filmov

tv

Calculus 2, Lec 21A, Actuarial Present Value of a Future Payment (Exponential Lifetime)

Показать описание

Calculus 2, Lecture 21A.

(0:00) Plan for the lecture.

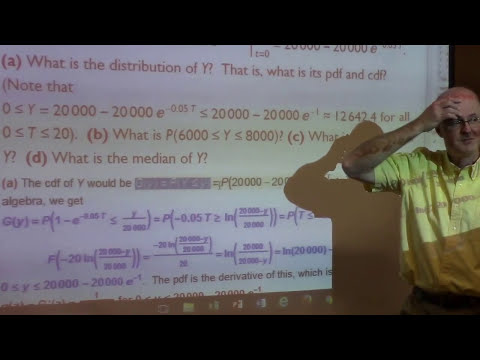

(0:46) Actuarial Present Value of a future payment based on an exponentially distributed lifetime random variable.

(3:00) The probability that T is between 14 and 17 is calculated as F(17) - F(14) and the mean of T is 1 over "lambda".

(4:22) Present value random variable of a future payment.

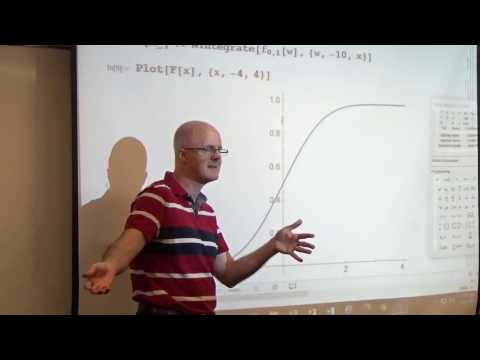

(7:36) Calculations of the pdf, cdf, a probability, the mean, and the median while making use of Mathematica.

(0:00) Plan for the lecture.

(0:46) Actuarial Present Value of a future payment based on an exponentially distributed lifetime random variable.

(3:00) The probability that T is between 14 and 17 is calculated as F(17) - F(14) and the mean of T is 1 over "lambda".

(4:22) Present value random variable of a future payment.

(7:36) Calculations of the pdf, cdf, a probability, the mean, and the median while making use of Mathematica.

0:19:18

0:19:18

0:35:39

0:35:39

0:33:30

0:33:30

0:30:47

0:30:47

0:33:54

0:33:54

0:06:46

0:06:46

0:09:37

0:09:37

0:21:44

0:21:44

0:39:12

0:39:12

0:05:02

0:05:02

0:04:24

0:04:24

0:20:52

0:20:52

0:02:37

0:02:37

0:12:51

0:12:51

0:10:23

0:10:23

0:39:12

0:39:12

0:03:18

0:03:18

0:16:57

0:16:57

0:30:22

0:30:22

0:04:42

0:04:42

1:33:22

1:33:22