filmov

tv

Statement of financial position

Показать описание

What is the statement of financial position, and how can I use it to learn more about the financial situation of a company? What do the various financial terms on the statement of financial position mean, and how do I understand the full picture?

⏱️TIMESTAMPS⏱️

0:00 Introduction to statement of financial position

0:15 What is the statement of financial position

0:34 Balance sheet vs statement of financial position

0:58 Reading a statement of financial position

1:46 Statement of financial position example

3:11 Statement of financial position categories

3:45 Assets on the statement of financial position

8:09 Equity and liabilities on the statement of financial position

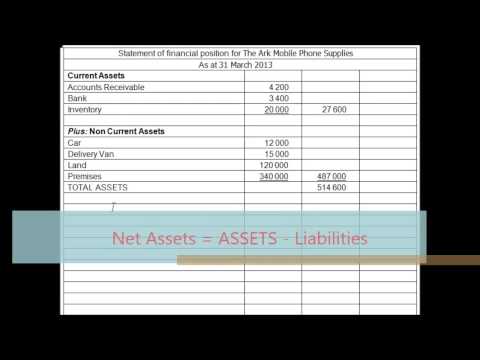

The statement of financial position is an overview of what a company owns and what a company owes at a point in time. What is owned is on the left, what is owed is on the right. It’s like a picture. Most companies call this overview of what is owned and what is owed a balance sheet, some call it a statement of financial position. Not just the name of this financial statement can differ, also the sequence in which the various categories are listed can differ.

By calling it a balance sheet, you describe the structure of the statement: double entry bookkeeping requires debits to equal credits. By calling it a statement of financial position, you describe the function of the statement: it presents the financial position of an entity.

When reading a statement of financial position, it is important to start off reviewing it by category. Non-current assets and current assets on the left. Equity, non-current liabilities, and current liabilities on the right. Non-current assets are longer-term investments that cannot be converted into cash quickly. Current assets are cash and other assets that are expected to be converted to cash within a year. Equity on the balance sheet is the book value of the shareholder capital. Non-current liabilities are amounts owed that are to be paid after the period of one year. Current liabilities are amounts due to be paid to creditors within twelve months.

That’s how the statement of financial position works on a conceptual level. Let’s now look into the statement of financial position of a real-world company: aerospace corporation Airbus. We will review the statement of financial position for December 31st, 2019. As the statement of financial position is just a picture at a point in time, and a lot has happened in early 2020, future balance sheets of Airbus might look very different. Non-current assets €57,7 billion, current assets €56,7 billion, adding up to total assets of €114,4 billion. Equity €6 billion, non-current liabilities €46 billion, current liabilities €62,4 billion. The total amount owned equals the total amount owed. Per the accounting equation: assets equal equity plus liabilities. To put things in perspective, I always calculate as a minimum two financial ratios for the statement of financial position. The current ratio, current assets divided by current liabilities, is 0.9 for Airbus: for every Euro of current liabilities, there is 90 cents of current assets available. Equity as percentage of the balance sheet total is just 5.2%, fairly low compared to what I have seen on the statement of financial position for other companies.

Let’s zoom into the statement of financial position in more detail, and review what is in each of the balance sheet categories: non-current assets, current assets, equity, non-current liabilities, and current liabilities. Same five categories, just a lot more detail to dig into. In the European format of the statement of financial position, assets are listed from least liquid to most liquid. Liabilities are listed from due last to due first. I will take you through the main line items.

Philip de Vroe (The Finance Storyteller) aims to make accounting, #finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

⏱️TIMESTAMPS⏱️

0:00 Introduction to statement of financial position

0:15 What is the statement of financial position

0:34 Balance sheet vs statement of financial position

0:58 Reading a statement of financial position

1:46 Statement of financial position example

3:11 Statement of financial position categories

3:45 Assets on the statement of financial position

8:09 Equity and liabilities on the statement of financial position

The statement of financial position is an overview of what a company owns and what a company owes at a point in time. What is owned is on the left, what is owed is on the right. It’s like a picture. Most companies call this overview of what is owned and what is owed a balance sheet, some call it a statement of financial position. Not just the name of this financial statement can differ, also the sequence in which the various categories are listed can differ.

