filmov

tv

Practical of straight line depreciation in excel | 2020

Показать описание

How to calculate Straight Line Depreciation in Microsoft Excel?

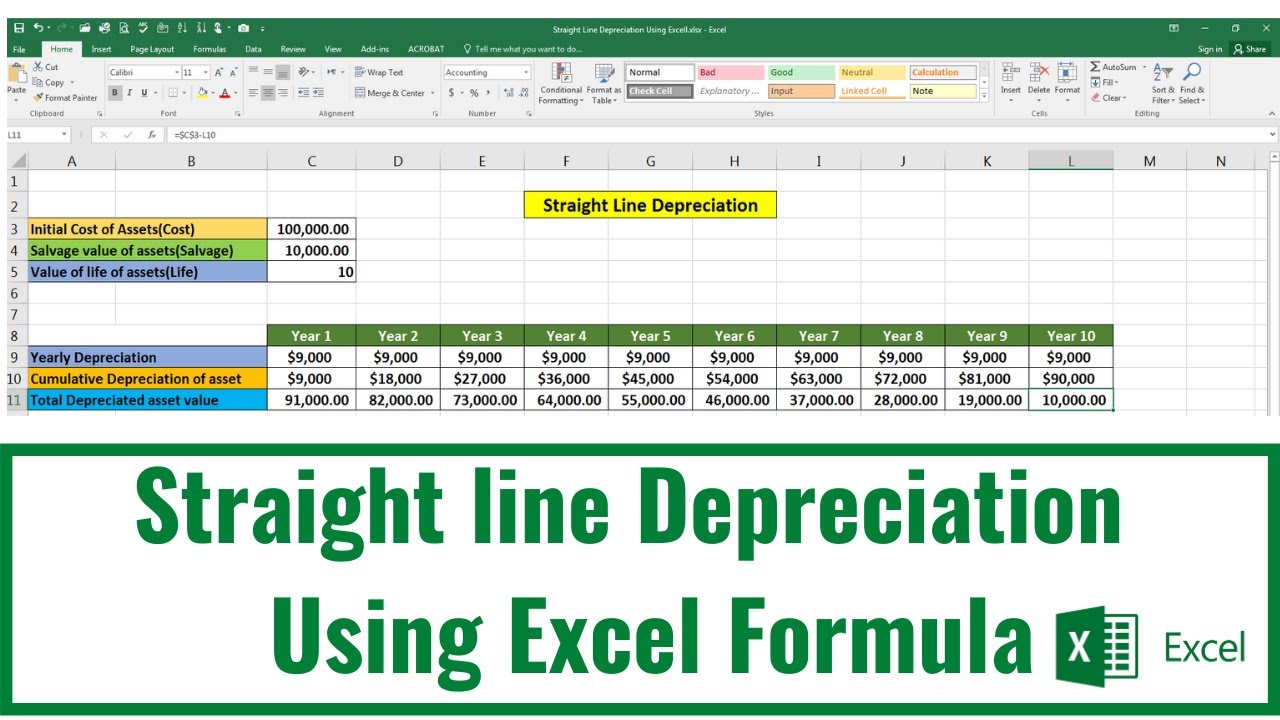

In straight-line depreciation method, cost of a fixed asset is reduced uniformly over the useful life of the asset. Since the depreciation expense charged to income statement in each period is the same, the carrying amount of the asset on balance sheet declines in a straight line.

Due to its simplicity, the straight-line method of depreciation is the most common depreciation method. Generally-accepted accounting principles (GAAP) require companies to depreciate its fixed assets using method that best reflects the pattern in which the assets are expected to generate economic benefits. While the straight-line method is appropriate in most cases, some fixed assets lose more value in initial years. In such situations accelerated depreciation method are more appropriate.

Formula

Depreciation Expense for a year under the straight-line method is calculated by dividing the depreciable amount (the difference between cost and salvage value) of the fixed asset by its useful life (in years).

Straight Line Depreciation Expenses = Depreciable amount / Useful Life of Asset

Depreciable amount equals cost minus salvage value.

Straight Line Depreciation Expenses = Cost − Salvage Value / Useful Life of Asset

Cost is the amount at which the fixed asset is capitalized initially on balance sheet on its acquisition. Salvage value (also called residual value or scrap value) is the estimated value of the fixed asset at the end of its useful life. Since an amount equal to the salvage value can be recovered by selling the asset, only the difference between the cost and the salvage value is depreciated. Useful life of a fixed asset represents the number of accounting periods within which the asset is expected to generate economic benefits.

Annual depreciation rate under the straight-line equals 1 divided by the useful life.

