrument Variables

0:09:20

0:09:20

Endogeneity and Instrumental Variables Animation (Beginner)

0:11:04

0:11:04

Instrumental variable solution to endogeneity

0:12:43

0:12:43

PMAP 8521 • (11) Instrumental variables I: (1) Endogeneity and exogeneity

0:13:35

0:13:35

Instrumental Variables - an introduction

0:10:59

0:10:59

Instrumental Variables for Endogeneity Problem

0:05:23

0:05:23

Instrumental-variables regression using Stata®

0:05:02

0:05:02

The Most Simple Explanation of the Endogeneity Bias and 2-Stage Least Squares Regression

0:08:02

0:08:02

Endogeneity tests

0:13:51

0:13:51

Managerial Economics: Endogeneity and Instrumental Variables

0:08:52

0:08:52

#How to perform test of #endogeneity in STATA #2SLS instrumental variables approach

0:11:26

0:11:26

Lecture 103: Instrumental Variable and Endogeneity Bias

0:16:23

0:16:23

Endogeneity: An inconvenient truth (for researchers), by John Antonakis

0:06:30

0:06:30

A Full Course in Econometrics Lecture 137 | Endogeneity and Instrumental Variables

0:56:54

0:56:54

Instrumental Variables

0:16:43

0:16:43

PMAP 8521 • Instrumental variables 2: Endogeneity & exogeneity

0:06:10

0:06:10

Overview of instrumental variable analysis workflow

0:12:57

0:12:57

Introduction to Instrumental Variables (IV)

0:26:58

0:26:58

Instrumental Variables

0:02:26

0:02:26

Microeconomic Evaluation - Instrumental Variables

0:01:11

0:01:11

Instrumental-variables quantile regression

Комментарии