filmov

tv

2| CONCEPTUAL FRAMEWORK |CHAP 2- QUALITATIVE CHARACTERISTICS OF USEFUL FINANCIAL INFORMATION| FAR210

Показать описание

CHAPTER 2 -QUALITATIVE CHARACTERISTICS OF USEFUL FINANCIAL INFORMATION

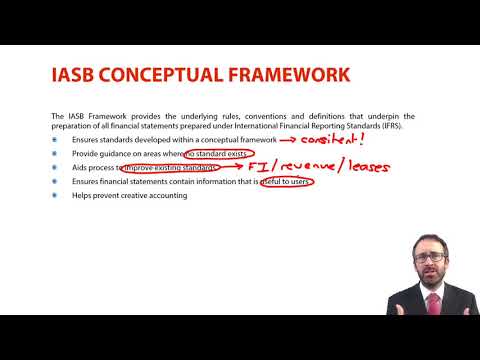

The qualitative characteristics discussed here identify the types of information that are likely to be most useful to the existing and potential investors, lenders and other creditors for making decisions about the reporting entity on the basis of information in its financial report (financial information).

If financial information is to be useful, it must be relevant and faithfully represent what it purports to represent. The usefulness of financial information is enhanced if it is comparable, verifiable, timely and understandable

#MASB#IASB#MIA#IFRS#far410

The qualitative characteristics discussed here identify the types of information that are likely to be most useful to the existing and potential investors, lenders and other creditors for making decisions about the reporting entity on the basis of information in its financial report (financial information).

If financial information is to be useful, it must be relevant and faithfully represent what it purports to represent. The usefulness of financial information is enhanced if it is comparable, verifiable, timely and understandable

#MASB#IASB#MIA#IFRS#far410

2| CONCEPTUAL FRAMEWORK |CHAP 2- QUALITATIVE CHARACTERISTICS OF USEFUL FINANCIAL INFORMATION| FAR210

0:17:48

0:17:48

Conceptual Framework - Intermediate Accounting Chapter 2

0:08:26

0:08:26

(2) Chapter 2- Development of a Conceptual Framework

0:18:28

0:18:28

THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING (PART 2)

0:40:22

0:40:22

FAR1 Conceptual Framework (Ch 2)

0:26:14

0:26:14

THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING (PART 1)

0:08:50

0:08:50

ADMN 502: Chapter 2 - Part 1 - Conceptual Framework

0:03:01

0:03:01

Chapter 2: Conceptual Framework

0:07:05

0:07:05

What Makes Humans UNIQUE in Christian Theology? | Theology & Anthropology

0:31:45

0:31:45

Chapter 2 - Conceptual Framework

0:43:23

0:43:23

ACCA F3/FIA - Chapter 2 - Regulatory Framework

0:08:32

0:08:32

IASB Conceptual Framework - introduction - ACCA Financial Reporting (FR)

0:55:13

0:55:13

2- Intermediate Accounting: Chapter 2

0:08:11

0:08:11

Financial Accounting 9e, Chapter 2: The Conceptual Framework for Financial Reporting

0:15:32

0:15:32

Chapter Two(Theoretical literature review, Empirical literature review and Conceptual framework )

0:10:07

0:10:07

(1) Chapter 2- Need for a Conceptual Framework

0:09:58

0:09:58

CHAPTER 2 | CONCEPTUAL FRAMEWORK OF ACCOUNTING | 11th ACOUNTANCY | LET'S CLEAR with A²

1:11:07

1:11:07

Chapter 2 - Conceptual Framework for Financial Reporting

0:25:17

0:25:17

Lesson4: Qualitative Characteristics of Useful Financial Information, Chp 2 of Conceptual framework

0:19:50

0:19:50

Conceptual Framework Chapter 2

0:03:33

0:03:33

Chapter 2 (Conceptual Framework) Practical Research 2

0:03:00

0:03:00

Develop a Theoretical Framework in 3 Steps | Scribbr 🎓

1:07:52

1:07:52

Chapter 2 IFRS Conceptual Framework

0:35:45

0:35:45

The Conceptual Framework for Financial Reporting

Комментарии