Normally purchase of fixed assets does not coincide with the start of financial year. In such situations, some companies elect to charge the whole-year depreciation to income statement in the year of purchase and do not charge any depreciation expense in the year of disposal. Another method which is more appropriate is to charge proportionate depreciation for partial year which is calculated using the following formula:

Straight-Line Depreciation Expense for Partial Year = D x N / 12

Where

D is the depreciation expense for a complete financial year.

N is the number of months during which the fixed asset was available for use.

#ProfessionalGrooming #StriaghtLineDepreciation #Accounting

In straight-line depreciation method, cost of a fixed asset is reduced uniformly over the useful life of the asset. Since the depreciation expense charged to income statement in each period is the same, the carrying amount of the asset on balance sheet declines in a straight line.

Due to its simplicity, the straight-line method of depreciation is the most common depreciation method. Generally-accepted accounting principles (GAAP) require companies to depreciate its fixed assets using method that best reflects the pattern in which the assets are expected to generate economic benefits. While the straight-line method is appropriate in most cases, some fixed assets lose more value in initial years. In such situations accelerated depreciation method are more appropriate.

Formula

Depreciation Expense for a year under the straight-line method is calculated by dividing the depreciable amount (the difference between cost and salvage value) of the fixed asset by its useful life (in years).

Straight Line Depreciation Expenses = Depreciable amount / Useful Life of Asset

Depreciable amount equals cost minus salvage value.

Straight Line Depreciation Expenses = Cost − Salvage Value / Useful Life of Asset

Cost is the amount at which the fixed asset is capitalized initially on balance sheet on its acquisition. Salvage value (also called residual value or scrap value) is the estimated value of the fixed asset at the end of its useful life. Since an amount equal to the salvage value can be recovered by selling the asset, only the difference between the cost and the salvage value is depreciated. Useful life of a fixed asset represents the number of accounting periods within which the asset is expected to generate economic benefits.

Annual depreciation rate under the straight-line equals 1 divided by the useful life.

Normally purchase of fixed assets does not coincide with the start of financial year. In such situations, some companies elect to charge the whole-year depreciation to income statement in the year of purchase and do not charge any depreciation expense in the year of disposal. Another method which is more appropriate is to charge proportionate depreciation for partial year which is calculated using the following formula:

Straight-Line Depreciation Expense for Partial Year = D x N / 12

Where

D is the depreciation expense for a complete financial year.

N is the number of months during which the fixed asset was available for use.

#ProfessionalGrooming #StriaghtLineDepreciation #Accounting

0:04:40

0:04:40

Practical of straight line depreciation in excel | 2020

0:43:19

0:43:19

#2 Depreciation - Straight Line Method - Problem 1- By Saheb Academy

0:08:36

0:08:36

Straight Line Depreciation Method - Meaning, Example, Formula and Calculations

0:04:34

0:04:34

Arithmetic Sequence - Practical Application Straight Line Depreciation

0:03:56

0:03:56

How to Compute Straight Line Depreciation

0:04:03

0:04:03

How to Calculate Straight Line Depreciation in Excel

0:00:54

0:00:54

Straight line method || Depreciation

0:01:31

0:01:31

Calculate Depreciation in MS Excel - Straight Line and Written Down Value

0:15:17

0:15:17

Depreciation Practical - 03 || Straight Line Method Practical Questions || Accountancy ||

0:00:24

0:00:24

Understanding Straight Line Depreciation: The Simplest Method for Asset Depreciation

0:09:05

0:09:05

How to Create a Straight Line Depreciation Schedule in Excel | Straight Line Depreciation Template

0:01:01

0:01:01

Depreciation methods. #accountancy #deprecation

0:04:23

0:04:23

Straight-line Depreciation for a Partial Year

0:06:43

0:06:43

SLM Method of Calculating Depreciation | Straight Line Method of Depreciation | class 11

0:30:54

0:30:54

Day#26 Excel Financial Accounting (Practical Working on Depreciation Straight line Method)

0:12:11

0:12:11

Depreciation: Straight line method or Original Cost method (Lecture - 2)

0:00:55

0:00:55

straight line depreciation in Excel

0:06:53

0:06:53

Form 3 Agriculture - Calculating depreciation using straight line method

0:00:17

0:00:17

SLN Function #shorts Microsoft Excel Tutorial Straight Line Depreciation

0:05:01

0:05:01

Calculating Depreciation Expense Using the Straight Line Method

0:46:06

0:46:06

Depreciation Accounting - Practical Problems - Straight Line Method - 6

0:42:02

0:42:02

Depreciation Accounting - Practical Problems Based on Straight Line Method - 3

0:08:54

0:08:54

Understanding straight line depreciation

0:01:13

0:01:13

Calculating Straight Line Depreciation in Excel

Комментарии