By calling it a balance sheet, you describe the structure of the statement: double entry bookkeeping requires debits to equal credits. By calling it a statement of financial position, you describe the function of the statement: it presents the financial position of an entity.

When reading a statement of financial position, it is important to start off reviewing it by category. Non-current assets and current assets on the left. Equity, non-current liabilities, and current liabilities on the right. Non-current assets are longer-term investments that cannot be converted into cash quickly. Current assets are cash and other assets that are expected to be converted to cash within a year. Equity on the balance sheet is the book value of the shareholder capital. Non-current liabilities are amounts owed that are to be paid after the period of one year. Current liabilities are amounts due to be paid to creditors within twelve months.

That’s how the statement of financial position works on a conceptual level. Let’s now look into the statement of financial position of a real-world company: aerospace corporation Airbus. We will review the statement of financial position for December 31st, 2019. As the statement of financial position is just a picture at a point in time, and a lot has happened in early 2020, future balance sheets of Airbus might look very different. Non-current assets €57,7 billion, current assets €56,7 billion, adding up to total assets of €114,4 billion. Equity €6 billion, non-current liabilities €46 billion, current liabilities €62,4 billion. The total amount owned equals the total amount owed. Per the accounting equation: assets equal equity plus liabilities. To put things in perspective, I always calculate as a minimum two financial ratios for the statement of financial position. The current ratio, current assets divided by current liabilities, is 0.9 for Airbus: for every Euro of current liabilities, there is 90 cents of current assets available. Equity as percentage of the balance sheet total is just 5.2%, fairly low compared to what I have seen on the statement of financial position for other companies.

Let’s zoom into the statement of financial position in more detail, and review what is in each of the balance sheet categories: non-current assets, current assets, equity, non-current liabilities, and current liabilities. Same five categories, just a lot more detail to dig into. In the European format of the statement of financial position, assets are listed from least liquid to most liquid. Liabilities are listed from due last to due first. I will take you through the main line items.

Philip de Vroe (The Finance Storyteller) aims to make accounting, #finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

0:09:47

0:09:47

Statement of financial position

0:08:00

0:08:00

How the Balance Sheet Works | Understand the Statement of Financial Position

0:12:48

0:12:48

How The BALANCE SHEET Works (Statement of Financial Position / SOFP)

0:15:45

0:15:45

Statements of Financial Position

0:09:06

0:09:06

FINANCIAL STATEMENTS: all the basics in 8 MINS!

0:17:23

0:17:23

STATEMENT OF FINANCIAL POSITION(BALANCE SHEET FOR A SOLE TRADER)FINAL ACCOUNTS P2 #accounting#viral

0:05:01

0:05:01

Statement of Financial Position (Balance Sheet) | Company

0:40:42

0:40:42

The Statement of Financial Position and Income Statement (part a) - ACCA (FA) lectures

0:50:04

0:50:04

FA - August 2024 Question 4B

0:05:57

0:05:57

Statement of Financial Position

0:06:59

0:06:59

The BALANCE SHEET for BEGINNERS (Full Example)

0:24:30

0:24:30

Income Statement & Statement of Financial Position for a sole trader

0:27:16

0:27:16

Final Accounts Question - Income Statement & Statement of Financial Position - 2018 OL Paper

0:45:21

0:45:21

CONSOLIDATED STATEMENT OF FINANCIAL POSITION (PART 1) - IFRS 10

0:08:48

0:08:48

The Statement of Financial Position Explained - Sole Trader (FULL EXAMPLE)

0:04:02

0:04:02

Statement of Financial Position (Balance Sheet)

0:04:01

0:04:01

Easy Way to Complete a Balance Sheet | Statement of Financial Position Explained

0:21:11

0:21:11

STATEMENT OF FINANCIAL POSITION

0:10:28

0:10:28

Statements of Financial Position (Balance Sheets) explained in about10 mins

0:09:29

0:09:29

Trial Balance to Income Statement and Statement of Financial Position

0:11:12

0:11:12

Statement of Financial Position (Balance Sheet) Accounting 101 Lesson 9 A Level Accounting

0:08:44

0:08:44

Introduction to the Statement of Financial Position

0:17:00

0:17:00

The Financial Statements & their Relationship / Connection | Explained with Examples

0:18:30

0:18:30

#1 Financial Statements - Concept - Easiest Way - Class 11 - By Saheb Academy

Комментарии